ECB Minutes; Rate Cuts Seen But Not Heard?

In the press conference following the Dec 14 ECB Council meeting, President Lagarde was adamant that ‘we did not discuss rate cuts at all. No discussion, no debate on this issue’. But the just-released account of the meeting suggest that rate cuts may not have been formally spoken about, but the issue was lurking is member’s minds. Indeed, the interest rates embedded in the staff projections – which may have laid above market interest rate thinking but still pointed to some 130 bp into 2025 –suggested that the rate path was in line with reaching the inflation target in H2 2025. Moreover, there was early but clear discussion of the factors and the timing (ie this summer) the Council would need in order to believe inflation was falling on a permanent basis. There was also continued uncertainty about how hard the monetary policy transmission mechanism may be working.

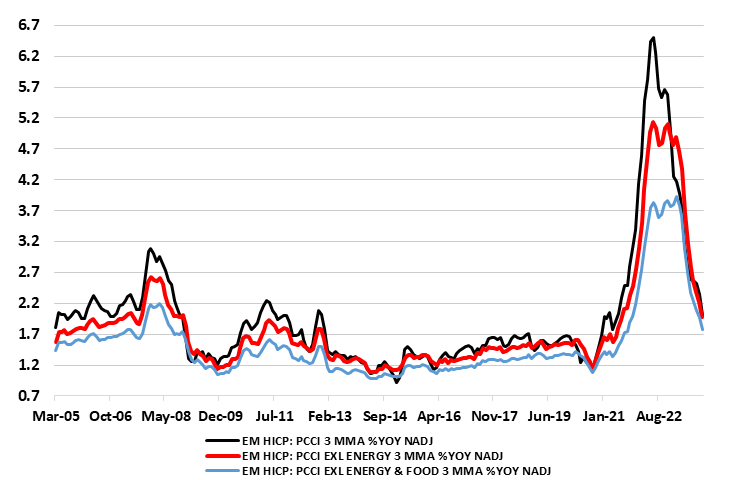

Figure 1: Persistent Price Pressures Falling Faster On Core Basis

Source: ECB, Persistent and Common Component of Inflation (PCCI)

Too Optimistic?

Within the Council, it was argued that the December staff projections for growth in the near term might be too optimistic overall, not least given that mechanical now-casting tools continued to point to slower economic activity and the possibility of a technical recession. Indeed, it was noted that the Consensus Economics forecast for GDP growth was also significantly lower for 2024 than the equivalent staff projection. Most of the ECB’s expected growth in 2024 hinged on an increase in consumption and that has an array of downside risks, the latter explaining our below-consensus thinking!

Policy Transmission Confusion

Somewhat puzzlingly, some suggested that there were several reasons why the transmission of monetary policy remained uncertain and might be less powerful than suggested by historical patterns and models. This line of argument conflicted with the alternative view (with which we concur) that there were signs of “over-tightening” in the banking sector, reflecting the dual effect of higher policy rates and lower deposits amid a declining supply of liquidity. Moreover, it was argued that a significant part of the interest rate pass-through was still pending, with the overall peak impact on activity seen in early 2024 and the bulk of the impact on inflation still expected over the next two years. The view was expressed that transmission to financing conditions and lending activity was working more strongly than initially expected and non-linearities or financial amplification could be at work.

The Inflation Backdrop and the Emergence of the Summer Schedule

The latest inflation numbers were e to be treated with caution, and it was too early to be fully confident that inflation would return to target was the overall view. More data were needed to confirm the decline, in particular data on wage growth, which were only expected in the spring of next year. As negotiations on many wage agreements would only be concluded early next year, members did not expect substantial hard evidence corroborating the projected moderation of wage growth to be available before the middle of the year, this having more recently having translated more formally to the ECB saying it is not thinking if any easing until this summer. This disinflation to date was indicative of weak demand and reflected the impact of monetary policy as well as diminishing effects from other factors that had been pushing inflation up. We would suggest the very opposite as supply has been the main factor and demand weakness has yet to come though appreciably. Indeed, improved supply conditions may explain why persistent price pressures have fallen so clearly and why the drop is steepest in regard to core prices (Figure 1).

But the inflation numbers are already making us more confident that the headline rate may fall to below the 2% target in Q2, thereby corroborating a disinflation trend already evident in seasonally adjusted m/m core and headline numbers, data we have been flagging for some time. And it does seem as if the ECB is starting to use such numbers as the Dec account mentions, albeit using a 3 month on 3 month annualized measure that very much lags the more coincident 3 month moving average we prefer. In this regard, it is notable that the ECB acknowledged that these were often better predictors of future inflation than annual growth rates and had already pointed to below target inflation.

At the same time, it was pointed out that lower inflation was so far not fully reflected in the perceptions of firms and the general public, so it should not be taken for granted that lower inflation figures would immediately translate into lower wage demands. This is not the case as the European Commission survey data shows consumer price expectations now at half their long-term average. There was also a debate about getting inflation down further using the so called last mile argument. But it was noted that looking at the annual inflation data for the last few years, it appeared that disinflation to date had actually been faster than the previous surge in inflation, questioning the empirical relevance of the “last mile” narrative.

PEPP Considerations

Finally, as for the somewhat surprise move to end PEPP reinvestments early, the account noted that the December results of the Survey of Monetary Analysts suggested that markets were already expecting a partial run-down of PEPP reinvestments from the middle of 2024 and a full run-off after December 2024. Moreover, it was also argued that the sustained demand for bonds in primary and secondary markets amid the ongoing run-down of the asset purchase programme (APP) portfolio was likely to support the smooth market absorption of an earlier end to full PEPP reinvestments.