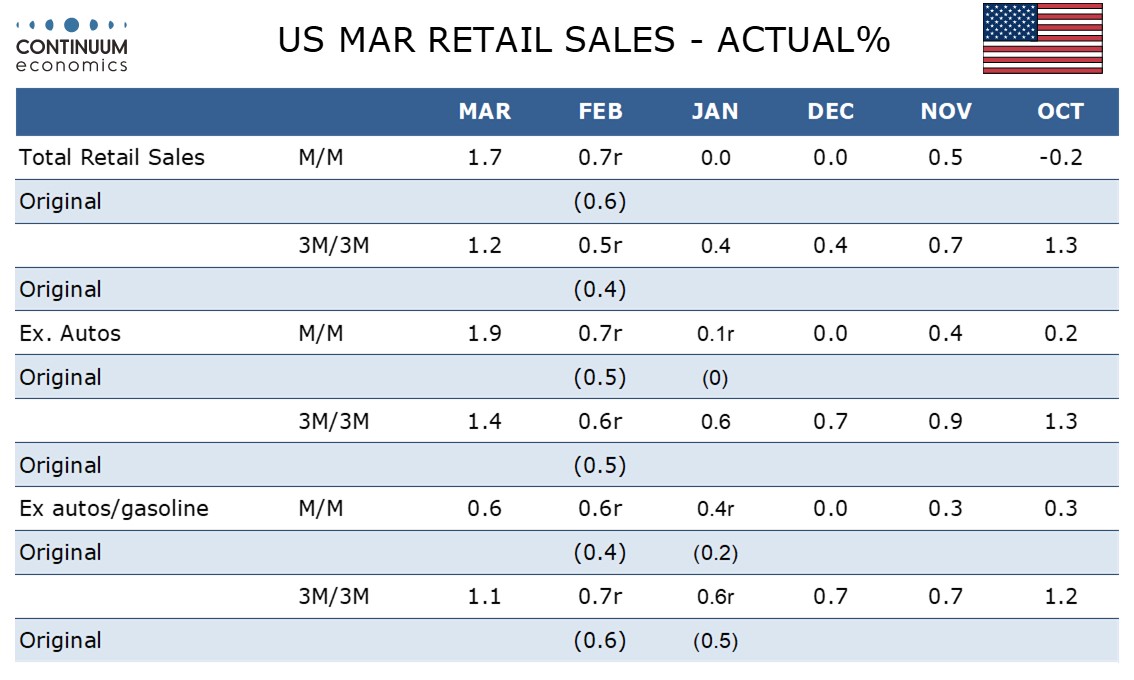

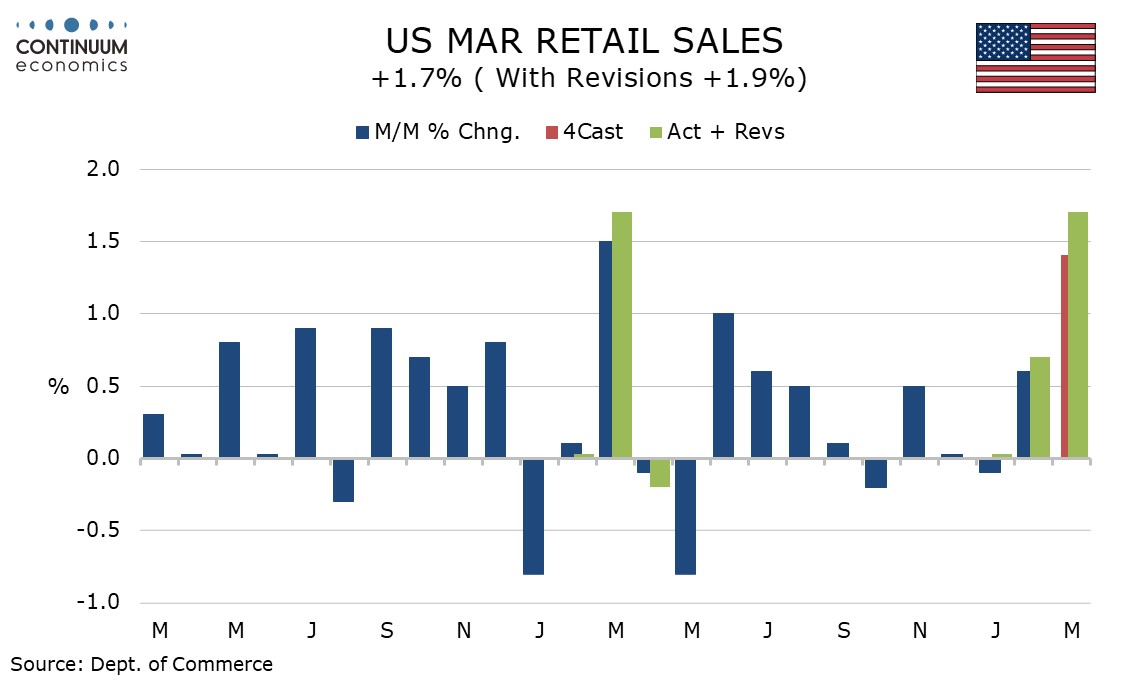

U.S. March Retail Sales - Underlying resilience, lower taxes may be helping

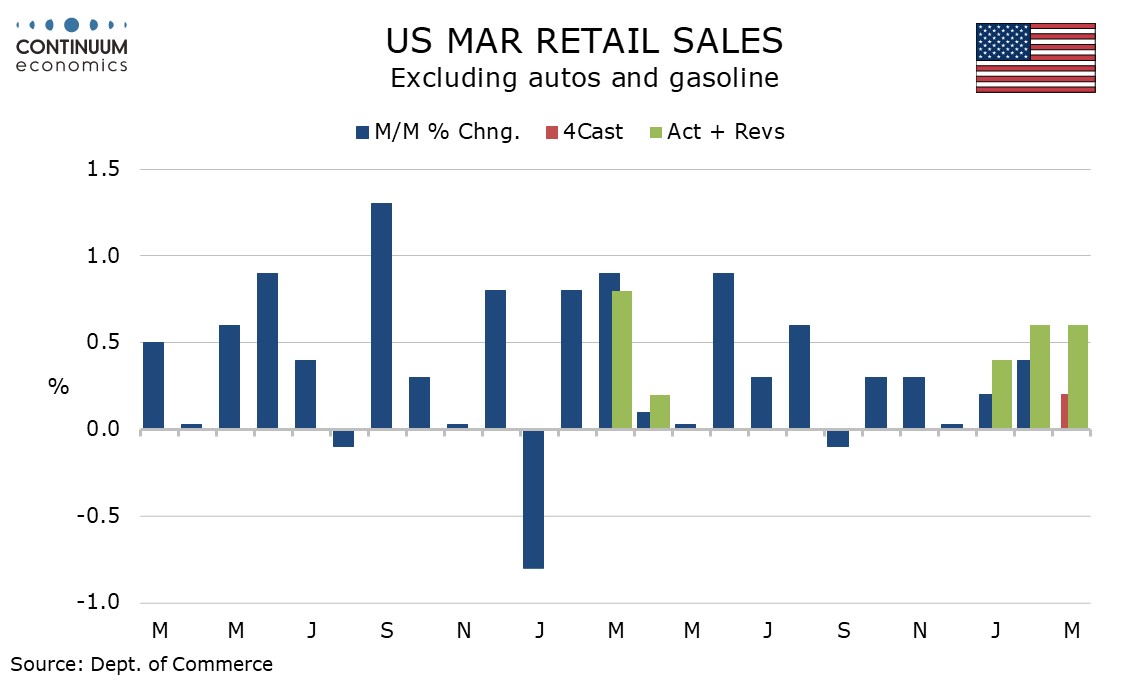

March retail sales with a 1.7% rise, 1.9% ex autos are stronger than expected. Most of the rise is on the surging price of gasoline, though sales ex auto and gasoline with a 0.6% increase are on the firm side of expectations, with February revised up to 0.6% from 0.4% and January to 0.4% from 0.2%. Tax cuts passed in 2025 have lifted tax refunds in early 2026 and are in part offsetting the rise in gasoline prices.

Revisions overall were less strong than for ex auto and gasoline sales, with February revised up only marginally to a 0.7% rise from 0.6% and January now unchanged rather than declining by 0.1%.

March gasoline sales surged by 15.5% but this was less than a 21.3% rise in gasoline prices seen in the CPI. The overall retail sales rise of 1.9% was very similar to a 2.0% rise seen in commodity prices seen in the CPI. Commodities less food, energy, used cars and trucks rose by only 0.2% in the CPI, suggesting the ex-autos and gasoline sales gain of 0.6% came more from volumes than prices.

Food sales were quite firm with a 0.7% rise, despite CPI food prices being unchanged. Other positives in the breakdown include gains of 2.2% in furniture and home furnishing and 1.0% in general merchandise. Only miscellaneous stores with a 0.9% decline were significantly negative. Autos saw a modest 0.5% rise, less than the ex-auto gain, meaning headline sales underperformed those ex auto.

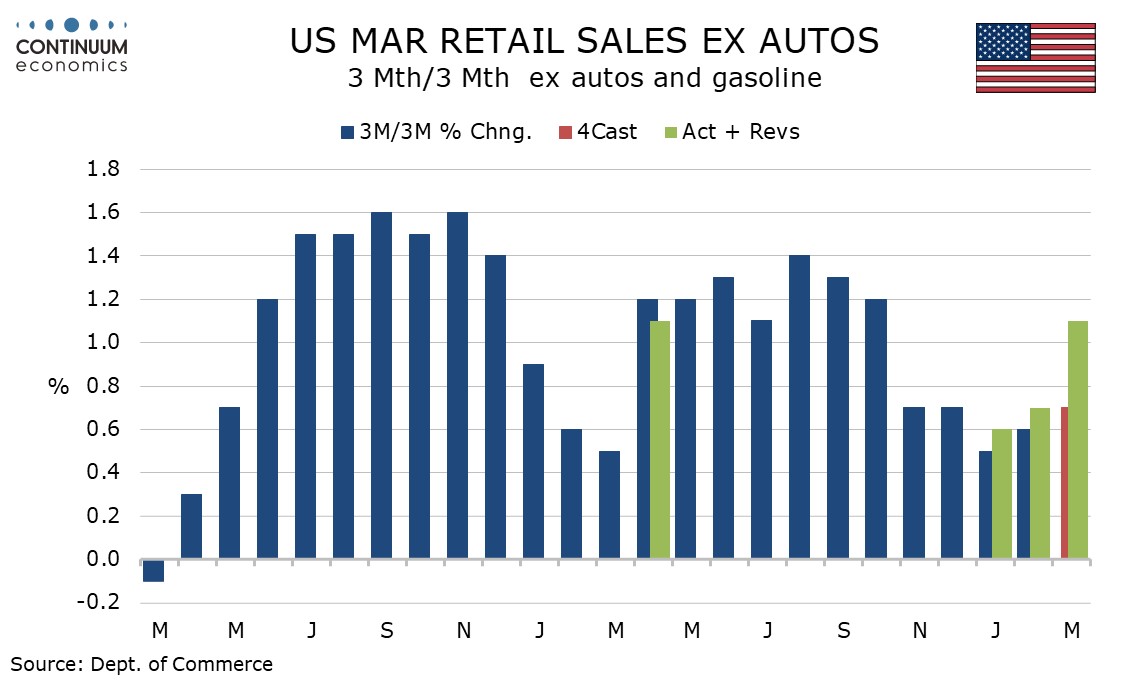

Q1 sales ex auto and gasoline rose by 1.1% (not annualized) after a 0.7% rise in Q4, thus regaining some momentum despite some bad weather in January and February, and thus showing resilience to weakness in real disposable income, something rising gasoline prices will further undermine. Quarterly gains of 1.2% in overall sales and 1.4% ex auto were stronger still, but lifted by gasoline.