Rupee at Record Low: Can India Weather the Dollar Storm?

The Indian rupee has slumped to an all-time low of 86 against the US dollar, underscoring the pressure on emerging market currencies as the dollar index surges to multi-month highs. For India, this currency depreciation signals potential disruptions in financial markets, with equities and bonds—now embedded in global indices—facing headwinds.

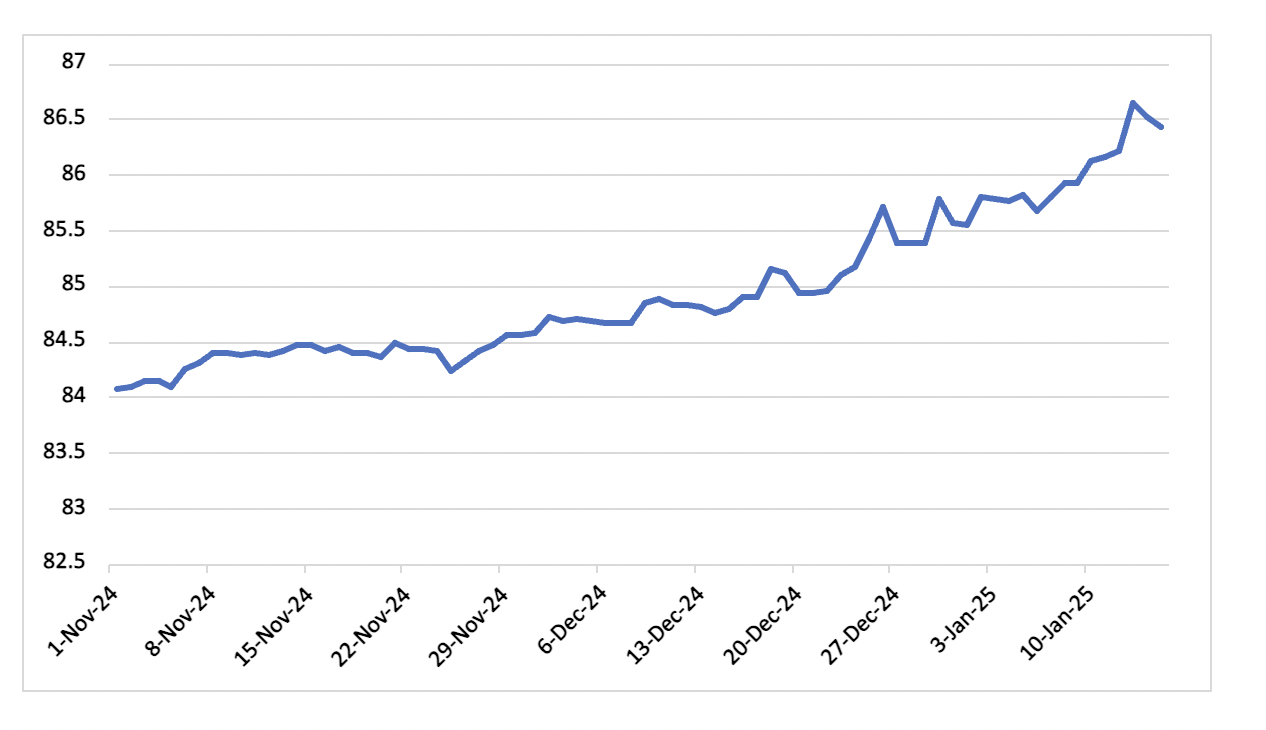

Figure 1: USD/INR Exchange Rate

The Indian INR's recent slide to a record low of 86.6 against the US dollar underscores the pressures facing emerging market currencies amid a global macroeconomic realignment. A resurgent US dollar, bolstered by unexpectedly strong economic performance and a hawkish Federal Reserve, has amplified challenges for India’s currency. The dollar index has surged by 8% over the last three months, compounding the INR’s depreciation and creating ripple effects across India’s financial markets.

A struggling Eurozone and slowing growth in China, which has also adopted a more flexible currency regime, leave the dollar as the preferred safe haven. Geopolitical uncertainties and elevated policy risks only enhance the appeal of dollar-denominated assets, putting added strain on emerging market currencies like the INR.

India’s central bank has long managed the INR’s exchange rate with an approach bordering on a de facto peg, supported by aggressive forex reserve interventions. However, this strategy is becoming increasingly untenable. Since October 2024, the Reserve Bank of India’s (RBI) foreign currency assets have dropped by US$47bn, straining domestic liquidity despite recent measures like a 50-basis-point cash reserve ratio cut. Maintaining such rigidity against the backdrop of a strengthening dollar may exacerbate misalignments in the rupee’s valuation. With forex reserves declining and the risk of speculative attacks rising, the RBI may have no choice but to allow greater currency flexibility, in our view. The INR’s woes are compounded by weakening economic indicators. Indian equities have underperformed global peers, with the Nifty and Sensex delivering an 8.3% yr/yr return compared to the US S&P 500's 26%. Corporate profits, once buoyed by post-pandemic demand, have contracted under margin pressures and subdued consumption. This relative underperformance could deter foreign portfolio investors, further pressuring the rupee. Overseas investors have withdrawn over US$4bn from local stocks in January so far. This follows an additional US$ 11bn outflows in Q4 2024, a complete turnaround from the US$30bn inflows seen in Jan-Sep 2024.

Outlook: Further Depreciation Likely

Projections suggest that the rupee may weaken further, potentially reaching 87-88 against the dollar in the coming months. This aligns with the currency's historical trend of depreciating by 4% annually against the dollar. A significant negative India-US real policy rate spread (-1.7% in November 2024) and an overvalued real effective exchange rate add to depreciation pressures. While a weaker rupee could bolster export sectors such as IT and pharmaceuticals, it raises concerns about imported inflation, particularly in essential commodities like crude oil. RBI studies indicate that a 5% depreciation of the INR increases headline inflation by 35bps. New Governor Sanjay Malhotra has yet to articulate a clear stance, but signs of a more flexible exchange rate regime are emerging. Increased volatility in the INR’s trading patterns and calls for reduced intervention suggests a shift in strategy may be inevitable.

Allowing greater currency flexibility could alleviate some of the pressure on India’s reserves and align the INR more closely with market fundamentals. However, this approach would require robust measures to mitigate potential short-term shocks to the economy. The INR slide will also weigh on the RBI’s upcoming decision in February. The RBI will attempt to balance easing growth momentum with inflation and exchange rate stability. A more severe depreciation in the coming weeks or hints of price pressures mounting could see the RBI defer the rate cut to April. However, the probability remains low, especially as growth concerns increase.