Preview: Due April 5 - U.S. March Employment (Non-Farm Payrolls) - Slightly Slower but Labor Market Remains Strong

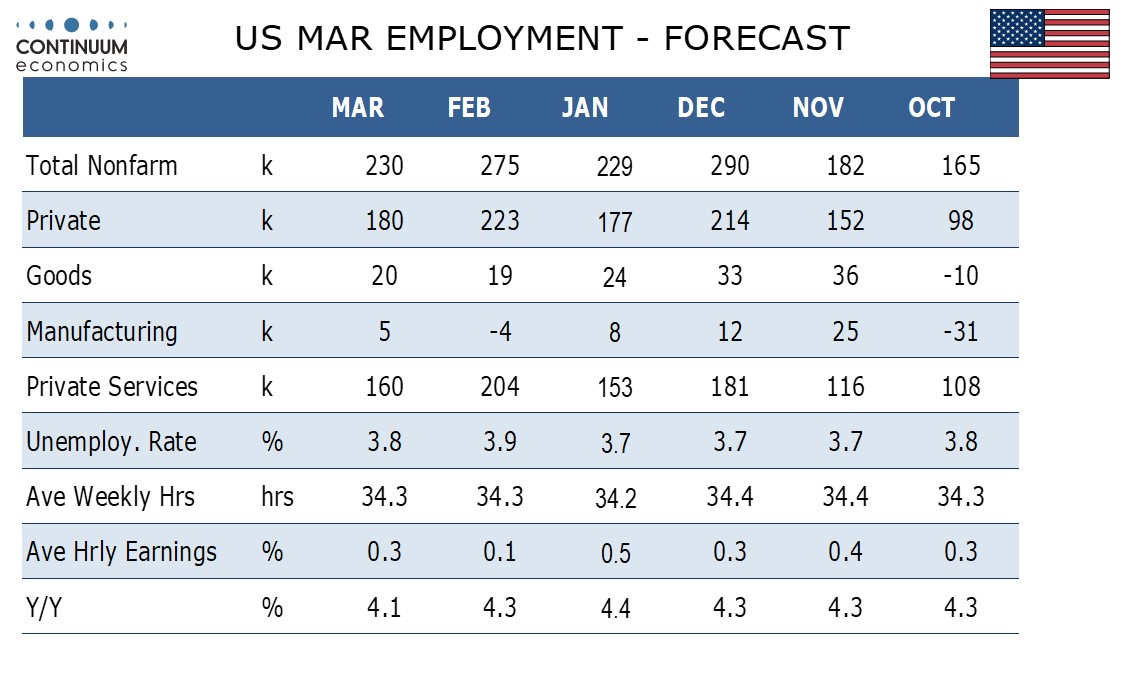

We expect a 230k increase in March’s non-farm payroll, which would be in line with the 6-month average but slightly below the 3-month. We expect a correction lower in unemployment to 3.8% from 3.9% and a moderate 0.3% increase in average hourly earnings.

Signals on the labor market remain strong, with initial claims remaining low and labor market perceptions actually picking up in the March consumer confidence report. However a few surveys suggest the economy may be losing a little momentum, so we expect a slightly slower payroll gain than February’s 275k, but there is little reason to expect a break of trend. We expect private payrolls to rise by 180k versus a 223k rise in February, with government remaining strong.

The unemployment rate rose to 3.9% in February after three straight months at 3.7% as the household survey showed employment slipping while the labor force increased. We expect employment to outpace labor force growth in March, moving the rate back down to 3.8%.

The unemployment rate rose to 3.9% in February after three straight months at 3.7% as the household survey showed employment slipping while the labor force increased. We expect employment to outpace labor force growth in March, moving the rate back down to 3.8%.

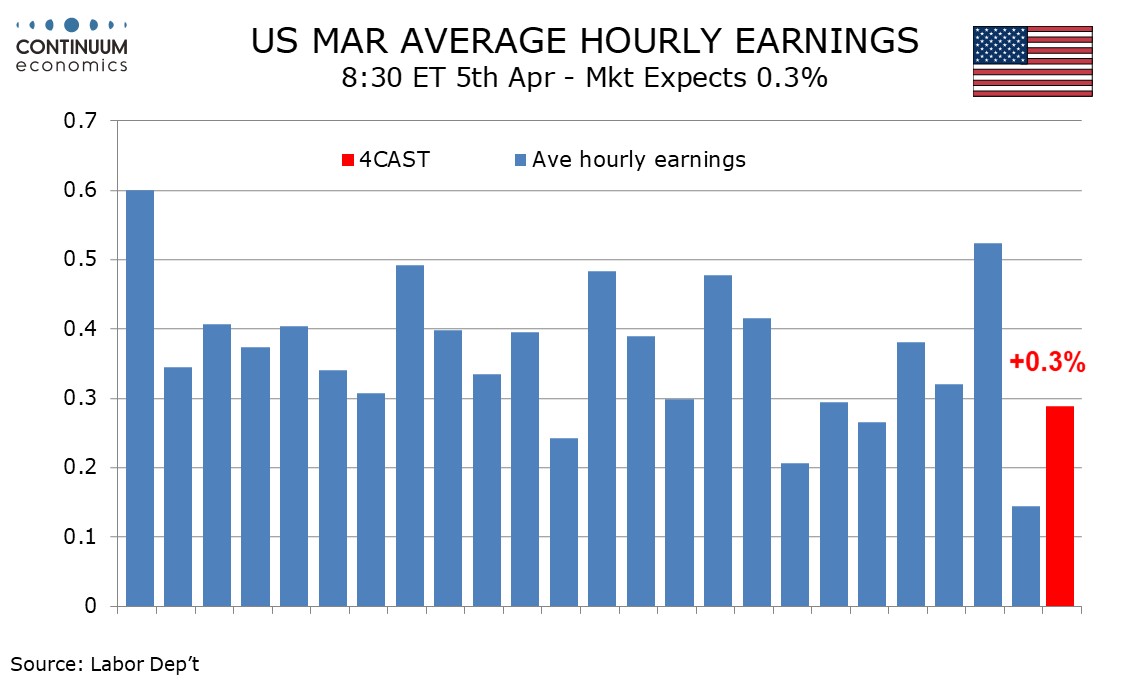

Average hourly earnings rose by an above trend 0.5% in January and a below trend 0.1% in February, and we expect a 0.3% rise in March. This would see yr/yr growth slowing to 4.1% from 4.3%, to its lowest since June 2021. Trend is a little stronger than 0.3% per month with both January and February data rounded down.

Average hourly earnings rose by an above trend 0.5% in January and a below trend 0.1% in February, and we expect a 0.3% rise in March. This would see yr/yr growth slowing to 4.1% from 4.3%, to its lowest since June 2021. Trend is a little stronger than 0.3% per month with both January and February data rounded down.

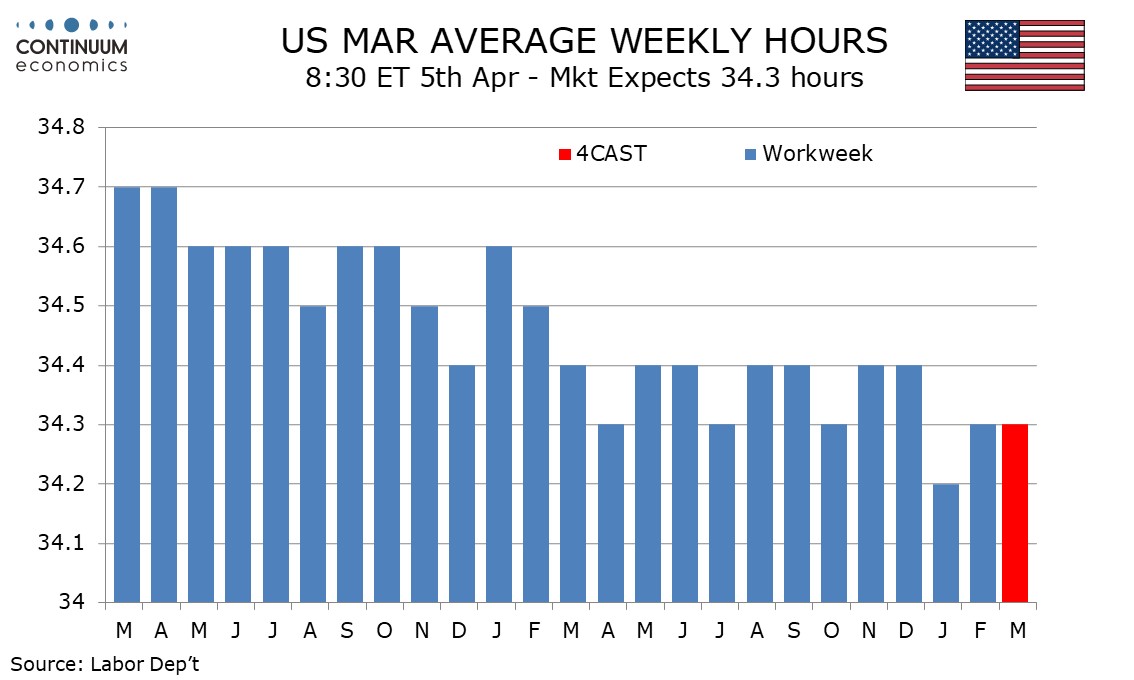

That the workweek slipped, probably on bad weather, in January and recovered in February may have inflated earnings per hour in January and restrained February’s data. We expect the workweek to be unchanged in March but with a rise more likely than a fall, which suggests hourly earnings are more likely to be below than above trend.

That the workweek slipped, probably on bad weather, in January and recovered in February may have inflated earnings per hour in January and restrained February’s data. We expect the workweek to be unchanged in March but with a rise more likely than a fall, which suggests hourly earnings are more likely to be below than above trend.

Our forecasts for employment and the workweek would leave aggregate hours worked up by a modest 0.6% annualized in Q1, versus 1.4% in Q4 and 1.5% in Q3, hinting at slower GDP growth after two strong quarters but if productivity remains firm growth should remain respectable.

Our forecasts for employment and the workweek would leave aggregate hours worked up by a modest 0.6% annualized in Q1, versus 1.4% in Q4 and 1.5% in Q3, hinting at slower GDP growth after two strong quarters but if productivity remains firm growth should remain respectable.