German HICP Review: Headline Back Higher But EZ Price Picture Still Reassuring?

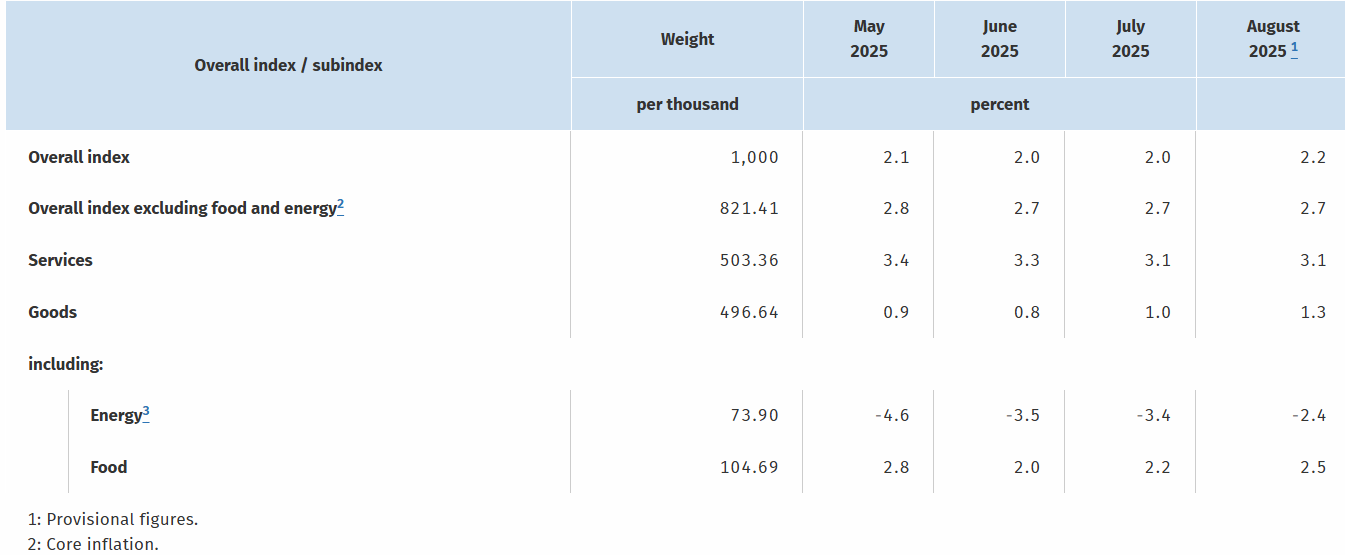

Germany’s disinflation process hit a slightly more-than-expected hurdle in August, as the HICP measure rose 0.3 ppt from July’s 1.8% y/y, that having been a 10-mth low (Figure 1). This occurred largely due to energy base effects with food prices also contributing slightly. The result was that the CPI core rate was unchanged at 2.7%. Despite the German rise, the likelihood is that next Tuesdays EZ HICP data will rise by only 0.1 ppt, and possibly actually stay at July’s 2.0% given the downside surprises seen in Italian, French and Spanish data seen earlier today. The (likely to be friendly) HICP details may be more important for the likes of the ECB.

Figure 1: German HICP Inflation Edges Back Above Target?

Source: German Federal Stats Office

The German August data were again bolstered by energy prices – mainly due to fuel prices having dipped more this time last year than this year – and this will again be the case in September despite some small m/m drop seems to have occurred. Indeed, such base effects could pull the headline a little higher in September, before a fresh fall resumes in Q4! Regardless, perhaps continued disinflation news is evident in adjusted m/m data which have shown some fresh downtick in core rates even though this does not seem to have proceeded discernibly further in the August numbers. In fact, adjusted data also suggest disinflation may have stalled, although this may be more a result of recent calendar aberrations than anything underlying and even if so, the data remain consistent with on-target inflation.

As for the EZ inflation picture, and despite the German rise, the likelihood is that next Tuesday’s EZ HICP data will rise by only 0.1 ppt, and possibly actually stay at July’s 2.0% given the downside surprises seen in Italian, French and Spanish data seen earlier today. Moreover, those numbers, together with the German figures suggest some further slowing in hitherto seemingly resilient EZ services inflation. This may be of the order of 0.1-0.2 ppt, this likely to take the EZ core HICP down again – we see it the August reading dropping from 2.3% to a fresh cycle-low of 2.1%, below consensus and also suggesting an undershoot of ECB underlying inflation forecast for Q3, a softening already evident in adjusted m/m data. As a result, the EZ headline and core rate could both dip below 2% in Q4 with base effects pulling the headline down to around 1.5% in Q1, especially if demand weakness starts to accentuate what have largely been supply factors driving the disinflation process hitherto.