Eurozone: Services Offer Sobering News

The May flash composite PMI data may have fallen into apparent contraction territory as the index dropped to 49.5 in May from 50.4 in April, below the 50.0 no-change mark for the first time in five months and thereby signalling a reduction, albeit a marginal one. We do not take much issue whether the composite is signalling marginal expansion or, as seemingly the case at present, the opposite. More notable is the message in the surveys, mainly still weak growth and where services activity is faltering. The latter is all the more worrisome as a) services have been the mainstay of EZ GDP growth in the last 4-6 quarters and b) the hope that the sector would offer further, if not greater support to shield the economy from manufacturing weakness accentuated by tariff tensions. The other message is that price weakness, if not disinflation persists, with France even seeing the most marked discounting since midway through the pandemic

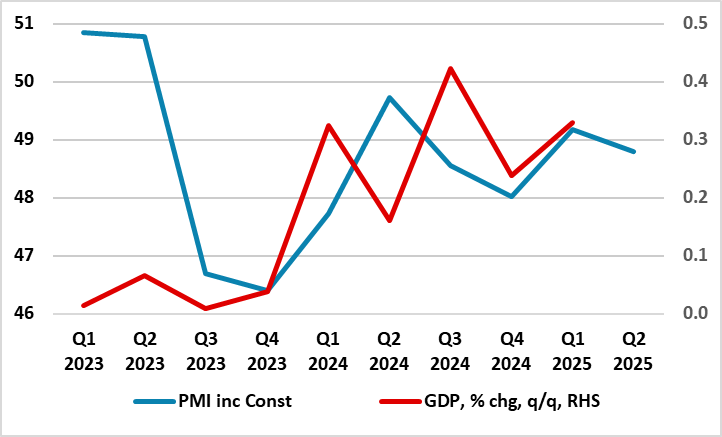

Figure 1: PMI Weakness May Overstate Lost Momentum

Source: Eurostat, Markit

This weaker-than-expected PMI outcome was largely echoed by May business survey data in France (INSEE) and Germany (Ifo), all pointing to weak real activity. Thus the data will be uncomfortable reading for the ECB. The data very much suggest that the better news regarding EZ consumer spending seen of late (albeit where retail sales may have slipped afresh) has failed to bolster either output or business sentiment and where instead global economy uncertainty is causing continued falls even ahead of what may be a marked blow should tariffs actually be extended as is being threatened. The data imply a little above flat growth at best (Figure 1) which includes even weaker construction PMI numbers). But the main message are worrying hints, if not acknowledgements, that hitherto solid services output is buckling as sentiment turns sour. In fact, excluding the outbreak of the COVID-19 pandemic in 2020, services sentiment was the second-lowest since the end of 2012.

Momentum Lost?

While the ECB may draw some comfort from signs of a seemingly Q1 further recovery in consumer spending, albeit with little evidence that disinflation has persuaded households to run down what seem to be elevated savings, there seems to be a general and continued loss of momentum nonetheless, led by continued weakness which may now be spilling over more discernibly into weak exports. In addition, the increasing weakness in the labor market that the PMIs point to is also hardly as positive from a demand perspective, especially is ECB wage indicators are right in suggesting much slower pay rises. Moreover, the risks are that the whole of the EZ is weakening given the possibly gloomier messages from business survey data into the current quarter with it likely that the modest Q1 GDP rise actually reflected fresh GDP declines as the quarter finished. We still see a very sub-consensus 0.5% GDP picture thus year although note that the consensus is dropping towards our view!

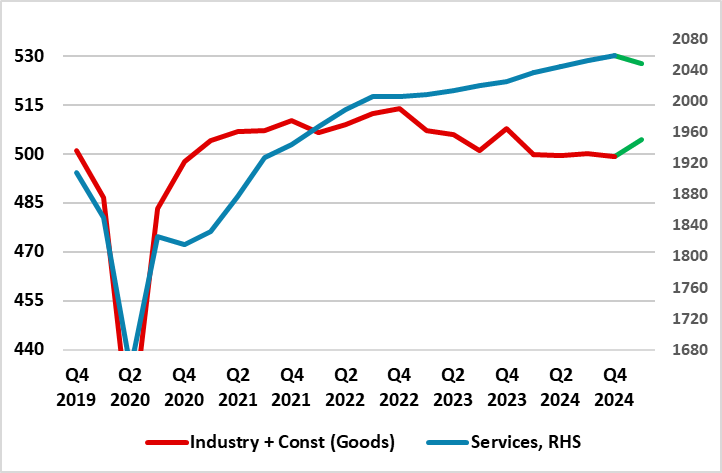

Figure 2: Services Succumbing?

Source: Eurostat, green lines are CE Q1 projections (EUR billion)

The latter is important and is very much the main perturbing message from the PMIs. As we have noted before, the limp EZ recovery over recent quarters has come in spite of protracted manufacturing weakness with services instead having offered support. This may be changing albeit with the factory sector still in trend reverse (albeit with a Q1 jump in anticipation of the tariffs) while services flatten out if not falter (Figure 2). Indeed, it could very well be that actual services output fell sharply at the end of Q1, possibly setting an adverse precedent for at least H1 this year, and where the evolution of how global risks develop deciding what happens thereafter – we are not reassured.

As for inflation, there have been some less reassuring signs fi late, albeit probably more a result of the timing of Easter this effect even pushing up underlying gauges. But the anecdotal still soft message from the PMI regarding output prices is supportive as disinflation provides the ECB with the scope to ease policy while weak activity (actual and/or threatened) provides the rationale.