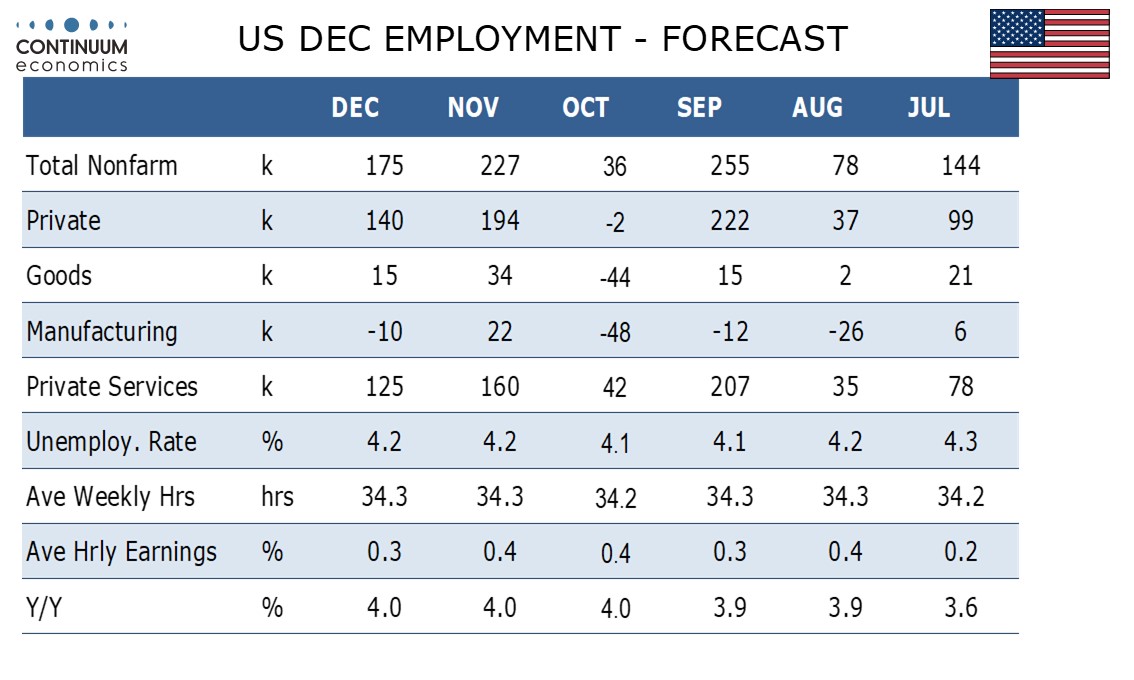

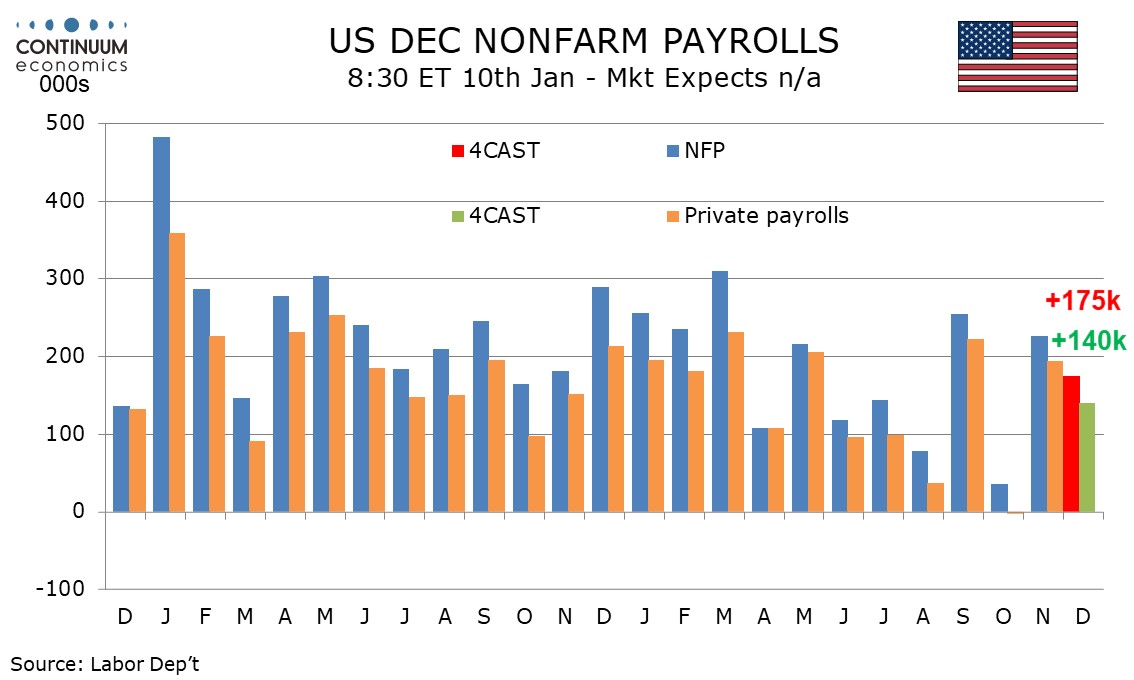

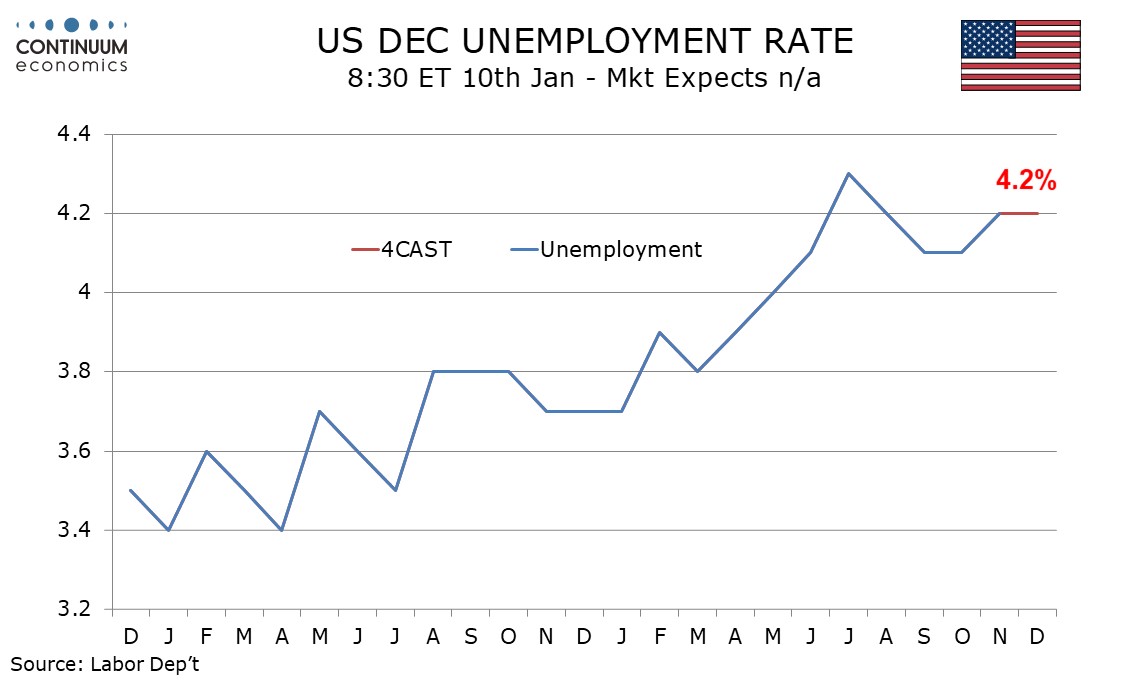

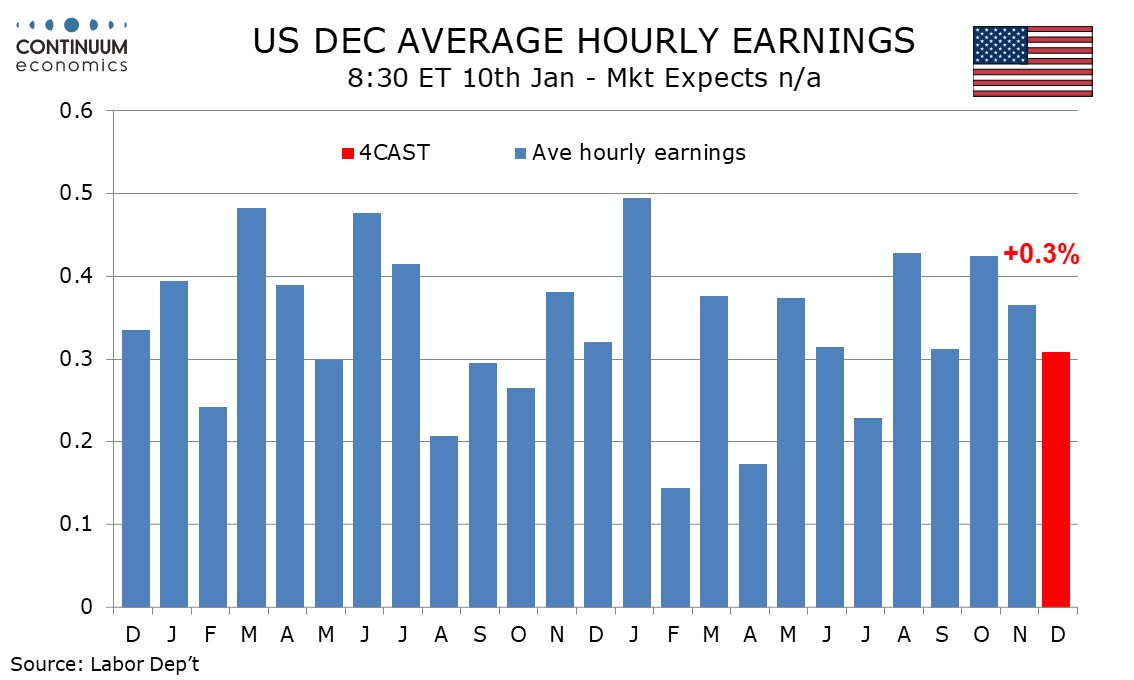

Preview: Due January 10 - U.S. December Employment (Non-Farm Payrolls) - Closer to solid underlying trend

We expect 175k increase in December’s non-farm payroll, with 140k in the private sector, a number that should be closer to underlying trend than a strong November and a weak October. We expect unemployment to be unchanged at 4.2% and average hourly earnings to slow to a 0.3% increase after two straight gains of 0.4%.

October’s 36k increase was restrained by hurricanes and a strike at Boeing and November’s 227k increase saw some catch up. Our forecasts are close to the 3-month averages of 173k overall and 138k in the private sector, though can be seen as positive given that the 3-month average includes September’s strong 255k increase but not August’s weak 78k.

The reason our forecasts are on the firm side of the 2-month and 4-month averages is that we see scope for a stronger rise in construction after two straight below trend gains totaling only 12k, and a rebound in retail after a 28k November decline.

We expect employment growth to exceed that of the labor force causing the unemployment rate to fall before rounding, but at 4.183% will still round to 4.2% after a November increase to 4.246%. Annual revisions will be seen to unemployment rates, which will probably be marginal, though it would not take much to see November revised up to 4.3%.

A 0.3% rise in average hourly earnings would be on the low side of trend after two straight slightly above trend gains of 0.4%. Yr/yr growth would then stand at 4.0% for a third straight month.

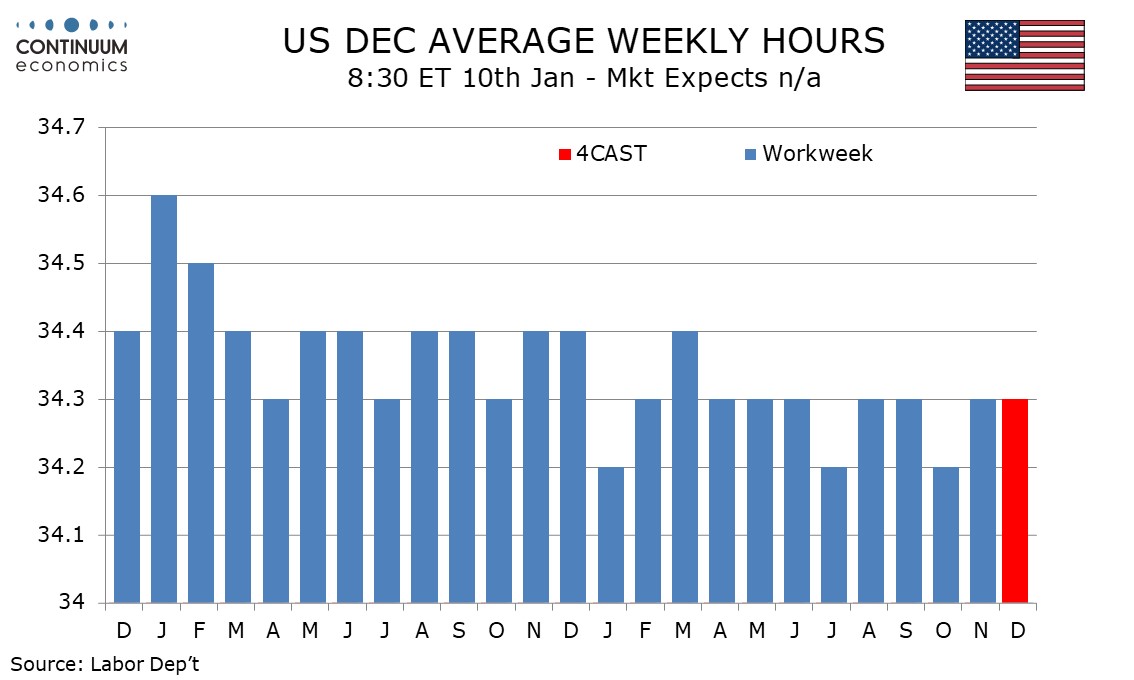

We expect an unchanged workweek of 34.3 hours, matching six of the last eight months and three of the last four, the exception being October’s hurricane-impacted reading. Aggregate hours worked would then rise by 0.8% annualized in Q4, up from 0.6% in Q3. Stronger GDP growth would require continued strength in productivity.