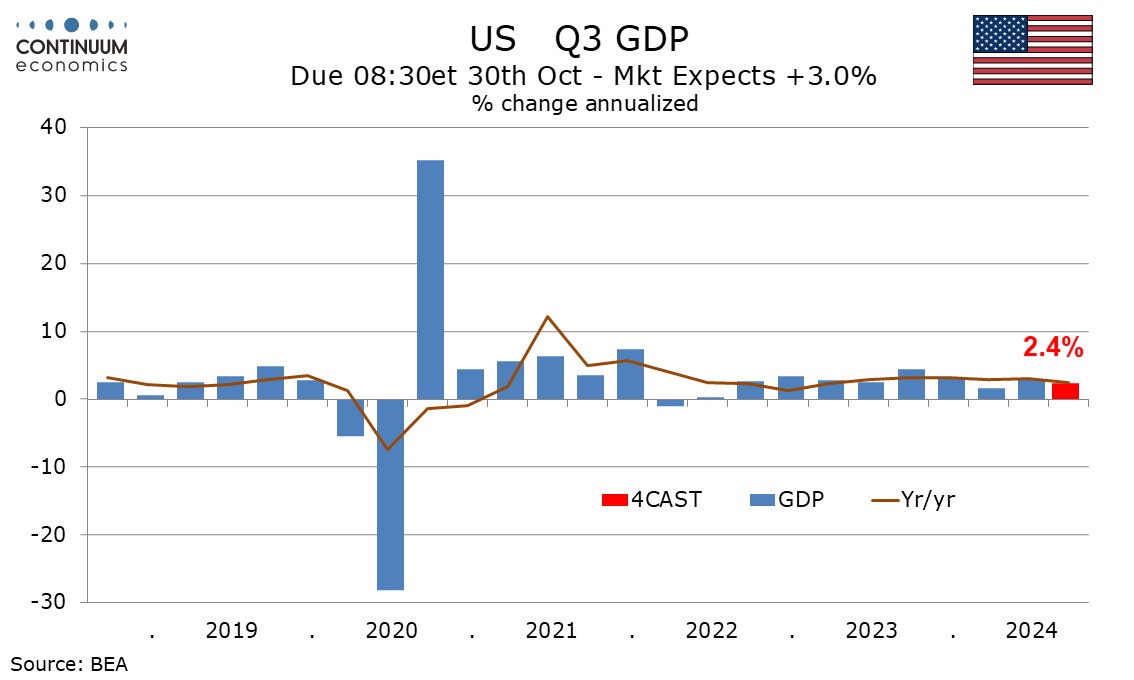

Preview: Due October 30 - U.S. Q3 GDP - Slower but still solid with Core PCE Prices consistent with target

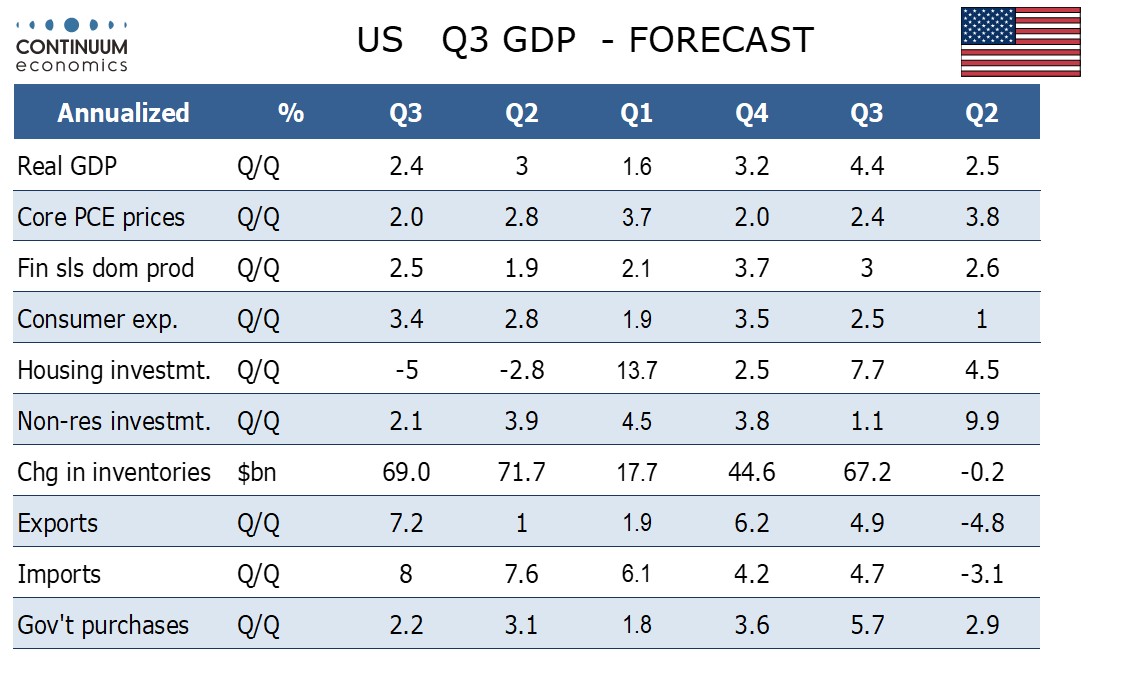

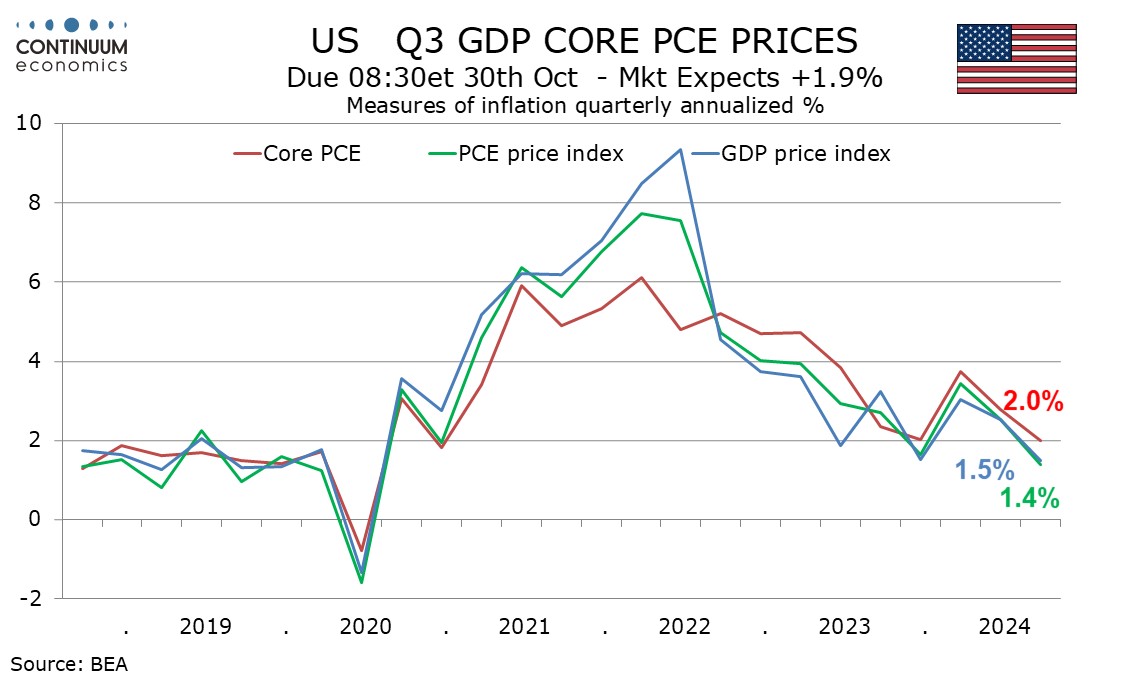

We expect a 2.4% annualized increase in Q3 GDP, slower than Q2’s 3.0% but still maintaining solid momentum. with a slowing in core PCE prices to an on-target 2.0% annualized after gains of 2.8% in Q2 and 3.7% in Q1.

Q3’s GDP gain will be led by consumer spending. The biggest uncertainty lies in business investment, which we expect to slow from an above trend Q3.

For core PCE prices to even reach the Fed’s 2.0% target we require a stronger increase in September, as hinted at by September’s core CPI. Lower gasoline prices will restrain overall PCE prices, we expect to 1.4%, and we expect a similar 1.5% rise in the overall GDP price index.

For core PCE prices to even reach the Fed’s 2.0% target we require a stronger increase in September, as hinted at by September’s core CPI. Lower gasoline prices will restrain overall PCE prices, we expect to 1.4%, and we expect a similar 1.5% rise in the overall GDP price index.

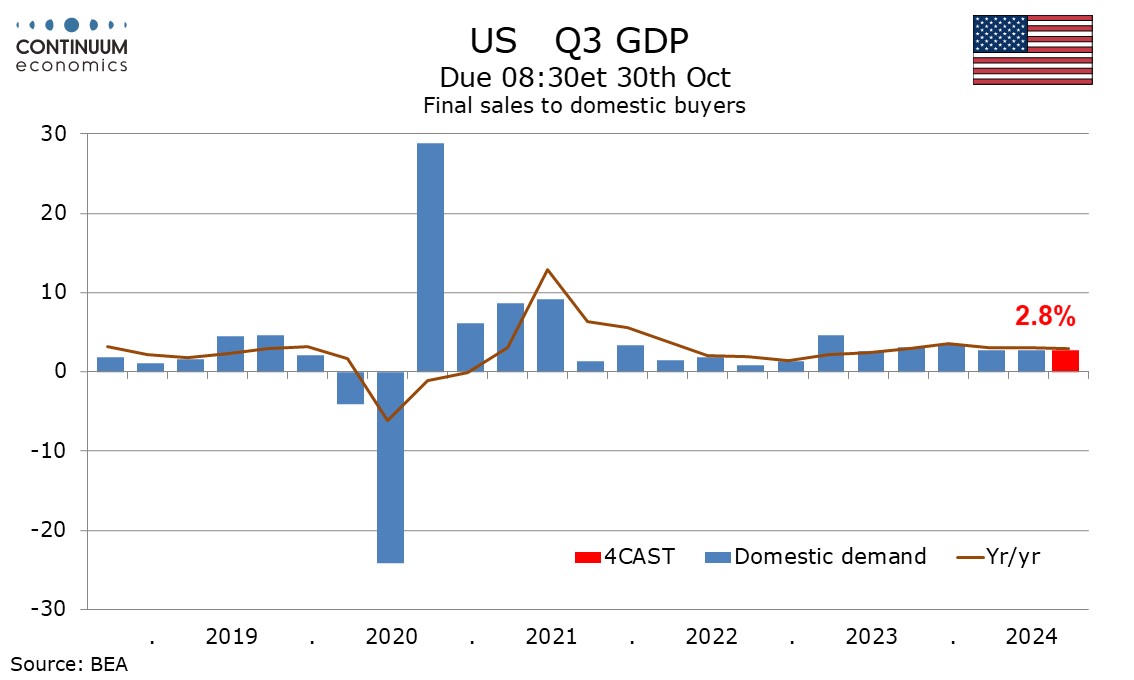

We expect final sales to domestic buyers (GDP less inventories and net exports) to rise by 2.8%, matching Q2’s pace and similar to Q1’s 2.7%, suggesting a very steady underlying pace.

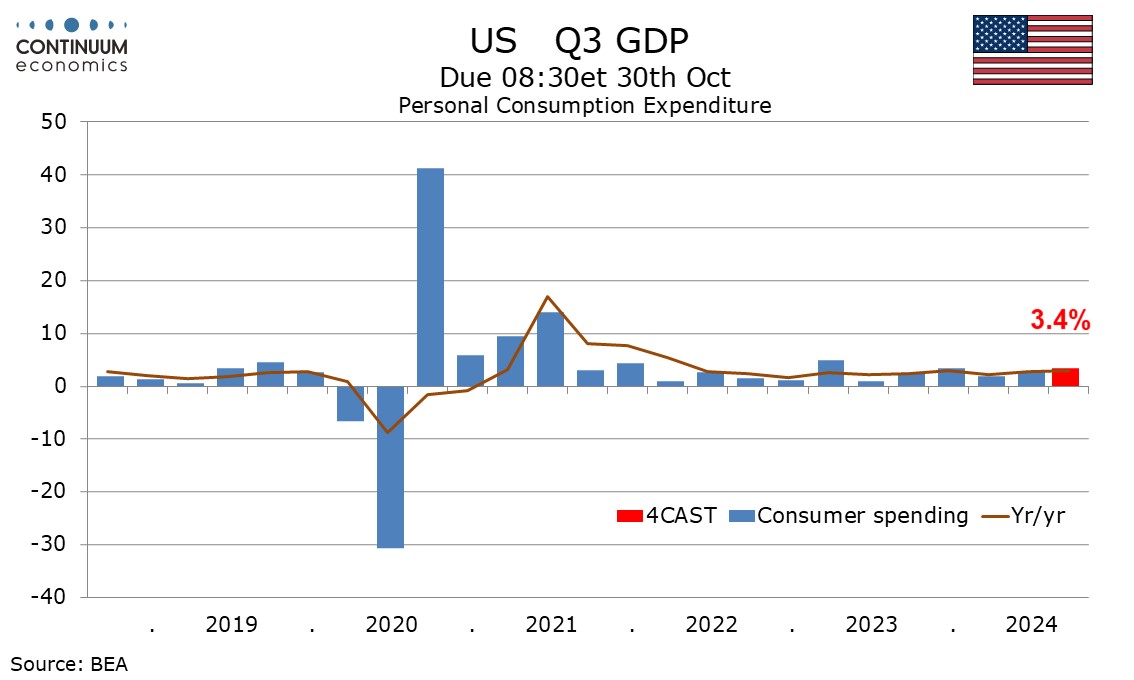

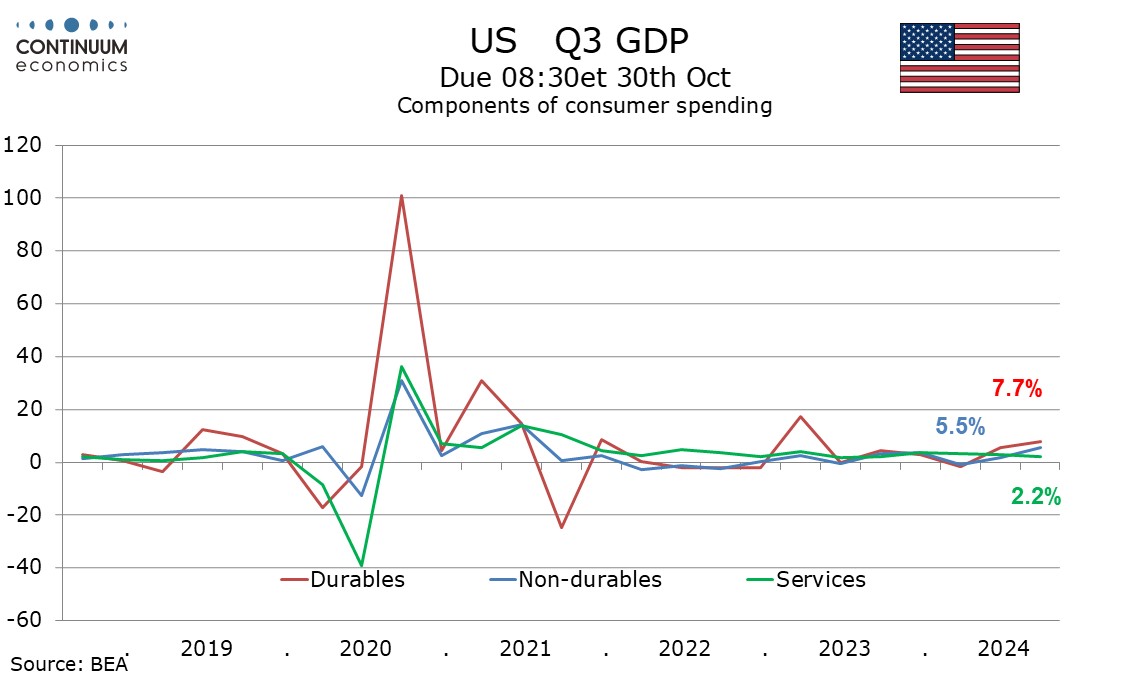

We expect a strong 3.4% increase in consumer spending, led by retail sales. For services we expect a moderate 2.2% increase which would be a 4-quarter low.

We expect a strong 3.4% increase in consumer spending, led by retail sales. For services we expect a moderate 2.2% increase which would be a 4-quarter low.

We expect the consumer spending gain to significantly outpace a 1.4% increase in real disposable income, though after the upward revisions to historical income with the final Q2 data yr/yr data will still show income consistent with spending, limiting downside risk to spending going forward.

We expect the consumer spending gain to significantly outpace a 1.4% increase in real disposable income, though after the upward revisions to historical income with the final Q2 data yr/yr data will still show income consistent with spending, limiting downside risk to spending going forward.

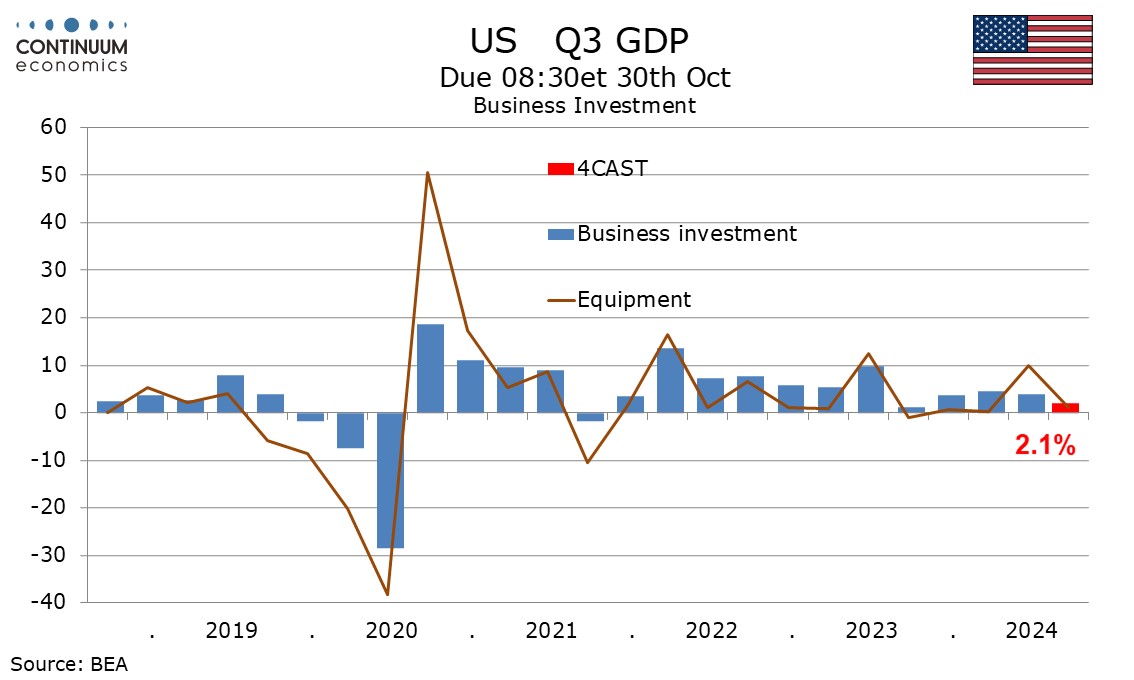

We expect business investment to slow to a 2.1% pace from 3.9% in Q2, with equipment slowing sharply to 1.1% from a 9.8% Q2 increase that came mostly in transportation equipment and is unlikely to be repeated. We expect intellectual property and structures to see modest accelerations from weak Q2 gains that fell short of 1.0%.

We expect business investment to slow to a 2.1% pace from 3.9% in Q2, with equipment slowing sharply to 1.1% from a 9.8% Q2 increase that came mostly in transportation equipment and is unlikely to be repeated. We expect intellectual property and structures to see modest accelerations from weak Q2 gains that fell short of 1.0%.

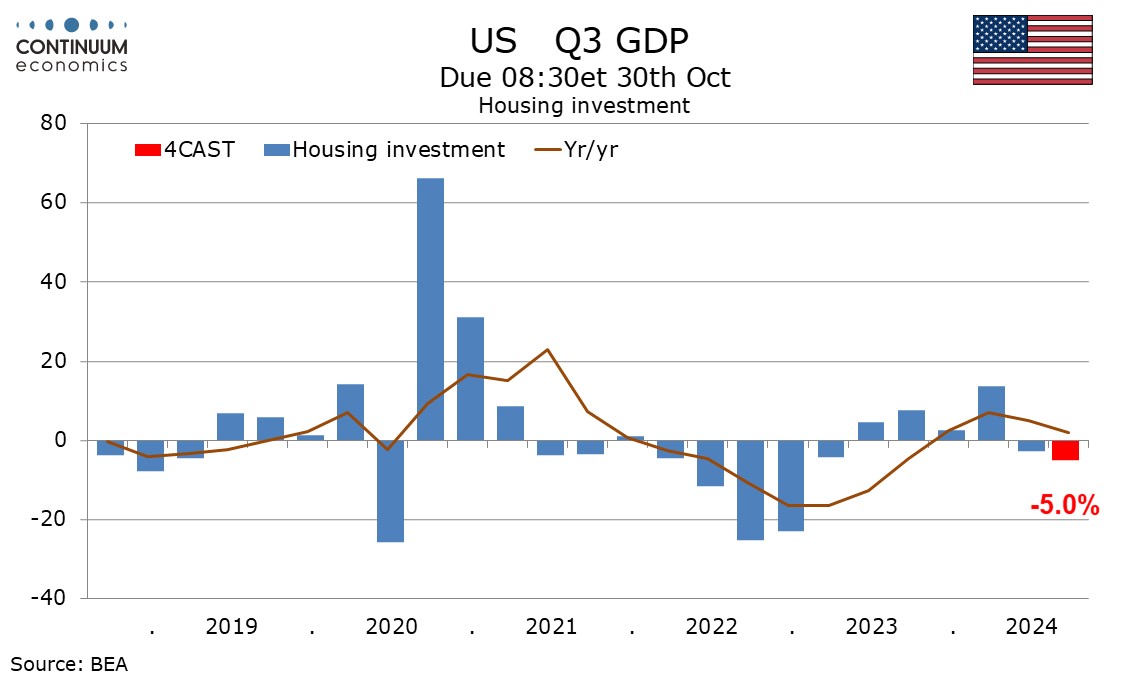

Weaker residential construction spending suggests a 5.0% decline in housing investment, despite some signs that housing demand started to pick up as the Fed started to ease.

Weaker residential construction spending suggests a 5.0% decline in housing investment, despite some signs that housing demand started to pick up as the Fed started to ease.

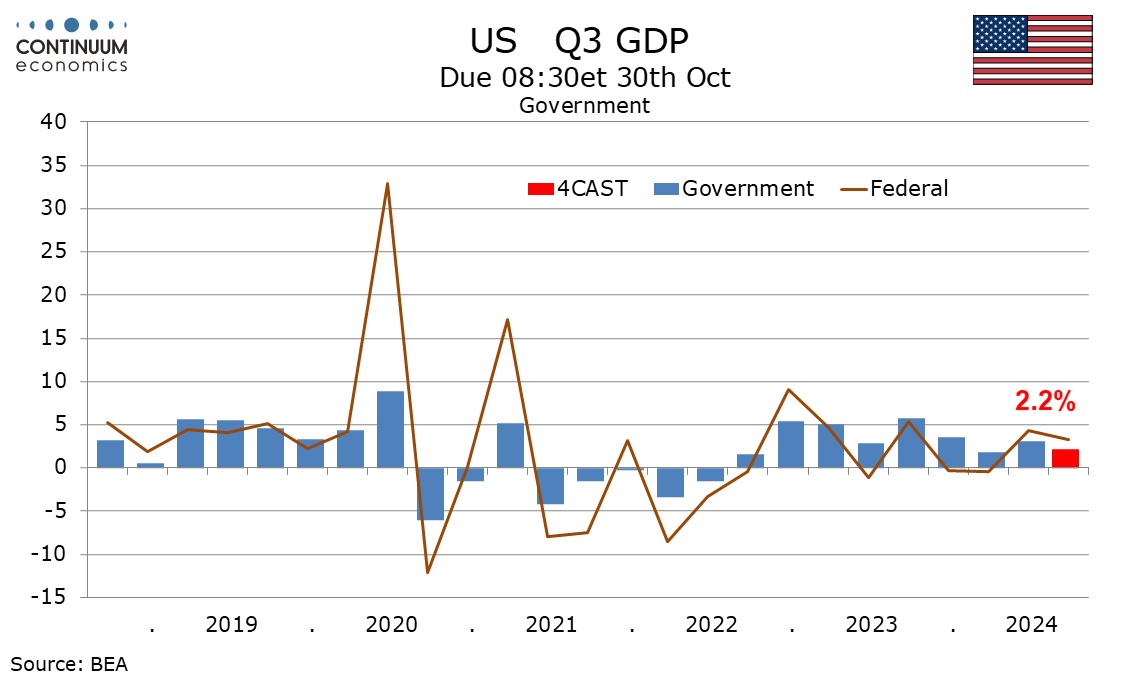

Public construction has also lost some momentum and we expect government to rise by 2.2%, down from 3.1% in Q1, though Federal spending is likely to remain firm, led by defense.

Public construction has also lost some momentum and we expect government to rise by 2.2%, down from 3.1% in Q1, though Federal spending is likely to remain firm, led by defense.

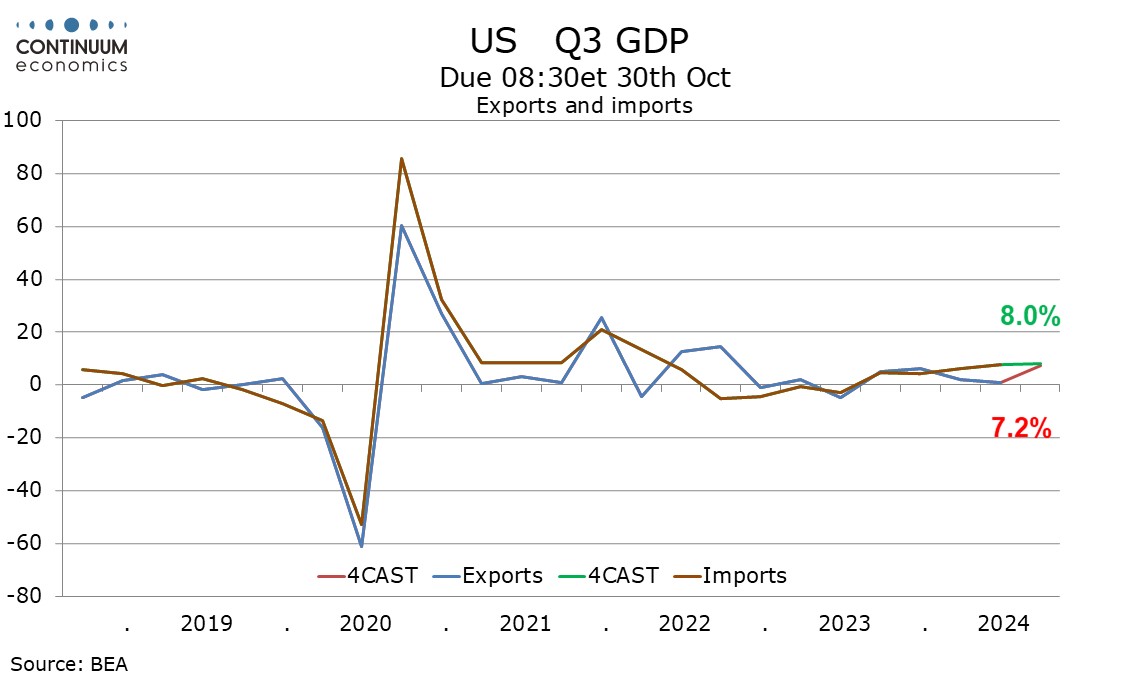

Exports are likely to see a healthy rise of 7.2%, but we expect imports to be stronger still at 8.0%, leading to a negative contribution from net exports. We assumed a wider trade deficit in September, which added to the downside risks in its recent release.

Exports are likely to see a healthy rise of 7.2%, but we expect imports to be stronger still at 8.0%, leading to a negative contribution from net exports. We assumed a wider trade deficit in September, which added to the downside risks in its recent release.

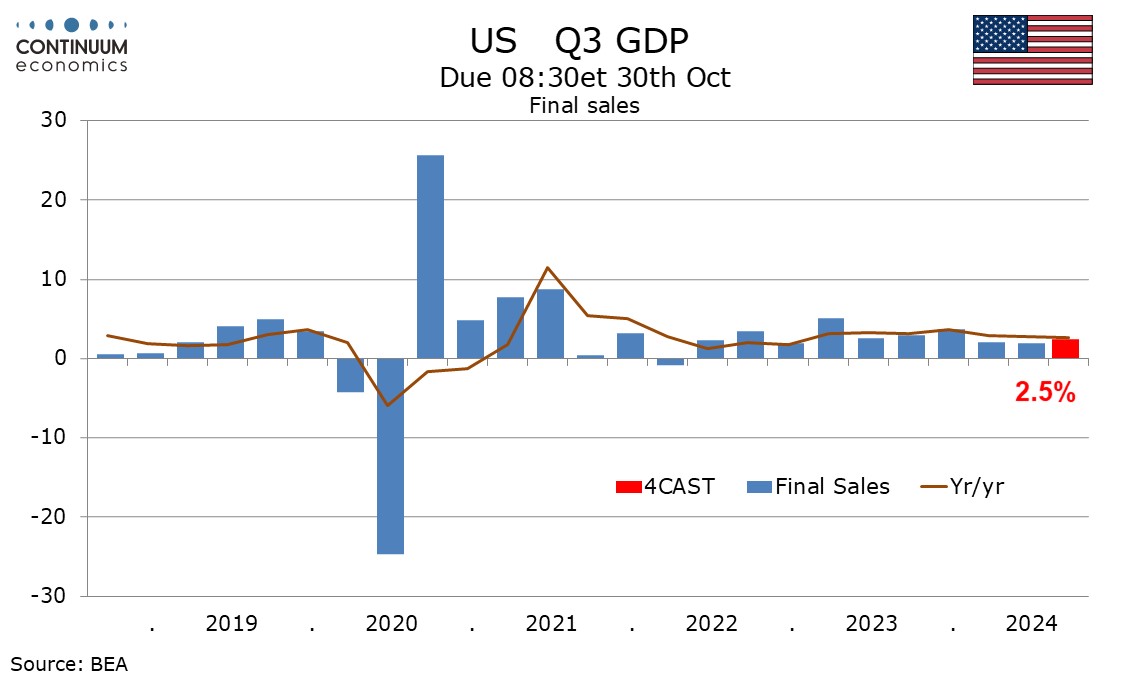

We expect final sales (GDP less inventories) to rise by 2.5%, slightly slower than final sales to domestic buyers but stronger than gains of 1.9% in Q2 and 2.1% in Q1.

We expect final sales (GDP less inventories) to rise by 2.5%, slightly slower than final sales to domestic buyers but stronger than gains of 1.9% in Q2 and 2.1% in Q1.

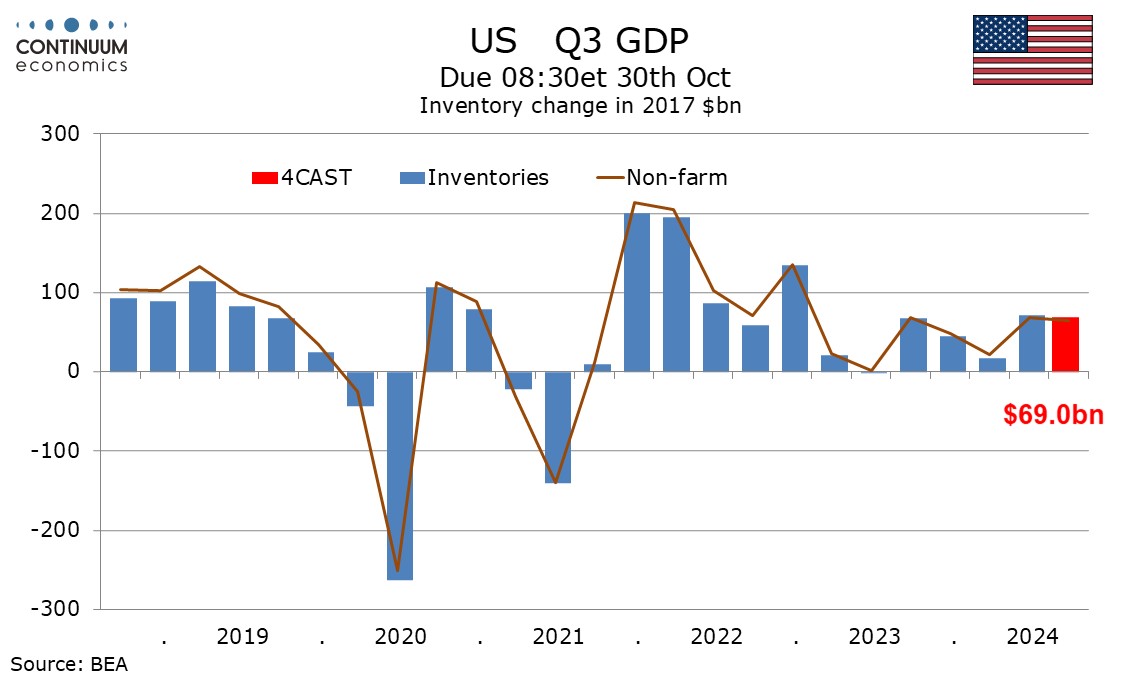

Inventory growth appears to be continuing at a similar pace to what was a significant acceleration in Q2, and we expect inventories to deduct only a marginal 0.1% from Q3 GDP.

Inventory growth appears to be continuing at a similar pace to what was a significant acceleration in Q2, and we expect inventories to deduct only a marginal 0.1% from Q3 GDP.

Underlying momentum still looks solid in Q3 but there are some downside risks in Q4 from a strike at Boeing, recent hurricanes and election uncertainty. Still, a move into recession looks unlikely.

Underlying momentum still looks solid in Q3 but there are some downside risks in Q4 from a strike at Boeing, recent hurricanes and election uncertainty. Still, a move into recession looks unlikely.