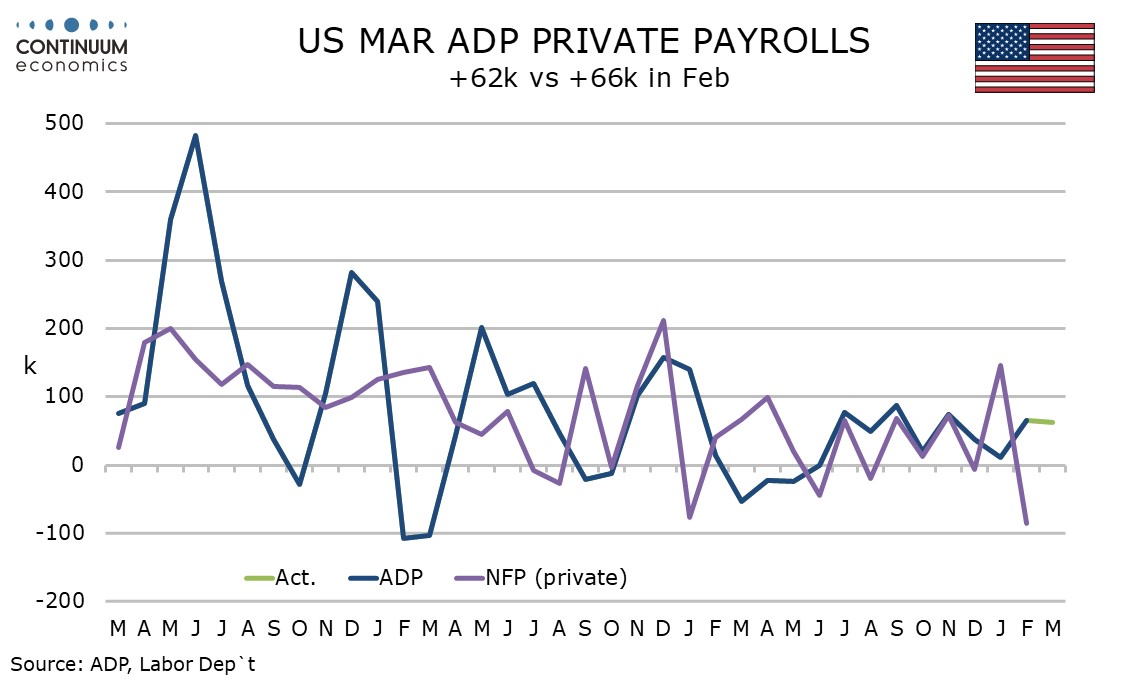

U.S. February Retail Sales and March ADP Employment resilient, but gasoline prices may undermine consumers

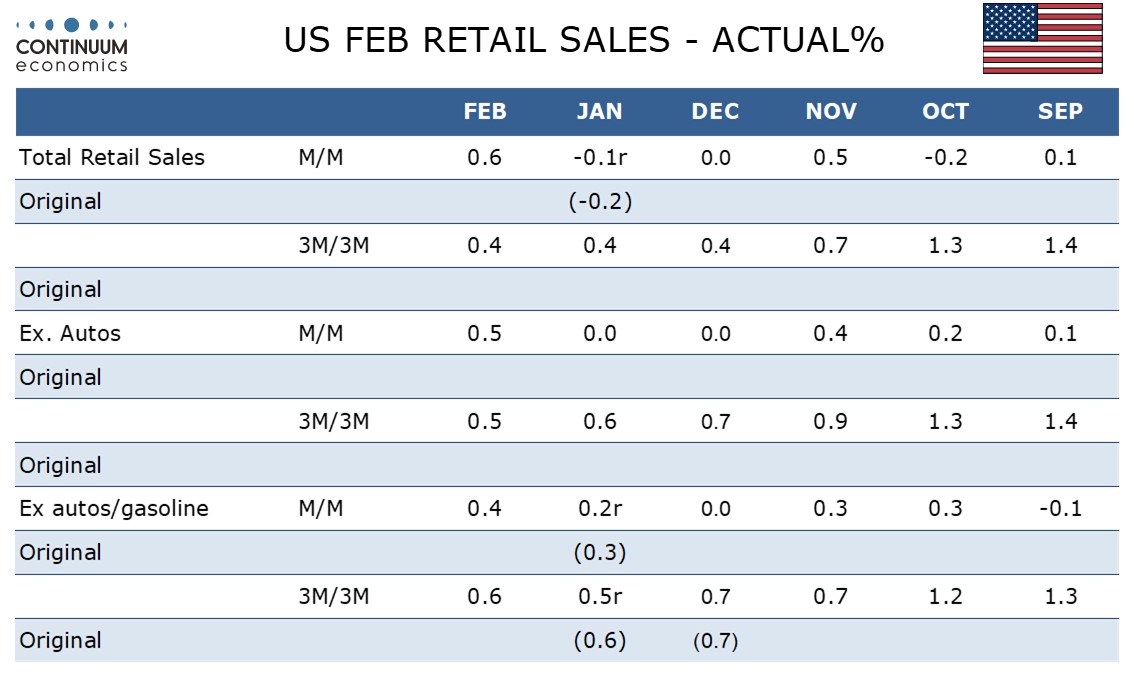

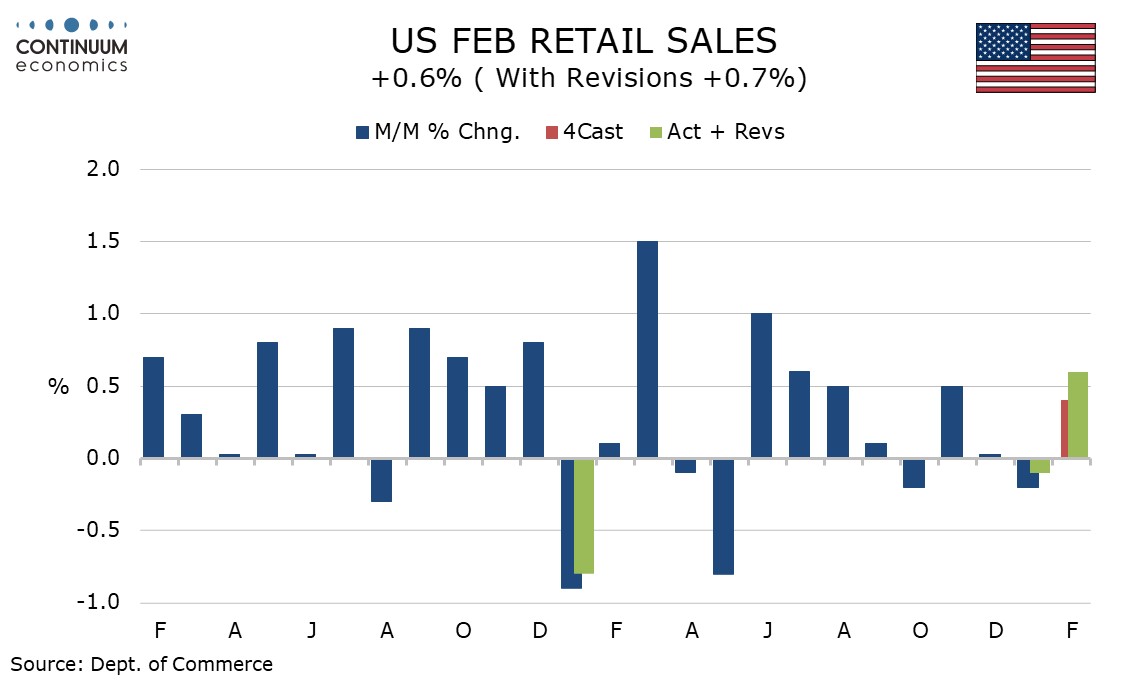

March’s ADP’s estimate of private sector employment of 62k is stronger than the market expected and similar to February’s 66k. February retail sales are also marginally firmer than expected, up by 0.6% overall, 0.5% ex autos and 0l;4% ex autos and gasoline. In March consumers will be dealing with a sharp rise in gasoline prices, which may undermine spending elsewhere.

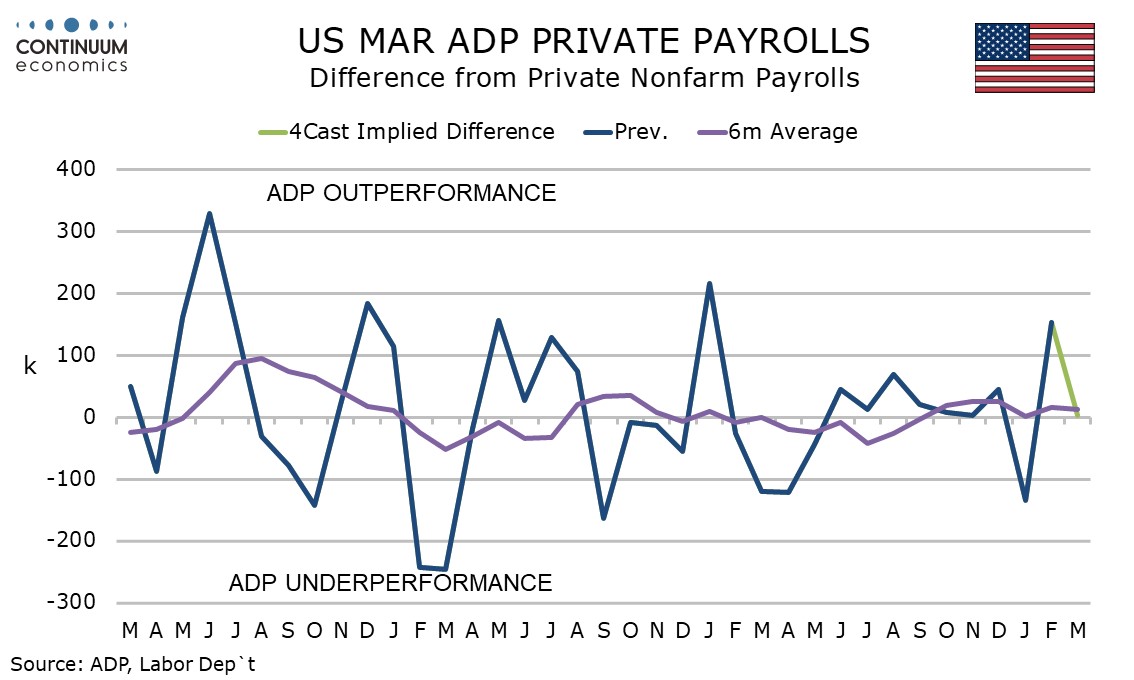

The ADP employment gains is similar to our upwardly revised forecast for private sector non-farm payrolls of 60k, though that will be lifted by 32k returning strikers. It was Friday’s strike report that saw us revise our payroll forecast up by 30k. We see overall payrolls up by 50k.

The ADP gain came largely from a 58k rise in education and health, where almost all the returning strikers are to be found. However with March’s ADP gain, both overall and in education and health, looking similar to February’s, it does not appear that the strikers were captured by the ADP data. Strikers were a restraint on February’s non-farm payroll, which underperformed the February ADP report, though that followed a sharp outperformance by the non-farm payroll in January.

Elsewhere in the ADP data there is a sharp 58k decline in trade, transport and utilities, and a fall of 11k in manufacturing. Construction saw an above trend rise of 30k which may reflect improved weather, while information and natural resources/mining both saw gains above 10k. The ADP gain was fairly evenly split between goods, up by 30k, and services, up by 32k.

Wage growth was unchanged at 4.5% yr/yr for job-stayers but for job-changers it bounced to 6.6% from February’s slower 6.3%, which can be seen as a positive sign.

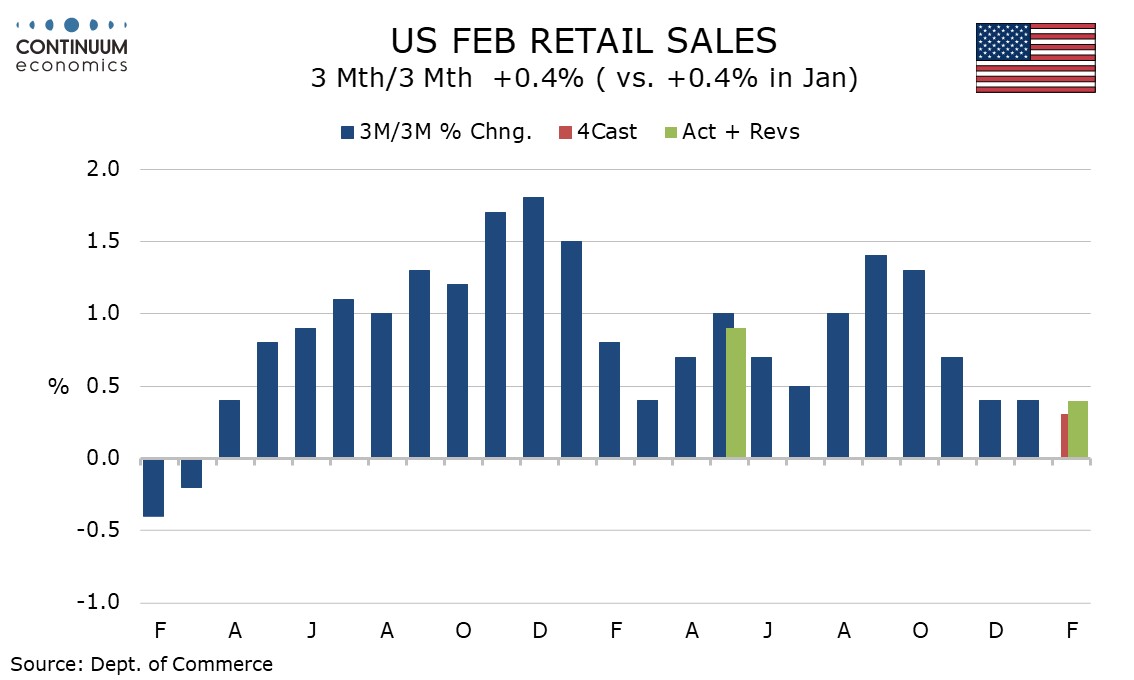

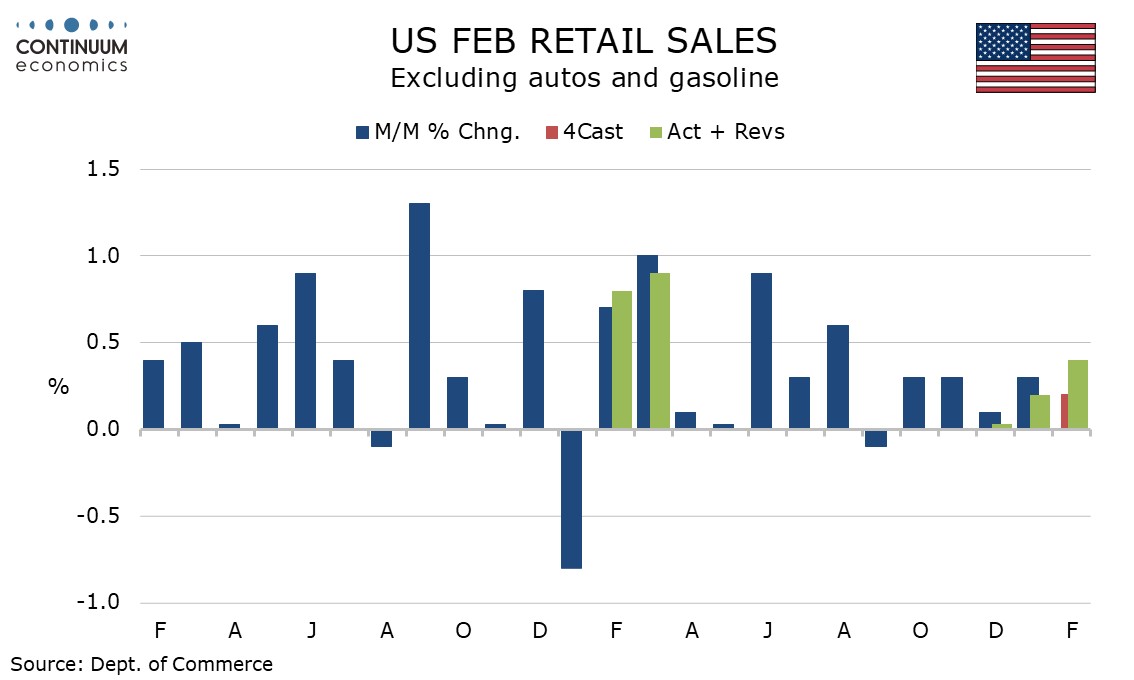

February retail sales are picking up from two straight near flat months, and the 3 month/3 month pace has slowed significantly in recent months, with the overall pace at only 0.4% in December, January and February, down from 1.4% in September. Ex autos the 3 month/3 month pace is 0.5% and ex autos and gasoline it is 0.6%.

The slowing in retail sales trend follows spending outperforming real disposable income in in the second half of 2025, though real disposable income in January got a lift from lower taxes. The boost from lower taxes is however likely to be offset in March by a surge in gasoline prices, which may keep trend in consumer spending subdued.

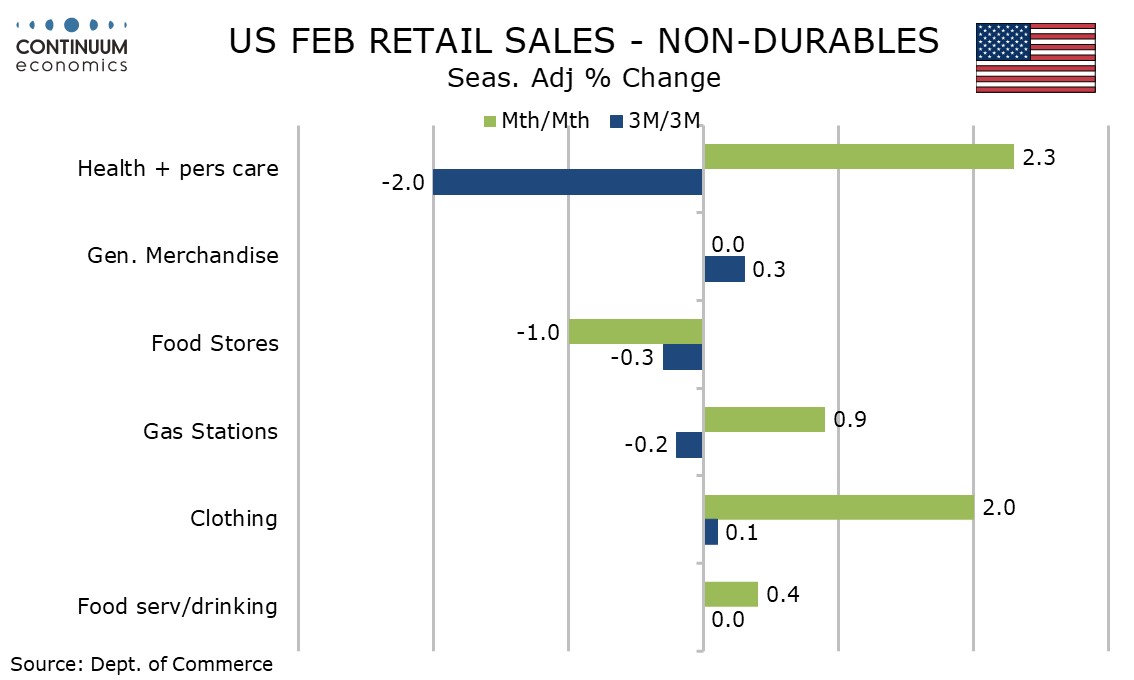

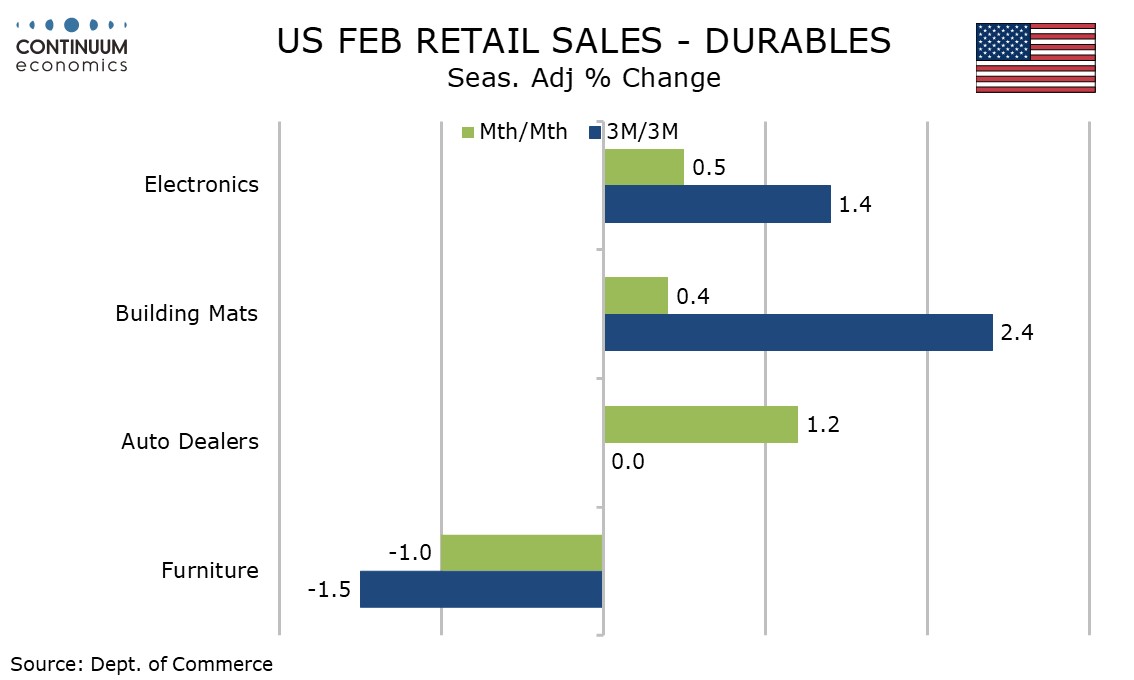

February’s retail sales gain saw modest positives from autos and gasoline after January dips but the main positive came from a 2.3% bounce in health and personal care which fell by 2.9% in January. Clothing with a 2.0% increase more than fully erased two straight preceding declines. February’s gain should be seen as largely corrective.

January and February data may both have been restrained by spells of cold weather and weather is likely to be more supportive in March. March may prove resilient to rising gasoline prices, but if the gasoline price rise is persistent, it is likely to weigh on consumer spending in Q2.