Eurozone Banks See Company Loan Demand Slump as ECB Unconventional Tightening Bites Further

While there may be few positive straws in the wind in the latest (April) 2024 bank lending survey (BLS), the ECB should fund the balance of results still troubling. Company credit demand slumped afresh amid rising interest rates and deferred capex plans. Admittedly, credit supply to firms tightened only moderately further but still added to the marked rise in recent quarters Figure 1). There was a positive in a fall in credit standards for mortgage lending but this was almost exclusively a French rather than EZ-wide development and came alongside still falling demand (amid what are now falling EZ house prices). The data certainly back the case for some ECB rate cutting, but this is going to have only a gradual and partial impact as the BLS makes clear that ongoing central bank balance sheet reduction has continued to exert tightening pressures and the ECB has no plans (yet) to slow, let alone stop its unconventional tightening regardless of what and when its reduces official rates. It could be argued that if the ECB purses further balance sheet reduction, then larger/faster conventional easing may be needed!

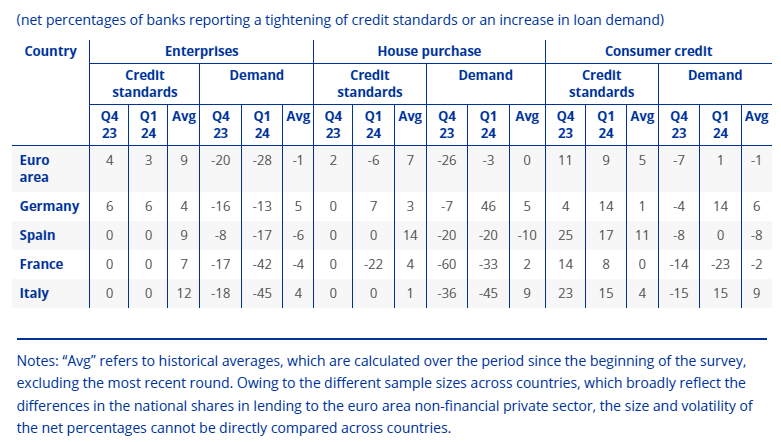

Figure 1; Banks Still Seeing Company Credit Supply Slipping as Demand Drops Further

Source; ECB,

Balance Sheet Reduction Biting

The ECB unconventional policy is clearly biting, something we have long argued has been accentuating the conventional rise in interest rates and has been visible in both the slump in bank deposits and credit levels of late. Indeed, the BLS specified that the reduction of the ECB’s monetary policy asset portfolio had a further negative impact, resulting in a moderate tightening of terms and conditions and a negative effect on lending volumes. EZ banks also indicated that the phase-out of the third series of targeted longer-term refinancing operations continued to negatively affect banks’ liquidity positions. Reflecting the very significant repayments made since November 2022 and the comparatively small remaining outstanding amounts of TLTRO III, banks reported only a small tightening impact on their overall funding conditions and a neutral effect on lending conditions.

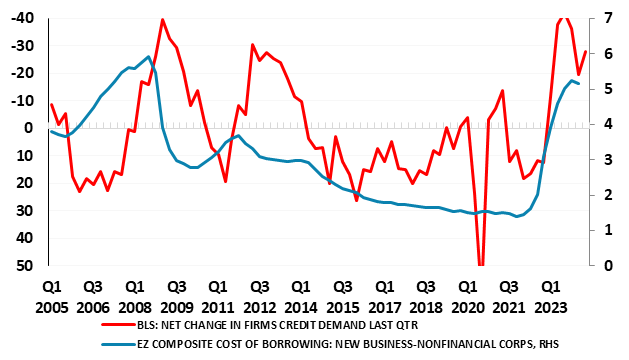

Figure 2; Company Credit Demand Drops Further as Rates Rise

Source; ECB

Still Falling Credit Supply

In regard to credit supply, which has fallen markedly of late thereby compounding the impact of arise in the costs of credit, EZ banks reported a small net tightening of their credit standards – ie banks’ internal guidelines or loan approval criteria – for loans or credit lines to enterprises in the first quarter of which was less than banks had expected in the previous round. Notably, banks, for the first time since end- 2021, reported a moderate net easing of their credit standards for loans to households for house purchase whereas credit standards for consumer credit and other lending to households tightened further. Risk perceptions continued to exert tightening pressures across all loan categories, while competition and, for housing loans, also banks’ risk tolerance, contributed to an easing of credit standards, this all the more surprising given growing signs of falling EZ house prices.

Perhaps more troubling given the implications for reduced credit supply, banks reported a further net increase in the share of rejected loan applications for firms all of which added to the increases seen since the first quarter of 2022. The further increase in the share of rejected company loan applications was driven by Germany. Admittedly somewhat smaller, Banks reported a further net increase in the share of rejected applications for housing loans.

Fragile Loan Demand

As for demand, banks reported an unexpected and much more substantial decline in company loan demand (Figure 2) alongside a small decline in demand for housing loans, while demand for consumer credit and other lending to households was reported as broadly stable. As has been the case in recent quarters, higher interest rates, as well as lower fixed investment for firms and lower consumer confidence for households, exerted dampening pressure on loan demand.

Policy Considerations

For ECB hawks who have suggested that the fall in market interest rates in the last few months (admittedly much of which has reversed most recently) constitutes an easing in financial conditions, the BLS points very much in the opposite direction. In addition, ECB unconventional policy is biting, acting to reduce the supply of credit and raise its costs. As for credit supply, the further net rise in credit standards adds to the substantial cumulative tightening since 2022, which has contributed, together with weak demand, to the strong fall in loan growth to firms and where there has also been a marked cumulative fall in credit demand. But the BLS very much underscores that the impact of past tightening will continue to dampen loan growth in the coming quarters, not least as more tightening in credit standards (less credit supply) is expected through the current quarter. The BLS will add to the ECB dovish case and will feature strongly in the Council debate this week that will include minority) demand for immediate easing. The question is whether ECB attention should/will shift to its balance sheet plans in due course too!