German Data Review: Lower Headline Amid Clearer Drop in Services Inflation

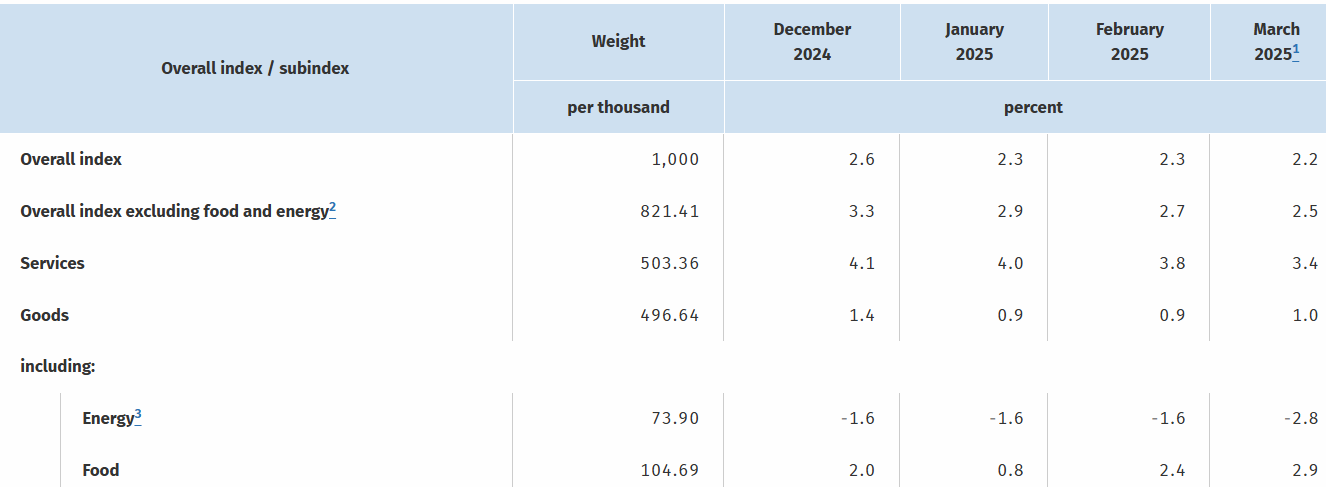

Germany’s disinflation process continues, but there had been signs that the downtrend was flattening out but this changed somewhat in February and again in the March preliminary numbers. Indeed, HICP inflation fell back from January’s 2.8% to a 3-mth low of 2.6% last month and then to 2.3% in March, this despite a pick-up in food inflation in both months. Notably the March outcome is the third lowest reading in this down-cycle, with only the two on target outcomes in late summer below. Moreover, perhaps clearer disinflation news was evident in the where the core which fell back 0.2 ppt while services eased 0.4 ppt to cycle-low - both of the latter are for the CPI measure. Moreover, adjusted m/m data also show some fresh downtick in core rates.

Figure 1: Less Services Inflation Persistence?

Source: German Federal Stats Office, % chg y/y

As for the looming EZ HICP flash we still think they may deliver better news and broadly so. Indeed, we see more supportive news in the March flash numbers, with the headline and core down 0.2 ppt (the former to 2.1% and hence the lowest since last autumn), services down perhaps a little more sizeable and the core down and where adjusted data continue to suggest underlying price pressures are consistent with the ECB target