Eurozone Data Preview (Jul 30): Fading Momentum?

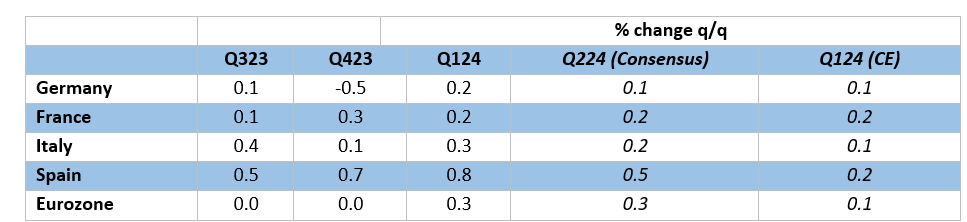

According to revised official national accounts data, the EZ economy actually avoided what was previously suggested to have been a modest recession in H2 last year. Moreover, the economy sparked back in Q1, albeit against a backdrop of marked, if not increasing, national growth divergences but where the outcome exceeded expectations. Indeed, Q1 GDP rose by 0.3% q/q, three times the ECB estimate and where even Germany saw a return to positive growth. However, real GDP was bolstered afresh by weaker imports, working day effects and unseasonable weather and where a weak capex backdrop in Q1, these hardly a result of improving fundamentals. But it seems that such GDP growth rates continued into the last quarter, with the ECB suggesting a pick-up to 0.4%. We think that this is too high and doubt whether it will persist, given both weaker survey data into this quarter and official data featuring continued manufacturing and construction softness. Indeed, amid the 0.1% pace we envisage will be more national divergence (Figure 1) and to a degree that downside real activity risks may be both increasing (Figure 2) and materializing, issues that may accentuate disinflation trends and add to monetary easing rationale.

Figure 1: Divergent EZ GDP Picture Less Clear in Q2?

Source: Eurostat, Continuum Economics, Bloomberg

Geographical Disparity Continuing?

The weakness in domestic demand persisted, if not deepened, in Q1, with a drop in imports masking a small drop in government spending and further inventory shrinkage – we think the latter is normalizing in the holding of stocks rather than presaging any intentional inventory rebuild into H2. As a result, we would not read too much into any apparent ‘strength’ in the Q1 GDP numbers. As an aside, the data in Q1 reflected marked divergences among the EZ economies, most notably among the ‘Big 4’. Spanish GDP growth picked up to a revised 0.8% q/q. But the fact that Q1 saw all of the Big 4 returning to growth, the key being how any such momentum spills over into the rest of 2024 – and beyond.

This can be partly answered by looking at recent actual monthly data for Q2 and (at least for survey numbers) into the current quarter. They very much suggest continuing weakness and declines in manufacturing and construction, but with momentum evident in services – the former hardly implying and inventory rebuild. Indeed, official data on services output suggest a very upbeat Q2 outcome, but this is purely on the basis of April data which may have been boosted by aberrant factors such as the timing of Easter. This is something certainly suggested by business survey data whether they be PMI numbers or those offered by the European Commission, with a clear loss of GDP momentum being signaled into the Q3.

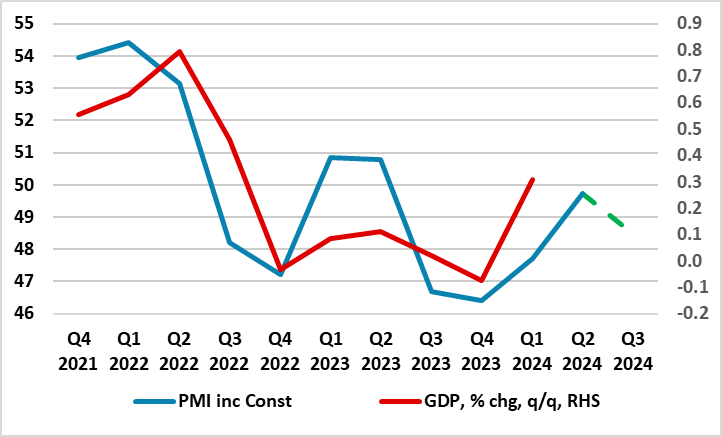

Such a backdrop may perturb some Council members who may still be wary that the ECB’s recently upgraded growth forecasts are still too optimistic, they being reliant on annualized goth of well over 1.5% through the rest of 2024. Admittedly, we have repeatedly cautioned about taking much from PMI readings not least given the misleading picture it has offered in the past regarding actual EZ GDP swings and its conflict with much and persistently weaker European Commission survey data (Figure 2). This may be partly a result of its limited geographical coverage and its lack of account of the construction, retail and government sector readings – all volatile but also very rate sensitive. Indeed, the broader based European Commission business and consumer survey data is telling a much different story, having slipped afresh and remains much more with contraction territory. In addition, the weakness in domestic demand (most notable in the form a fresh drop in Italy and seemingly still in Germany) is important as it accentuates the disinflation backdrop still coming through. This clearer disinflationary backdrop, is, however, something that the business survey data also highlight – the recent July PMI numbers noting ‘companies raised their selling prices at a softer pace. In fact, the pace of charge inflation was the slowest since last October’.

ECB Optimism Overdone

Thus we remain of the view that the ECB is still too optimistic regarding real economy prospects, even though our existing 2024 GDP estimate of 0.5% may need some reassessment, but where we see the ECB outlook of 0.9% this year and 1.5% 2025 look like being undershot. This reflects not least as nowhere near the full extent of its policy tightening has filtered through yet, this formal hiking being accentuated both by the ECB balance sheet shrinkage and by credit standards being raised by the banking sector. But the ECB has been very aware of a still very weak credit and bank deposit backdrop, this very much being compounded by fiscal consolidation. Indeed, the European Commission is suggesting both more and faster such consolidation it having out several EU counties under excessive deficit surveillance. Furthermore, on the monetary side, the continued planned shrinkage in the ECB monetary policy asset portfolio will have a further negative impact on banks’ financing conditions and liquidity position, resulting in a moderate tightening of terms and conditions and a negative effect on lending volumes. Importantly, continued weakness in consumer borrowing (still running at just 0.3% y/y and very negative in real terms) is hardly evidence of the consumer recovery that is the mainstay of ECB growth thinking.

Figure 2: Business Surveys Suggest Flagging Momentum

Source: Markit, European Commission

Flash GDP in Perspective

Amid a paucity of reliable data, but as we have underlined before, it is important to recognize that there are clear shortcomings to the flash estimate for EZ GDP. No details come with these flashes and they are prone to clear revisions. They are based on incomplete activity numbers with usually on one monthly vale for services and two for construction and manufacturing. This may be why the ECB is openly more focused on survey data, especially as it is more timely. Time will tell whether the Q2 flash numbers will tell any more authoritative a story! Regardless, the apparent resilience in overall GDP makes the sharp and broad fall in inflation all the more likely to have been driven more by supply factors than demand. But with demand now seemingly buckling (the PMI noted that new orders fell for the second month running and business confidence dropped to a six-month low, leading firms to halt a spell of hiring which began at the start of 2024) the disinflation process may have much further to run.

Policy Outlook

Regardless, we still feel that neither Fed policy, nor the US$, are likely to delay any further ECB move(s). Instead, and partly as the ECB remains focused on the labor costs updates, numbers produced quarterly, but also wants to amass a broad but fresh thrust of added insights, then subsequent rate cuts may only arrive in three-month intervals, ie September and December. This schedule also chimes with updated ECB projections. Hence, our long-standing view that the ECB may cut only a further 50 bp this year and we see 100 bp further easing through 2025, with the deposit rate then nearing 2% and thus more in line with a perceived neutral setting but hardly moving into a clear expansionary stance. But if the slowing economy backdrop becomes more discernible, then the ECB may ci faster and more sizably!