ECB Meeting Preview: Summertime and the Living is Easing

Once again the looming ECB meeting (January 25) is one where markets are not preoccupied with what the Council will do but rather what is said. Stable policy is just about nailed on, but the question is whether there will be any more formal attempt to redirect market thinking that still prices in around 150 bp of rate cuts in the coming year. Given divisions within the Council, which have surfaced in terms of the hawks showing reticence about easing so much, there is likely to be something of communication fudge about the policy outlook. Regardless, ECB rhetoric has changed markedly of late, chiming somewhat with how and why market rate thinking has progressed. Indeed, President Lagarde is now suggesting rate cuts may occur in the summer, chiming with an interview from Chief Economist Lane who implied the June meeting will be critical. We still think that cuts may arrive sooner, although we still pencil in no more than 100 bp cuts this year to be followed by a similar sized fall in 2025.

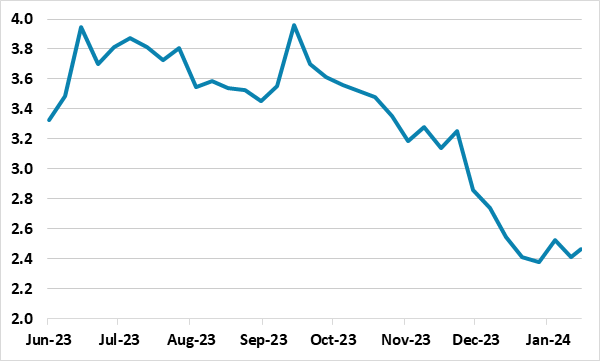

Figure 1: Aggressive Market Rate Thinking?

Source: Bloomberg, one year ahead ECB policy rate

Stable Policy in Perspective

After all, if the ECB were to wait until summer before easing, this would be a gap of around nine months since the last hike. That would be an appreciable wait, not least as the longest the ECB has even kept policy on hold before easing was back in 2000-01 when it waited less than eight months. Notably, that followed a hiking cycle of 225 bp, half that seen of late and where the recent set of hikes have been very much buttressed by ECB balance sheet reductions that have accentuated a tightening in credit conditions that have seen unprecedented falls in credit and money supply levels.

ECB Rhetoric On the Move

Moreover, ECB policy thinking has undergone a clear shift since the last hike in September 2023. Back In October, it was suggested that ‘even having a discussion on a cut is totally premature’ while last month it was said that ‘we did not discuss rate cuts at all. No discussion, no debate on this issue’. And now Lagarde says that the ECB is likely to cut interest rates in the summer, this echoing hints provided over the week-end by Chief Economist Lane. All of which suggests that despite no formal Council meeting having occurred in the last month, there has been clear discussion about the policy outlook as Council members have reacted to the same downside surprises (particularly on core inflation) that have prompted markets into their current policy outlook thinking (Figure 1). It also means that the minutes/account of the Dec 14 Council meeting due on Jan 18 may be largely redundant given how policy thinking has since evolved.

Why Point to the Summer

A stubborn Council, that alleges it is data dependent, very much wants to see an array of data due in coming months. While there is a clear focus on wages, Chief Economist Lane in a week-end interview underlined that the most complete dataset he wishes to assess is in the Eurostat national accounts data. As the Q1 data will not be available until the end of April, he pointed to the scheduled June Council meeting as being possible crucial as he will have those important data by then. In this regard, he is implying that the ECB wishes to see the income breakdown which will give a better insight not only into wages but also company profits which have been a clear additional factor in the recent inflation surge.

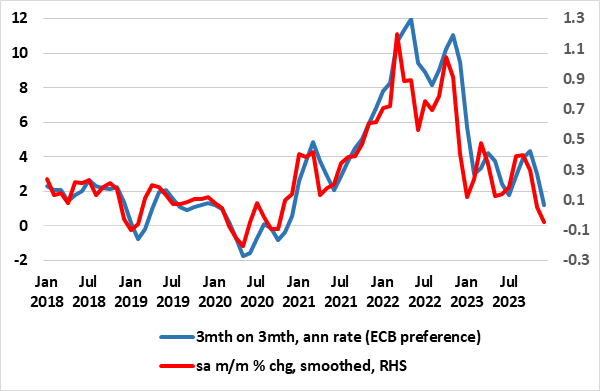

Figure 2: Adjusted m/m HICP Numbers Already Below Target

Source: ECB

Inflation Back Under Target Soon?

But very much other data will be even more important, not least the inflation numbers which we think could see the headline rate down to below the 2% target in Q2, thereby corroborating a disinflation trend already evident in seasonally adjusted m/m core and headline numbers, data we have been flagging for some time. And it does seem as if the ECB is starting to use such numbers as seen in a recent assessment by Lane, albeit using a 3 month on 3 month annualized measure that very much follows the more coincident 3 month moving average we prefer (Figure 2).

But other data will of course pay a role, especially real economy numbers where a recession may be formally identified for H2 last year and which may extend into 2024. But perhaps the other data over and beyond the downside inflation surprises that may have affected ECB thinking are the monetary numbers where there has been a unprecedented fall in broad and narrow money levels that have been accompanied by sharp falls in credit. The weakness in the later is something we fell is both demand and supply affected having been accentuated by tighter credit standards by the banking sector.

Key Bank Lending Survey Awaits

Thus makes next Tuesday’s ECB compiled Bank Lending Survey all the more important, especially if it merely echoes the worrying s signs of the last such survey released last October. That pointed to an on-going and substantial cumulative tightening in credit standards with a record drop reported in regard to company lending. The BLS also noted that bank’s access to funding deteriorated on a broad front. Overall, we think that the forthcoming BLS will again underscore the two pronged manner in which ECB tightening is affecting lending, both by the higher costs reducing demand but where (in sharp contrast to previous hiking cycles) the supply of credit is simultaneously being reduced by increased bank caution.