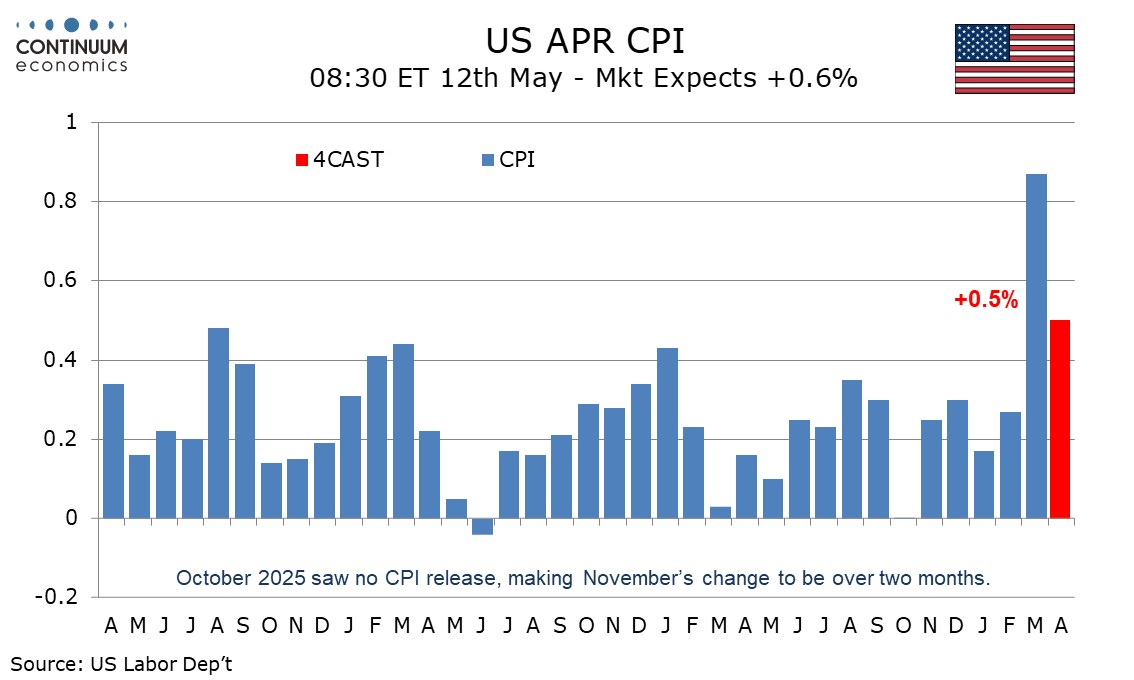

Preview: Due May 12 - U.S. April CPI - Energy to rise less sharply than in March, but air fares to lift the core

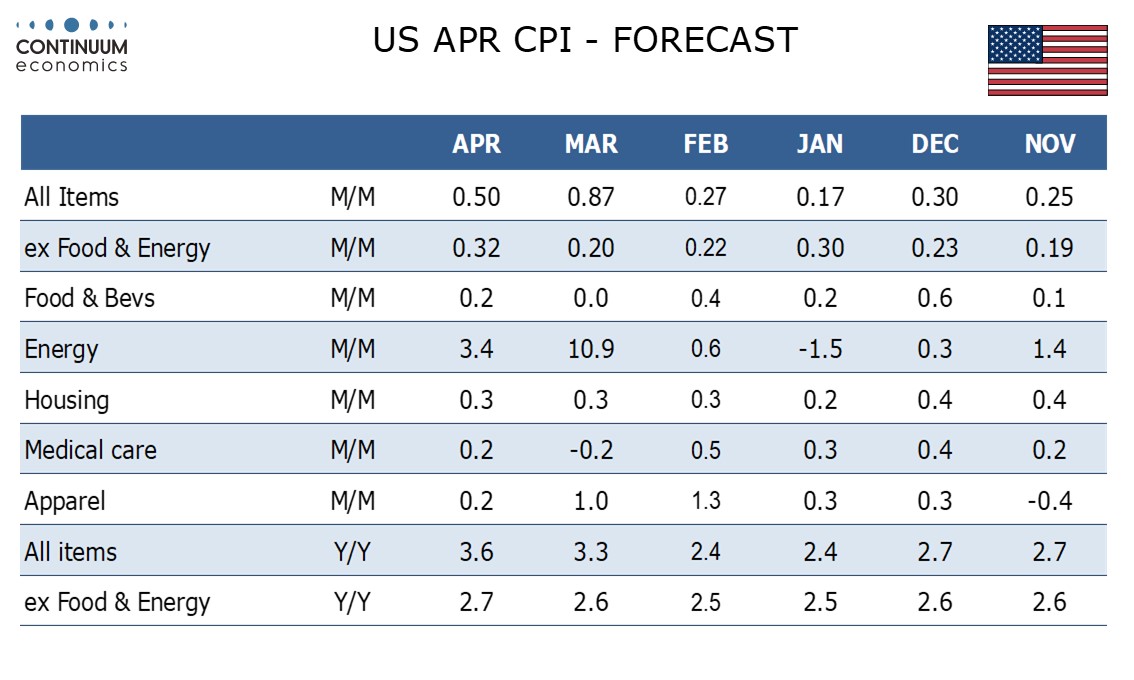

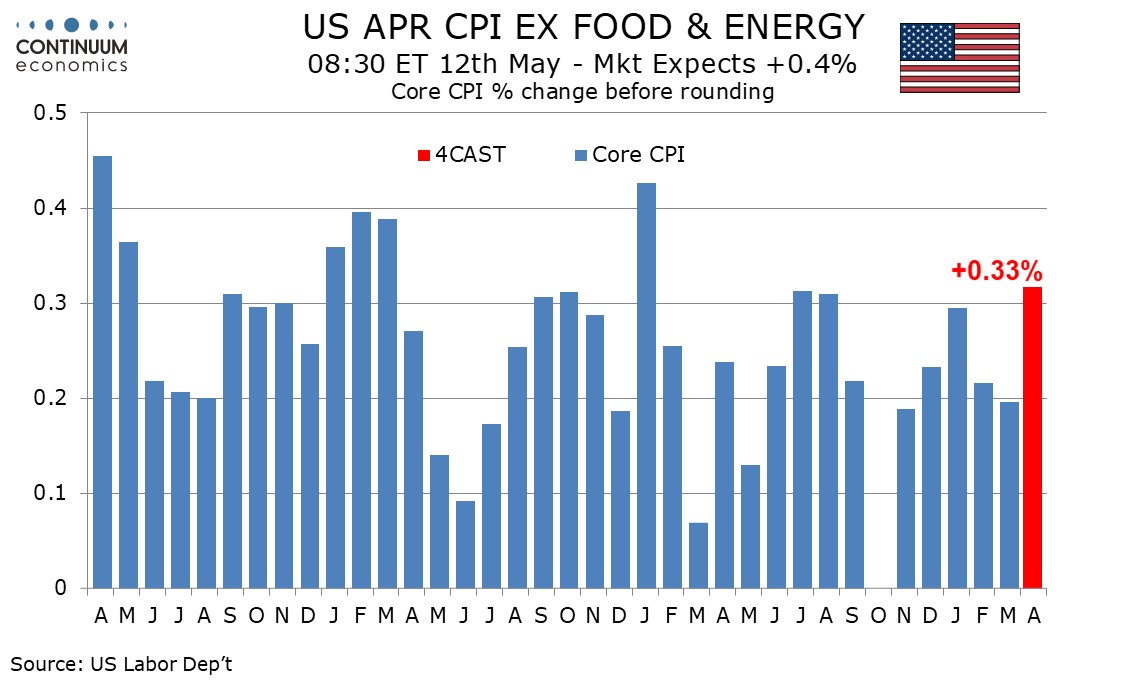

We expect April CPI to increase by 0.5% overall and 0.3% ex food and energy, with the latter rising by 0.33% before rounding and the highest since January 2025. Seasonal adjustments will restrain the increase in gasoline but we expect feed through of energy prices to air fares to be factor in lifting the core rate.

In March gasoline prices surged by 24.9% unadjusted and 21.2% seasonally adjusted, lifting overall CPI to a 0.9% increase while the ex food and energy rate rose by a modest 0.2%. In April gasoline prices look set to rise by around 12.0% unadjusted but this would leave seasonally adjusted gasoline prices up a less steep 6.5%, adding almost 0.2% to the CPI. We expect overall energy prices to rise by 3.4% and food to rise by 0.2%, the latter after a flat March and a 0.4% increase in February. Higher fertilizer prices pose an upside risk to food in the months ahead but we do not expect an impact from this to be seen in the CPI yet.

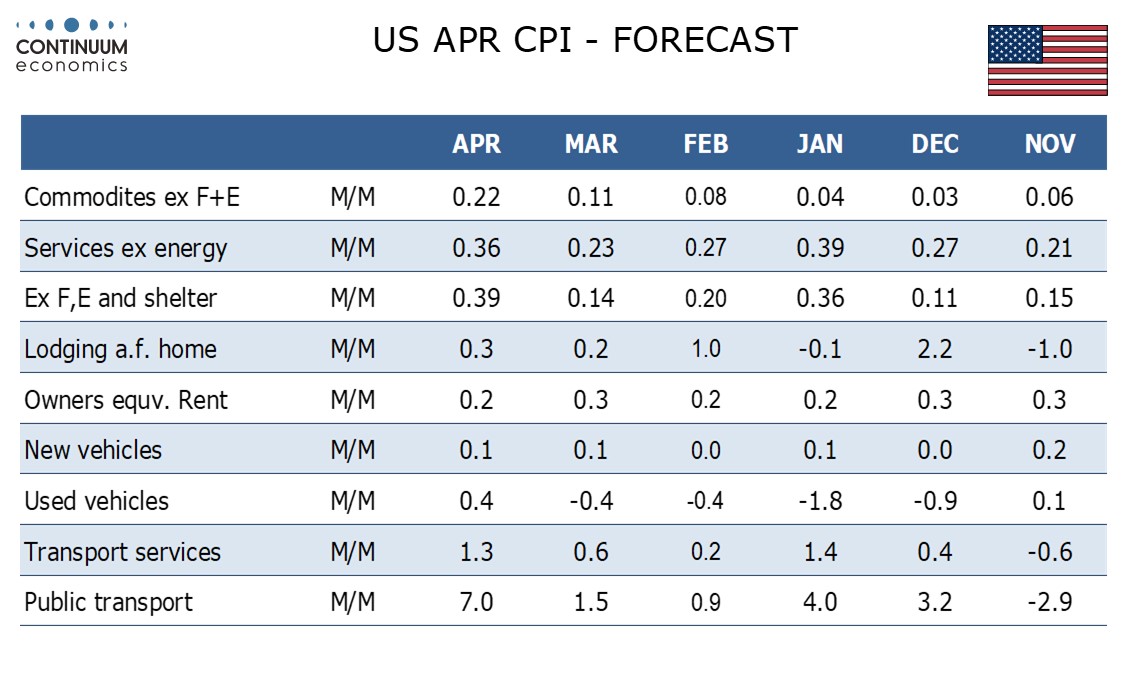

February and March both saw the ex food and energy rate rise by 0.2% after a 0.3% increase in January, a month which is more prone to out of trend moves than most as pricing decisions are made at the start of the year. The tariff impact is fading and were it not for the energy shock another 0.2% increase in the core rate would probably have been seen. Feed through from energy prices is likely to be modest in most components, but is likely to be significant in air fares. We also expect used auto prices to see a correction from recent slippage and increase for the first time in five months. We expect a 1.8% increase in transport, with autos, gasoline and air fares all contributing.

Medical care prices are unlikely to repeat a March decline though with March data correcting from preceding strength we do not expect a strong increase. There is some downside risk in apparel after two straight strong gains, while we expect shelter to slow from a slightly above trend March. Excluding food, energy and shelter we expect a 0.4% increase, 0.39% before rounding. We expect commodities ex food and energy, lifted by autos, to rise by 0.23%, and services ex energy, lifted by air fares, to rise by 0.36%, rounding to 0.2% and 0.4% respectively.

The monthly gains we expect would compare to 0.2% increases both overall and ex food and energy in April 2025, and thus lift yr/yr growth to 3.6% from 3.3% overall and to 2.7% from 2.6% ex food and energy. The overall yr/yr pace will be the highest since September 2023 but the yr/yr ex food and energy pace will have been stronger as recently as September 2025.