U.S. July Employment - Consistent with below potential growth, but not recession

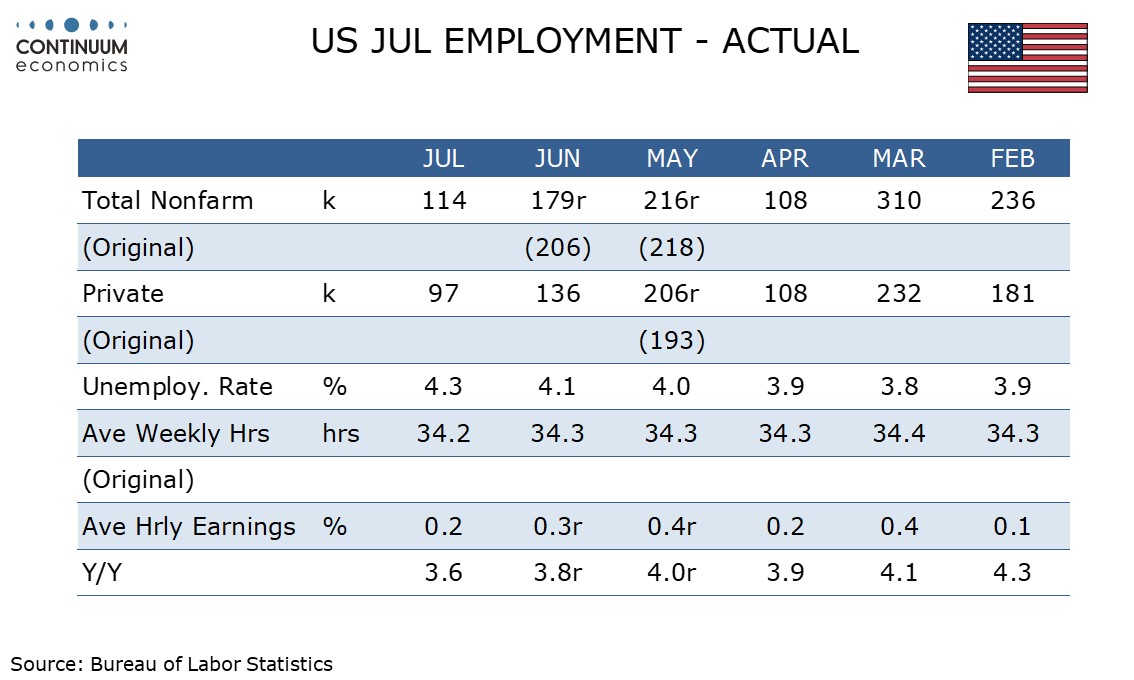

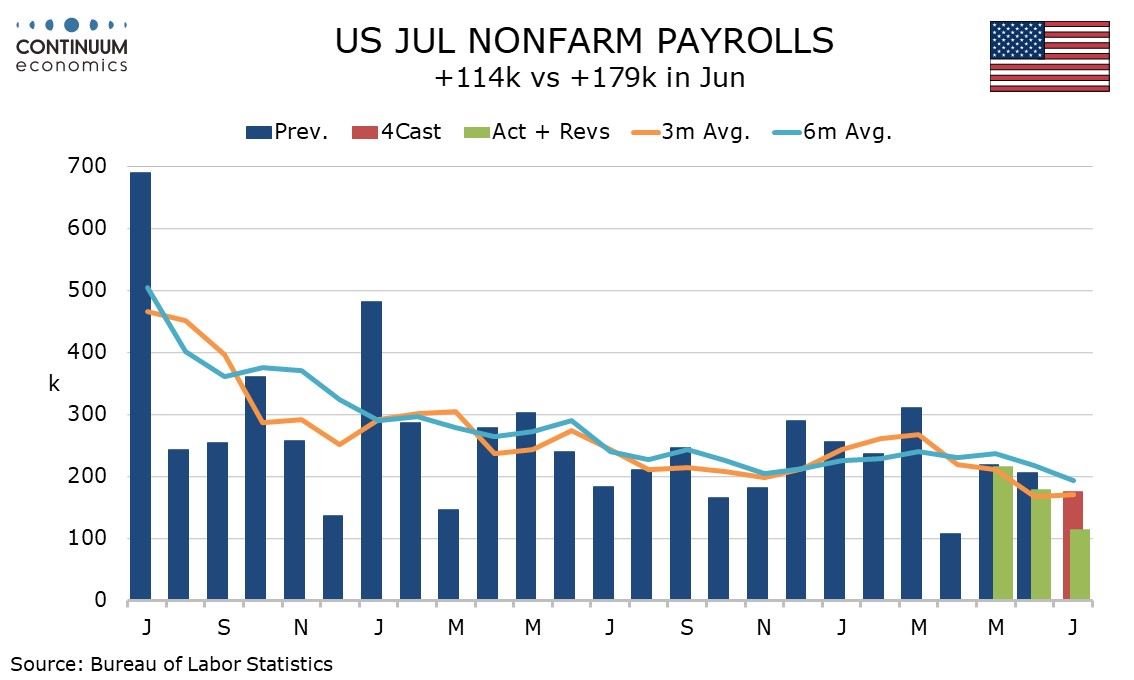

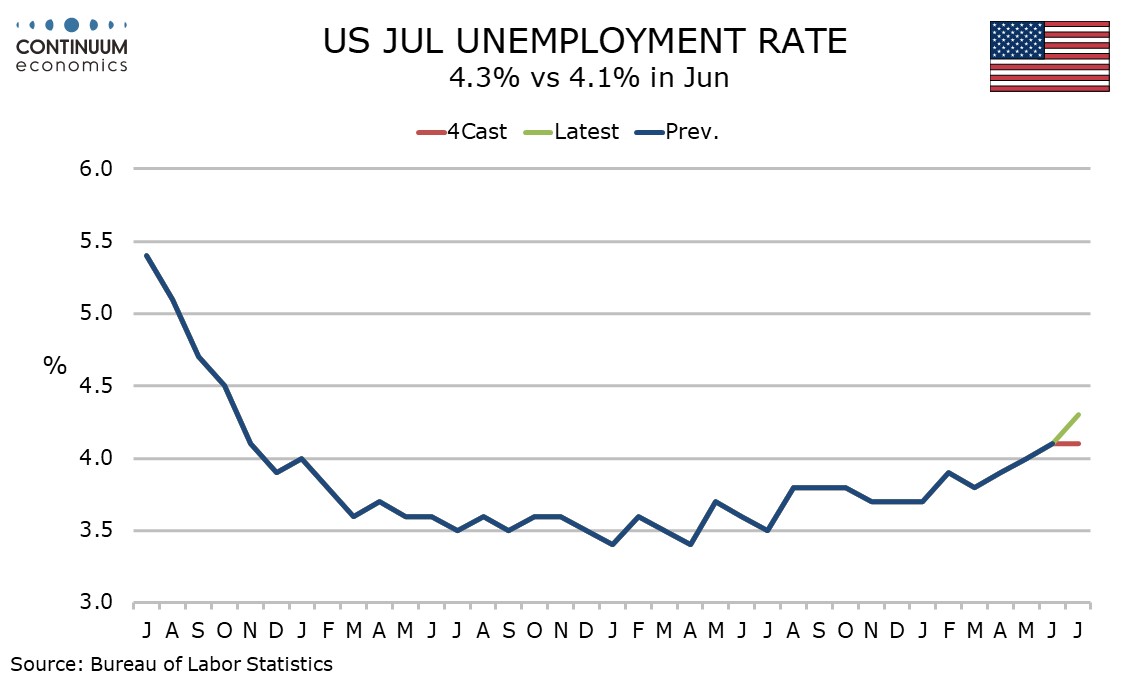

July’s non-farm payroll is weaker than expected with a 114k rise overall, 97k in the private sector, with weak details across the board, 29k in net negative revisions, a 0.2% rise in average hourly earnings, a lower workweek and a surprisingly sharp rise in unemployment, to 4.3% from 4.1%. A 25bps move is still the most likely FOMC September action, but more weak data could put 50bps on the table, and CPI data would have to be alarmingly strong to keep the FOMC on hold.

The data is consistent with below trend growth and rising unemployment rather than recession, though it is possible weakness was exaggerate by Hurricane Beryl, which hit around the time of the survey.

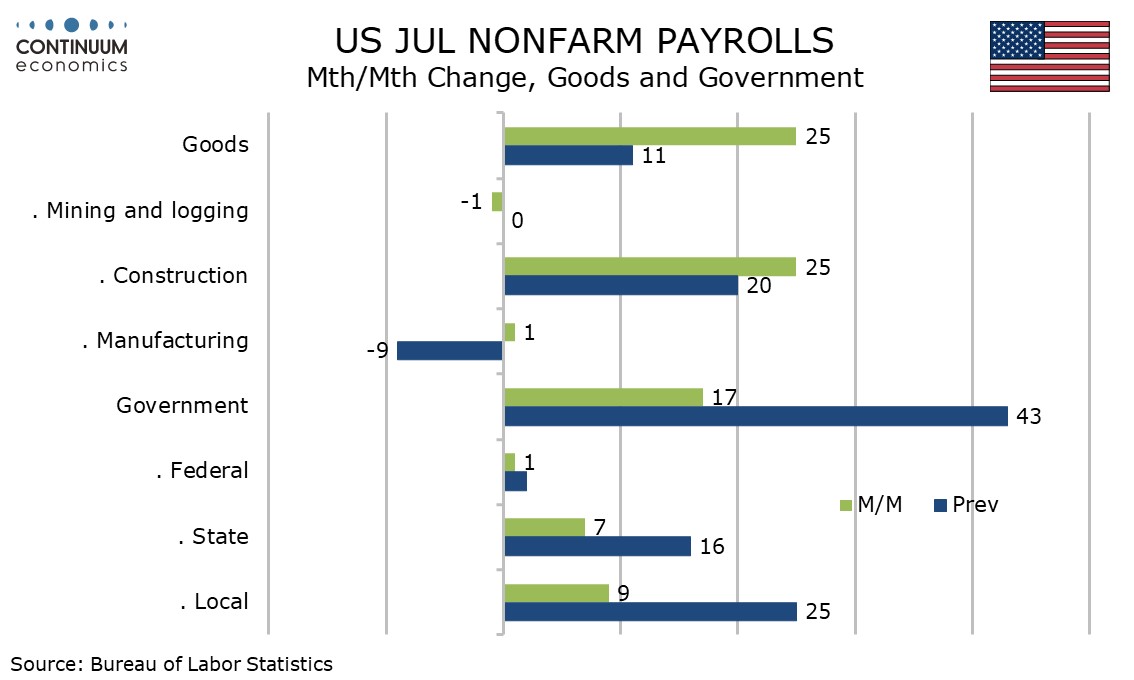

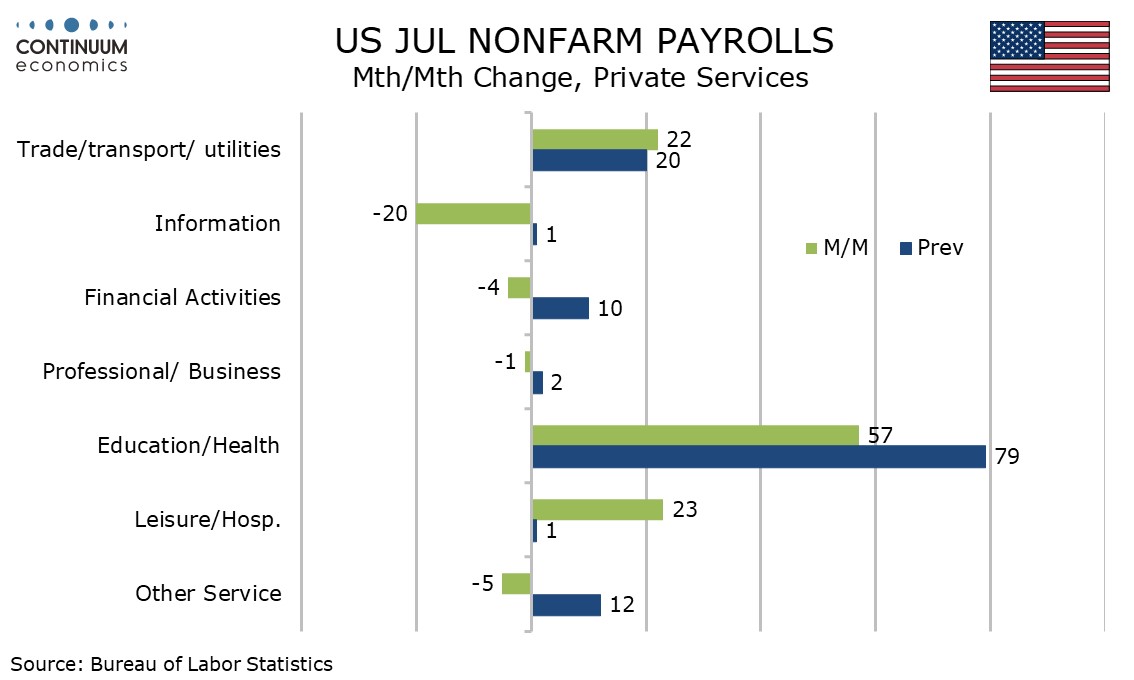

The employment details however do not suggest a strong impact from weather, with two of the more weather-sensitive components, construction with a rise of 25k and leisure and hospitality with a rise of 23k being relatively resilient.

The employment details however do not suggest a strong impact from weather, with two of the more weather-sensitive components, construction with a rise of 25k and leisure and hospitality with a rise of 23k being relatively resilient.

Information at -20k was most clearly below trend. Health care and social assistance continues to lead job growth, but at 64k was below recent trend.

The overall payroll increase is the weakest since April and the private sector gain the weakest since October 2023, which is not a conclusive sign of a sharp change in trend.

The overall payroll increase is the weakest since April and the private sector gain the weakest since October 2023, which is not a conclusive sign of a sharp change in trend.

The rise in unemployment will be of particular concern to the Fed, with the rate the highest since October 2021. However the detail shows the rise led by an unusually strong 420k increase in the labor force. The household survey’s estimate of employment growth at 67k was weaker than the payroll, but not dramatically.

The rise in unemployment will be of particular concern to the Fed, with the rate the highest since October 2021. However the detail shows the rise led by an unusually strong 420k increase in the labor force. The household survey’s estimate of employment growth at 67k was weaker than the payroll, but not dramatically.

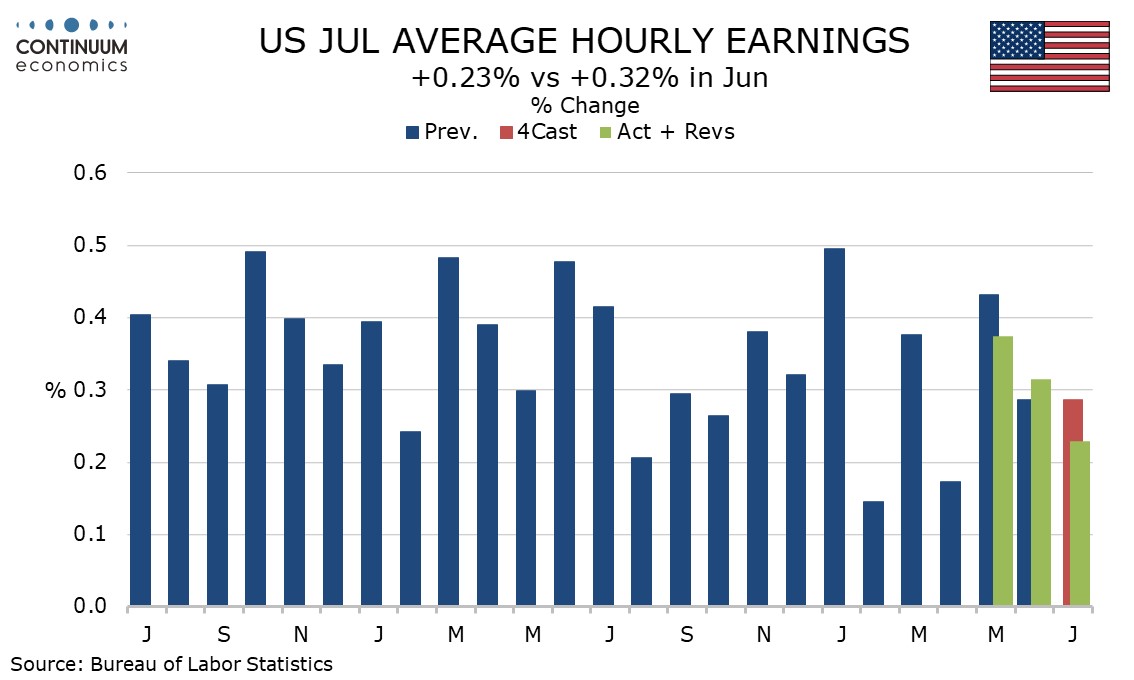

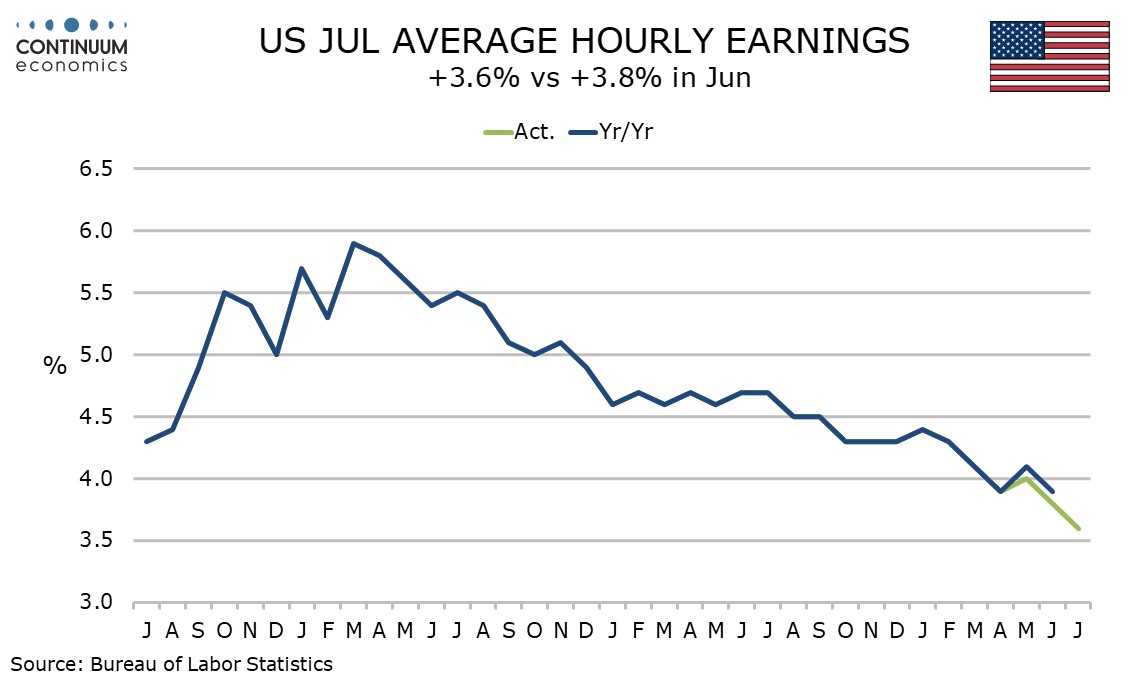

Average hourly earnings rose by 0.23% before rounding below trend if not dramatically with near neutral net revisions. Yr/yr growth of 3.6% from 3.8% is the weakest since April 2021, and if productivity continues to rise can be seen as consistent with near target inflation.

Average hourly earnings rose by 0.23% before rounding below trend if not dramatically with near neutral net revisions. Yr/yr growth of 3.6% from 3.8% is the weakest since April 2021, and if productivity continues to rise can be seen as consistent with near target inflation.

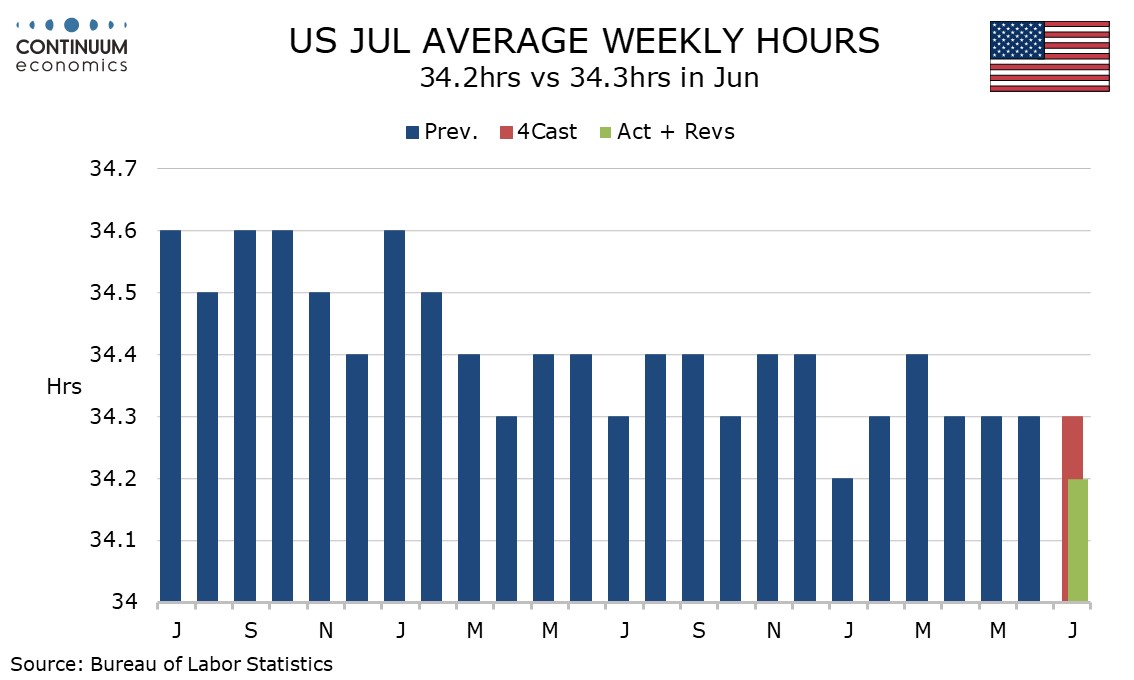

The workweek at 34.2 hours from 34.3 is the weakest since January, though Hurricane Beryl may have been a factor, and weather was seen as a factor depressing January data too.

The workweek at 34.2 hours from 34.3 is the weakest since January, though Hurricane Beryl may have been a factor, and weather was seen as a factor depressing January data too.

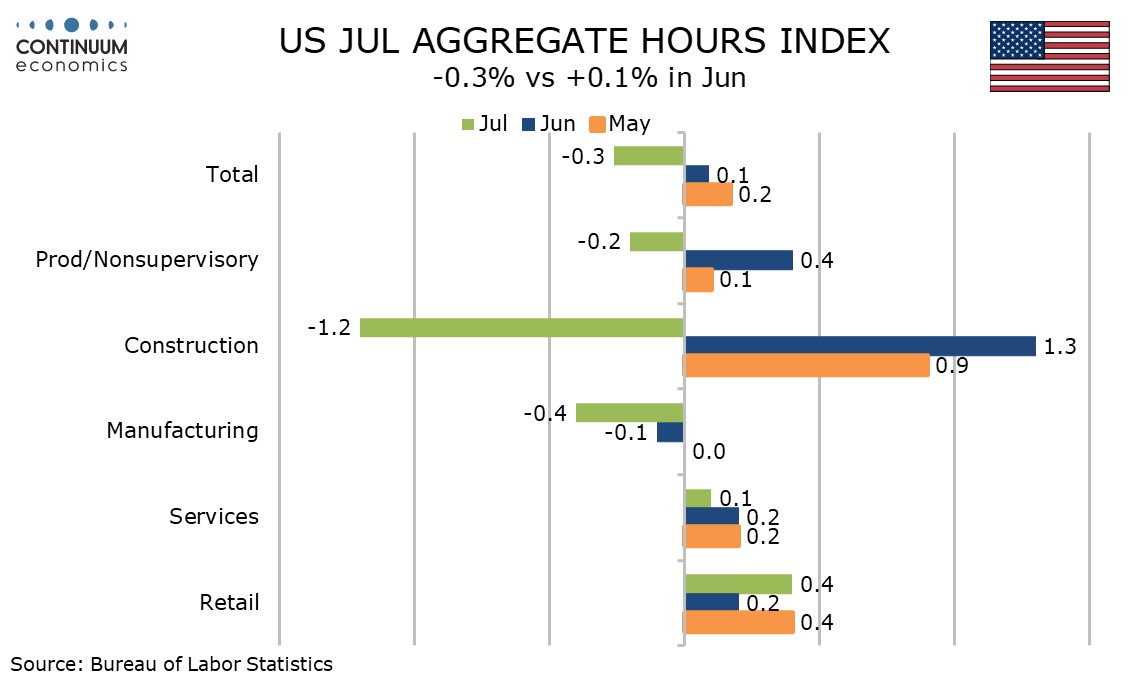

Aggregate hours data did show weather-sensitive construction particularly weak at -1.2% compared with -0.3% overall, though construction was coming off a strong rise in June. Manufacturing fell by 0.4% but private services managed a modest 0.1% increase.

Aggregate hours data did show weather-sensitive construction particularly weak at -1.2% compared with -0.3% overall, though construction was coming off a strong rise in June. Manufacturing fell by 0.4% but private services managed a modest 0.1% increase.

The data strengthens the case for Fed easing in September though we will still have August payroll data to see before the FOMC next meets as well as July and August CPIs. Given that unemployment is now trending higher however, CPI will probably have to significantly surprise on the upside to keep the Fed on hold. More surprisingly weak data could put a 50bps move on the cards.

The data strengthens the case for Fed easing in September though we will still have August payroll data to see before the FOMC next meets as well as July and August CPIs. Given that unemployment is now trending higher however, CPI will probably have to significantly surprise on the upside to keep the Fed on hold. More surprisingly weak data could put a 50bps move on the cards.