Fed: Leave Door Open To Cut, But

· Bottom line: The FOMC dots still pointed towards further rate cuts and Powell left the door open – noting it was too early to make judgement on the economic effects of the Iran war. We feel that the Fed is too optimistic about consumption and thus GDP, given that employment growth is close to zero and aggregate wage growth for the economy will be modest. On the Iran war our baseline remains for a 4-6 week war followed by a decline in WTI towards USD65-70 by end 2026. This can allow the Fed to look through the temporary impact of oil prices in March-April and deliver 25bps cut in September. Fed Warsh will also argue that current productivity is high and can argue for lower medium-term inflation and allow rate cuts and on the margin can be enough to help deliver the 2nd cut in December rather than Q1 2027. We would then see a pause throughout 2027.

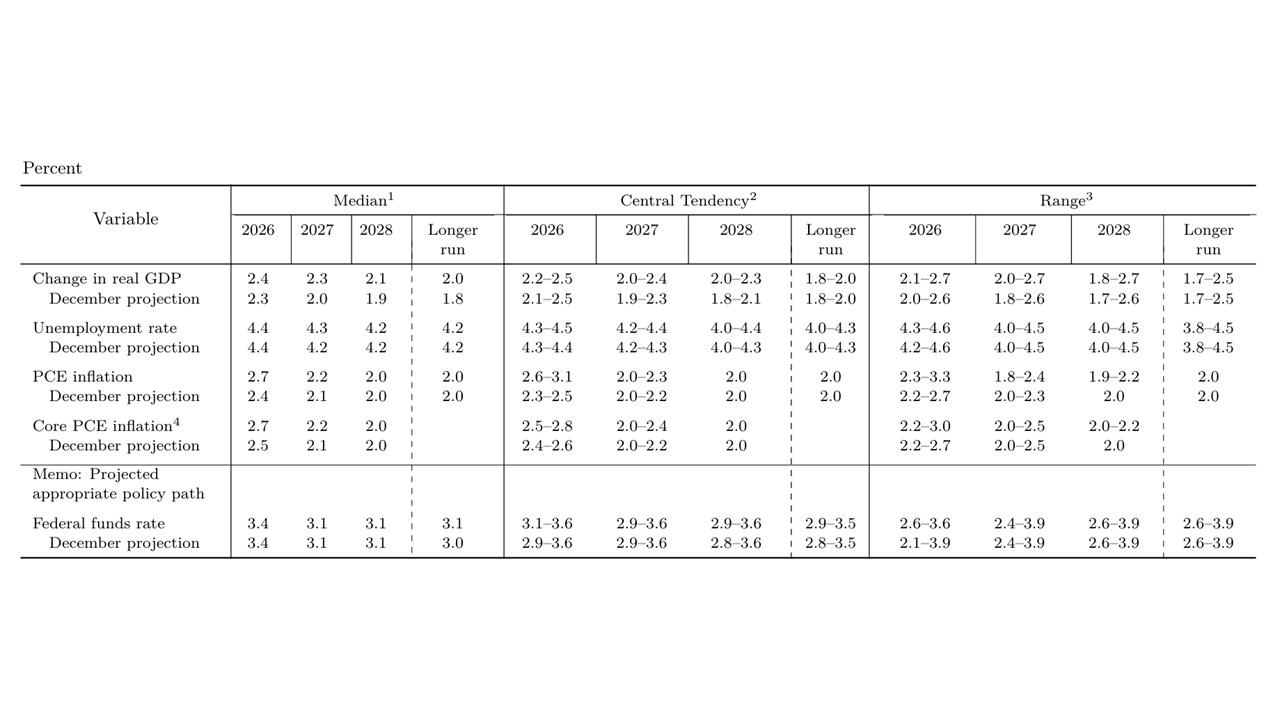

Figure 1: Fed March Summary of Economic Projections (SEP)

Source: Fed (March SEP)

Hold Then Cautious 2026 Easing

The March FOMC statement and Fed Chair Powell Q/A provide a number of clues on prospective policy. Key points include

· Inflation and growth. The FOMC median revised up the 2026 and 2027 GDP forecasts by 0.1% and 0.3% respectively, which is likely to be partially due to the ongoing AI infrastructure boom. Meanwhile, the median FOMC core PCE inflation was revised up 0.2% to 2.7%, but only by 0.1% in 2027 to 2.2% and this is consistent with no major 2nd round effects from higher energy prices yet. Powell did indicate however that it was too early to judge the economic effects of the Iran war, due to uncertainty over the duration and the impact on energy prices. The Fed chair also made clear that FOMC members’ conviction is not high and subject to change, though did note that the textbook is to think about looking through 1st round effects from energy shocks.

· Rates guidance. The March dot medians did not change from December, which was for one 25bps cut in 2026 and one 25bps in 2027 (Figure 1). Looking at the range of FOMC members Fed Funds views, 7 members want no change but we would note that this likely includes some non-voting FOMC fed district presidents. Fed Powell guidance in the Q/A was that the Fed bias remains towards rate cuts, though some had trimmed ideas of two cuts in 2026 to one further 25bps cut. Additionally, he guided that the rate cut in 2026 was conditional on inflation coming down, given the 1st round effects from tariffs on goods prices washing out. Meanwhile, it is also worth noting that the median for the long term neutral policy rate has edged upwards, which likely reflects some FOMC members feeling that the AI boom could push up the near-term neutral rate – Fed Barr, Cook and Jefferson have made this argument (here) and Powell also noted this in the Q/A, but too the Cook view that long-term AI could be disinflationary. Even so, neutral rate is largely an academic concept, as the Fed will act on policy rates with the macro picture from meeting to meeting.

· 2026 and 2027 rate prospects. We feel that the Fed is too optimistic about consumption, given that employment growth is close to zero and aggregate wage growth for the economy will be modest. Though high income households are robust, median to low income households are struggling and this suggests softer consumption than the Fed expects and also GDP growth. On the Iran war our baseline remains for a 4-6 week war followed by a decline in WTI towards USD65-70 by end 2026. It could be argued that this could build the case for a July 25bps cut, but the FOMC voters will likely want to wait until September and oil prices receding to the USD70-75 area. This can allow the Fed to look through the temporary impact of oil prices in March-April. We feel that the economic disappointment will be modest rather than large, but still enough to build a consensus for a further 25bps cut at the December meeting. Incoming Fed Chair Warsh will also argue that current productivity is high and can argue for lower medium-term inflation and allow rate cuts. This on the margin can be enough to help deliver the 2nd cut in December rather than Q1 2027. We would then see a pause throughout 2027.