ECB March Meeting Account – More Focus on Downside Risks than those on the Upside?

The Account of the Governing Council meeting on 5-6 March 2025 seemingly dwelt more on the downside risks posted by trade uncertainties than the upside risks posed by fiscal expansion plans across much of the EU. It noted that not all members supported the proposal to lower the three key ECB interest rates by 25 basis points but we were told that in the press conference. There were clear differences about how large and how to describe current policy restrictiveness but where a natural or neutral rate was seen of little value for steering policy on a meeting-by-meeting basis. Furthermore, it noted that the new projections presented at the meeting indicated that additional easing would be required to stabilise inflation at the medium-term target on a sustainable basis, albeit where (as we commented at the time) a lower probability should be attached to that central scenario given the risks noted above. But inflation might surprise on the downside if monetary policy dampened demand by more than expected. Regardless, it was considered important that the amended language on policy restriction should not be interpreted as sending a signal in either direction for the April meeting, with both a cut and a pause on the table. But the financial sector remains a worry!

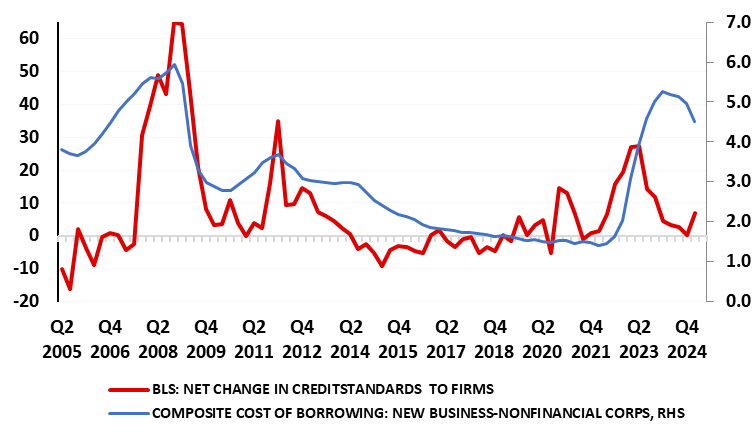

Figure 1: Modest but Troubling Rise in Credit Standards Already Evident

Source: ECB

This reinforced the value of a meeting-by-meeting approach, with no pre-commitment to any particular rate path. In the near term, it would allow the Governing Council to take into account all the incoming data between the current meeting and the meeting on 16-17 April, together with the latest waves of the ECB’s surveys, including the bank lending survey, the Corporate Telephone Survey, the Survey of Professional Forecasters and the Consumer Expectations Survey. Indeed, we note how important the bank lending survey (BLS) may be with a clear factor in ECB thinking how banks may react to the added uncertainty from tariffs certainly after what a troubling rise in credit standards for firms in the last set of numbers in January (Figure 1). The ECB is now admitting its QT program maybe making banks less willing/able to lend and now with increased real activity uncertainty, so the ECB will be looking at its Bank Lending Survey due two days before the April 17 Council meeting to see if credit standards are tightened further – of so another cut at the meeting would be so much more likely. Indeed, the topic of financial conditions on the economy was discussed in the March meeting. In particular, it was argued that the level of interest rates and possible financing constraints – stemming from the availability of both internal and external funds – might be weighing on corporate investment – again highlighting the likely importance of the BLS.

Looking ahead, the point was made in the March meeting that the likely shocks on the horizon, including from escalating trade tensions, and uncertainty more generally, risked significantly weighing on growth. It was argued that these factors could increase the risk of undershooting the inflation target in the medium term. In addition, it was argued that the recent appreciation of the euro and the decline in energy prices since the cut-off date for the staff projections, together with the cooling labour market and well-anchored inflation expectations, mitigated concerns about the upward revision to the near-term inflation profile and upside risks to inflation more generally. From this perspective, it was argued that being prudent in the face of uncertainty did not necessarily equate to being gradual in adjusting the interest rate.

Perhaps more pertinent over and beyond the March meeting account is the speech today from, Vice-President de Guindos, about Financial stability in uncertain times. He noted that while banks remain in good shape, with sound solvency and liquidity indicators that are well above regulatory minimums, there are weaknesses in several other areas. First, elevated valuations and concentrated risks make financial markets susceptible to adverse corrections. Second, sovereign indebtedness is a cause for concern at a time when defence spending is emerging as a priority in Europe, with different countries having very different amounts of fiscal space to respond. Third, the corporate sector has demonstrated resilience but faces competitiveness challenges and is subject to emerging credit risk concerns, especially in the case of firms that are more exposed to the export sector and geopolitical risks. In conclusion, he noted that an extraordinarily high level of uncertainty around economic and trade policy has been acting as a drag on markets and the economy alike. Overall it does seem as if the ECB is more focused on downside risks that any upside ones stemming from fiscal expansion.