Time Has Come: SARB Cut the Key Rate to 8.0% on September 19

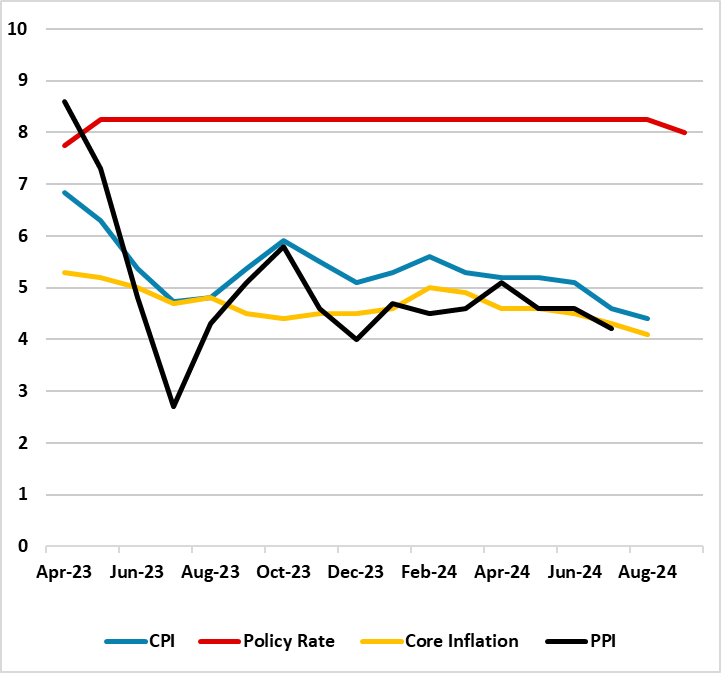

Bottom line: As we expected, South African Reserve Bank (SARB) started cutting the key rate at the upcoming MPC meeting on September 19 and decreased it from 8.25% to 8.0% given recent fall in inflation, suspended power cuts (loadshedding) after March, deceleration in inflation expectations and a relatively stable Rand (ZAR) as well as global central bank moves - mainly the U.S. Federal Reserve (Fed), which cut rates by 50 bps on September 18. The decision to cut rates was unanimous. Our end-year policy rate prediction remains at 8.0% for 2024, and 7.0% for 2025.

Figure 1: Policy Rate (%), CPI, PPI and Core Inflation (YoY, % Change), April 2023 – September 2024

Source: Continuum Economics

SARB announced its interest-rate decision on September 19, and as we expected the regulator cut the policy rate by 25 bps from 8.25% to 8.0%, for the first time since its Covid-19 response over four years ago. This marks the first time since May 2023 that the MPC has changed rates, and the MPC decision was unanimous.

There were many reasons behind the critical decision. First, on the inflation front, CPI continues its downward trend and further decreased to 4.4% in August driven by lower annual rates in several categories notably restaurants, fuel, transport, and housing. August inflation was below the midpoint of target band of 3% - 6%, and it marked the lowest inflation print since April 2021.

Second, Fed announced on September 18 that it reduced the key lending rate by half a percentage point, to a range of 4.75% to 5%, which is expected to loosen global financial conditions and potentially easing pressure on the ZAR, and hence on import prices.

On the power cuts end, after Stages 2 and 3 load shedding was implemented broadly in March, South Africa’s national electricity utility company, Eskom, announced on September 13 that load shedding remained suspended for 170 consecutive days, reflecting structural generation improvements and new investments. This is a significant development for South African economy as the suspension helped businesses and households to relieve facing increasing costs from using alternative sources such as diesel backup generators, contributing at lower inflation figures. (Note: Inflation outlook was also supported by a relatively stable ZAR, which hovered around 17.8-18.3 against the USD in August).

In addition to inflation readings, positive news is coming from the inflation expectations, as well. According to BER survey released on September 12, the average inflation forecast for 2024 fell to 5.1% in Q3 from 5.3% in Q2. This was a key data point for SARB as SARB governor Kganyago repeatedly said the regulator is paying full attention to the inflation expectations.

Following SARB’s decision, Kganyago emphasized on September 19 that the MPC members considered an unchanged stance, a 25 bps cut, and a 50 bps cut. Kganyago said that “The MPC ultimately reached consensus on 25 bps, agreeing that a less restrictive stance was consistent with sustainably lower inflation over the medium term.” The governor added that the forecast sees rates moving towards neutral next year, stabilising slightly above 7%, implying another 75-100 bps cuts to come. “Decisions of the MPC will continue to be data dependent, and sensitive to the balance of risks to the outlook,” Kganyago emphasized.

As SARB intermittingly signalled that it plans to start cutting interest rates after the inflationary pressures are under control backed up by data and expectations, we correctly envisaged an end to SARB tightening on September 19 as inflation continued its downward trend due to suspended power cuts, deceleration in inflation expectations and a relatively stable ZAR. We believe the cut will be relief for the consumers facing high costs of loans, as well as the automotive industry and the property sectors which have been hard hit by the elevated interest rates.

It is worth noting that inflationary risks remain due to the supply-side constraints like crisis at ports and rail network, geopolitical risks, and the U.S. presidential election in November, which shall be closely followed by SARB in Q4 and Q1 2025, before further rate cuts. In line with this, SARB governor Kganyago stated on September 19 that, inflation could be higher than SARB’s baseline forecast given scenarios such as higher housing costs, larger electricity price increases, wage increases that outrun inflation and productivity growth or higher food inflation causing uncertainty, demonstrating that SARB will be cautious about risks to the inflation outlook.

We now believe that SARB will hold the key rate stable at 8.0% in the next MPC meeting scheduled on November 21. Our end-year policy rate prediction remains at 8.0% for 2024, and 7.0% for 2025.