FX Weekly Strategy: Asia, April 27th- May 1st

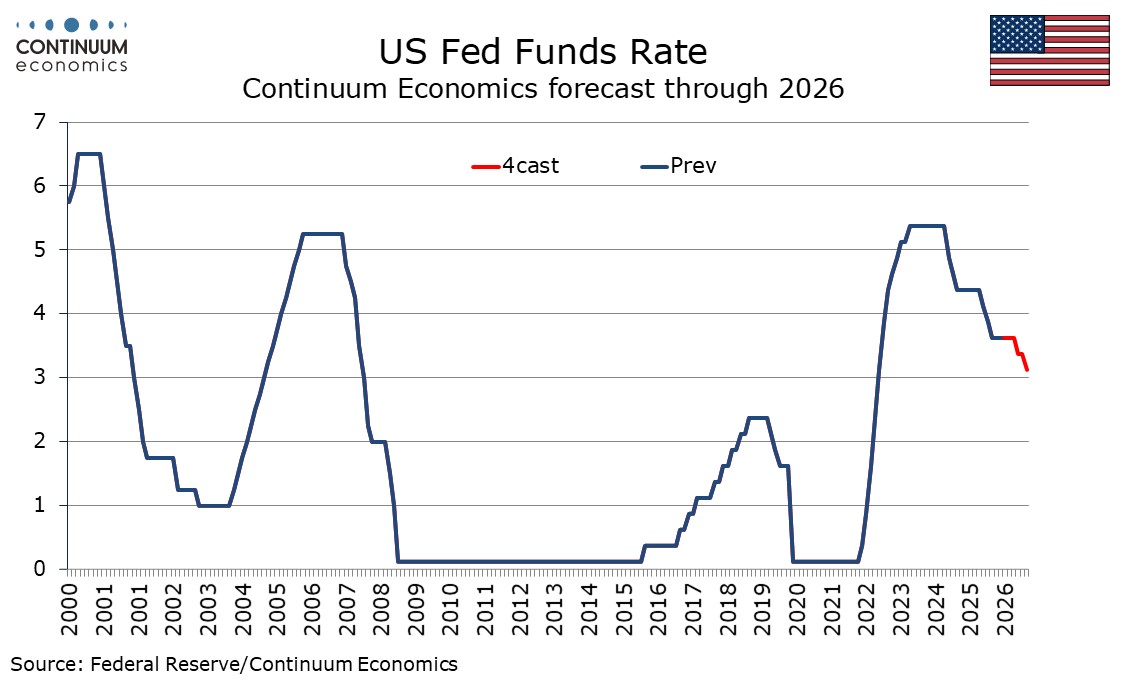

Uncertainty keeping the Fed on hold

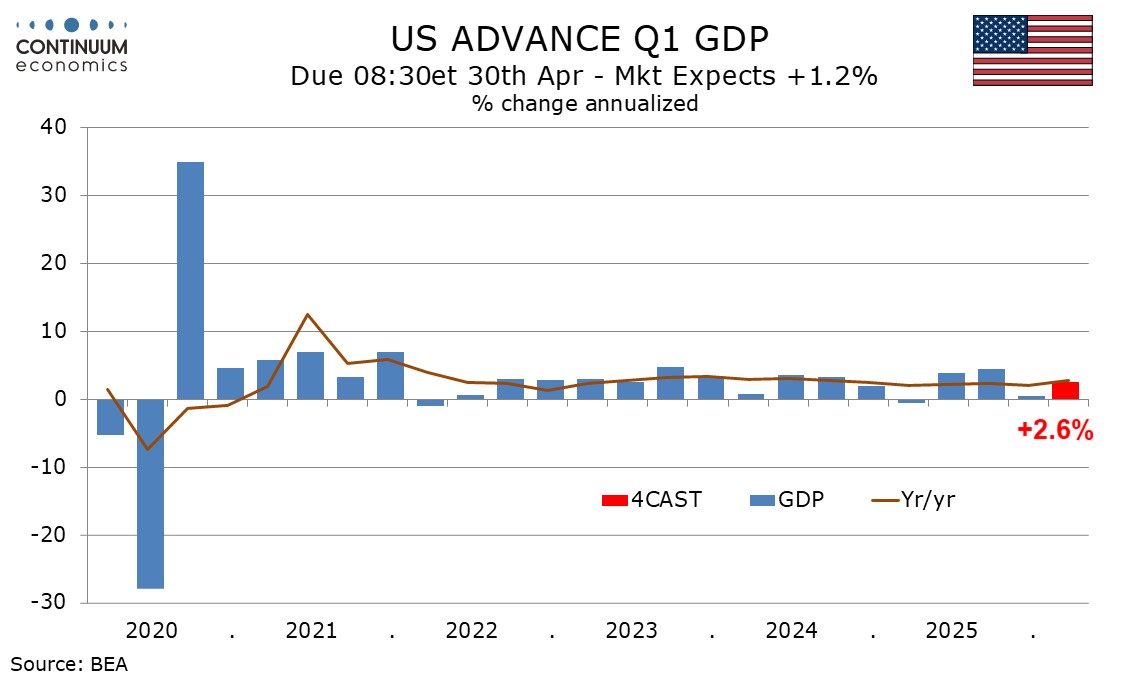

U.S. Q1 GDP to lead bounce from Government Spending

Real Economy Buckling Already Before ECB

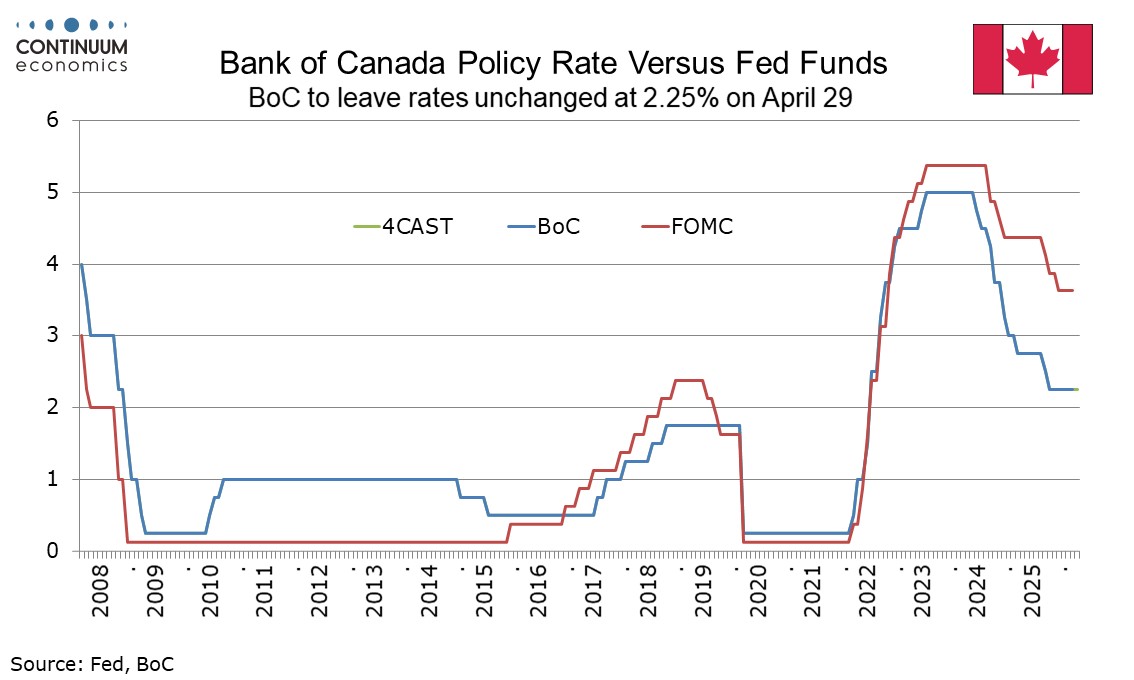

Bank of Canada No hawkish shift from energy price shock

The FOMC meets on April 29 and there is little risk of a change in rates from the current target range of 3.5-3.75%. High uncertainty, both on the geopolitical situation and the future of the Fed, suggests there will be little forward guidance, and the dots will not be updated until the next meeting on June 17. If there is a shift in tone it is more likely to be in a hawkish direction, but few appear to be considering a near term tightening, and we still expect the next move is more likely to be an ease.

There does not appear to be any pressing need for the FOMC to alter its statement from the last one on March 16, which saw the economy expanding at a solid pace. Q1 GDP data due on April 30 is likely to confirm this (we expect a 2.6% annualized increase). The statement went on to say that job gains have remained low and the unemployment rate has been little changed in recent months. That also remains the case, but a stronger March non-farm payroll suggests any fine tuning to the view will be positive. Inflation was described as somewhat elevated. With core PCE prices looking firm in Q1 (we expect a 4.1% annualized increase) and energy prices having surged, the Fed may say a little more on inflation this time.

We expect a 2.6% annualized increase in Q1 GDP, improved from a weak 0.5% in Q4 largely due to a rebound in government from Q4 data that was depressed by a shutdown. Excluding government we expect a second straight quarter close to 1.5%. We expect a significant acceleration in core PCE prices, to 4.1%, the highest since Q1 2023, from 2.7% in Q4.

We expect government to rise by 6.7%, more than fully reversing a shutdown-induced 5.6% decline in Q4. However we expect slower growth from state and local government and within the Federal detail so not expect a full reversal in non-defense Federal spending. Government did return to growth in Q3 after DOGE-related declines in Q1 and Q2, and we expect moderate growth going forward.

Figure: Real Economy Hit Clear(er) This Time Around

We again expect no change from the ECB on Apr 30, but President Lagarde will probably have to admit in the Q&A that unlike last time the decision was not unanimous. Overall, the communication will again suggest upside risks for inflation and downside risks for economic growth the extent and duration of both depend both on the intensity, length and likely resolution of the conflict. We still think the ECB is too pessimistic about inflation and too optimistic about growth as PMI data have started to show (Figure). And a series of data updates in the coming week may highlight this further, not least a bank lending survey showing probably increasing, signs of banks wariness about lending. In coming months, and given the manner in which the ECB may feel it cannot afford a repeat of what some call the policy mistake of four years ago, a rate hike by mid–year cannot be ruled out. But, this would be a mistake, ignoring how the policy and economic backdrop is vastly and increasingly different to then. As a result, we still see the next move being a cut to address adverse monetary condition albeit very late in the year!

The Bank of Canada meets on April 29 and looks set to leave rates unchanged at 2.25%. A quarterly Monetary Policy Report is due but given uncertainty the BoC may deliver a range of scenarios rather than an updated forecast. Despite the upside risks to overall inflation, recent subdued economic activity and core inflation data suggests the BoC will not delver a more hawkish tone.

In its last Monetary Policy Report in January the BoC looked for 1.8% annualized GDP growth in Q1. The statement at the last meeting on March 18 suggested near term growth would be weaker than expected in January, though we do not expect a sharp underperformance of the BoC’s forecast. Q4 GDP at -0.6% annualized was weaker than a flat BoC projection but the BoC in March noted this was largely on an inventory drawdown. The March statement also noted weak January and February employment data, which was followed by only a marginal correction higher in March. We expect the BoC will look for a subdued Q2 GDP gain of around 1.0% but its January forecast of 1.4% Q4/Q4 does not appear to require a significant downgrade. The growth implications of the energy shock are mixed for Canada, with the energy sector likely to see a boost.

For the Week Ahead

UK

The BoE dominates the week with Friday’s money/credit data likely to show more signs of a softer housing market but with the BoE/MPC decision and updated forecasts (Thu) taking top bill. Very clearly, the BoE kept rates on hold with the MPC unanimous last month and the same decision is expected this time around but with fresh dissent, with 2-3 members opting for an immediate hike. These splits will be even more evident in the individual MPC member statements (as expected) where more diverging views may again act to confuse markets seeking a clear(er) communication from the BoE.

Eurozone

There are various important data updates due before the next ECB verdict, such as Thursday’s jobless data and HICP and GDP numbers (for the EZ and individual members), the former likely to be up to as high as 3.0% but with a still stable core while the latter sags back to 0.1% q/q in Q1. NB; the EZ HICP data will be preceded by national CPI/HICP data with key German data due Apr 29 and where we see a relatively larger April jump from 3.8% to 3.3%!

But it is the next ECB Bank Lending Survey (Tue) that may be the most telling update, it’s likely message of (probably increased) bank wariness about lending partly being flagged by the ECB’s survey on the access to finance of enterprises (SAFE) due on Monday which also provides information on developments in the financial situation of enterprises and availability of external financing. Tuesday will see how things have shifted upwards in the ECB consumer expectations survey while Wednesday sees actual money and credit figures, still pre-war though. Wednesday also sees what will be gloomier European Commission survey data and more survey number arrive on Friday with final manufacturing PMIs

As for the ECB on Thursday, we again expect no change from the ECB, but President Lagarde will probably have to admit in the Q&A that, unlike last time, the decision was not unanimous. Overall, the communication will again suggest upside risks for inflation and downside risks for economic growth, the extent and duration of both depend both on the intensity, length and likely resolution of the conflict. These are just the added considerations that the ECB will have to assess but recent Council member comments suggest it is in no hurry to make sudden conclusions. Indeed, speaking from either side of the hawk-dove divide, Council member Schnabel suggested last week of no need to rush into a decision to raise rates while BoF Governor Villeroy de Galhau stressed that ‘a focus on April would be premature’.

Rest of Western Europe

There are few key events in Sweden, with the March GDP indicator likely to mean a pointer to a clear q/q Q1 drop. And more bad news may come in the Economic Tendency Survey also due on Wednesday. In Switzerland, Thursday sees the latest KOF survey update. Norway on Monday releases the latest credit numbers.

USA

A busy US weekly calendar opens quietly on Monday. Tuesday sees February house price data from FHFA and S and P Case-Shiller, and April consumer confidence. The latter is likely to take a hit on higher energy prices, but probably not as sharply as the Michigan CSI. On Wednesday housing starts and permits for both February and March will be released. We expect starts to fall by 7.2% in February after a 7.2% January increase, before a 1.4% rise to 1400k in March. We expect permits to rise by 0.3% in February to 1390k, and remain at that level in March. Also on Wednesday we expect March durable goods orders to increase by 1.0%, with a 0.4% rise ex transport, and March’s advance goods trade deficit to increase to $87.8bn from $83.5bn.

The FOMC meets on Wednesday and is likely to leave rates unchanged at 3.5-3.75%, giving limited forward guidance given exceptional uncertainty. The dots are not due to be updated at this meeting. The statement is likely to see limited changes from March, but with recent activity data showing resilience and the energy shock raising inflation risks any change in tone is likely to be in a hawkish direction, though without giving any hints that tightening is being considered.

Q1 GDP is due on Thursday and Wednesday’s data could bring some late fine tuning to expectations. We expect a healthy 2.6% annualized rise, lifted by a rebound in government from a shutdown-depressed Q4. Core PCE prices are likely to look strong, with a rise of 4.1%. March’s personal income and spending report will be released with, and contribute to, the GDP report. We expect spending at 0.9% to outperform a 0.2% rise in income, while we expect a 0.7% rise in PCE prices, with core PCE prices up by 0.3%. Also due are weekly initial claims, and the Q1 Employment Cost Index, which we expect to increase by 0.8%. On Friday we expect a stronger ISM manufacturing index of 53.5 for April, up from 52.7 in March.

CANADA

The Bank of Canada meets on Wednesday and is likely to leave rates unchanged at 2.25%. While higher energy prices will lift forecasts for overall CPI, with core inflation falling and activity and employment looking subdued the BoC is unlikely to adopt a more hawkish tone. February GDP is due on Thursday, and we expect a 0.3% increase, but with less impressive preliminary indications for March.

JP

The BoJ Meeting will be held on Tuesday. While market pricing for an imminent hike has been trimmed, we believe the call is 50-50 between April and June. The oil shock has been mostly covered by extension of stimulus but they maybe worried about contagion if geopolitical disruption last past June. Else, Tokyo CPI on Friday would be more important than other tier two releases throughout the week. Widely expected headline CPI will remain below 2% and core-core around target band.

AU

The Q1 and March CPI will be released on Wednesday. Quarterly CPI and Trimmed mean CPI are both likely above 3% but should see some signs of moderation, before the energy spike. The monthly figure will be more specific on the impact of rising energy prices and we could see a strong hawkish read.

NZ

Only business outlook, confidence on Thursday and Consumer confidence on Friday.

Recap of the Week

Iran Conflict Persists

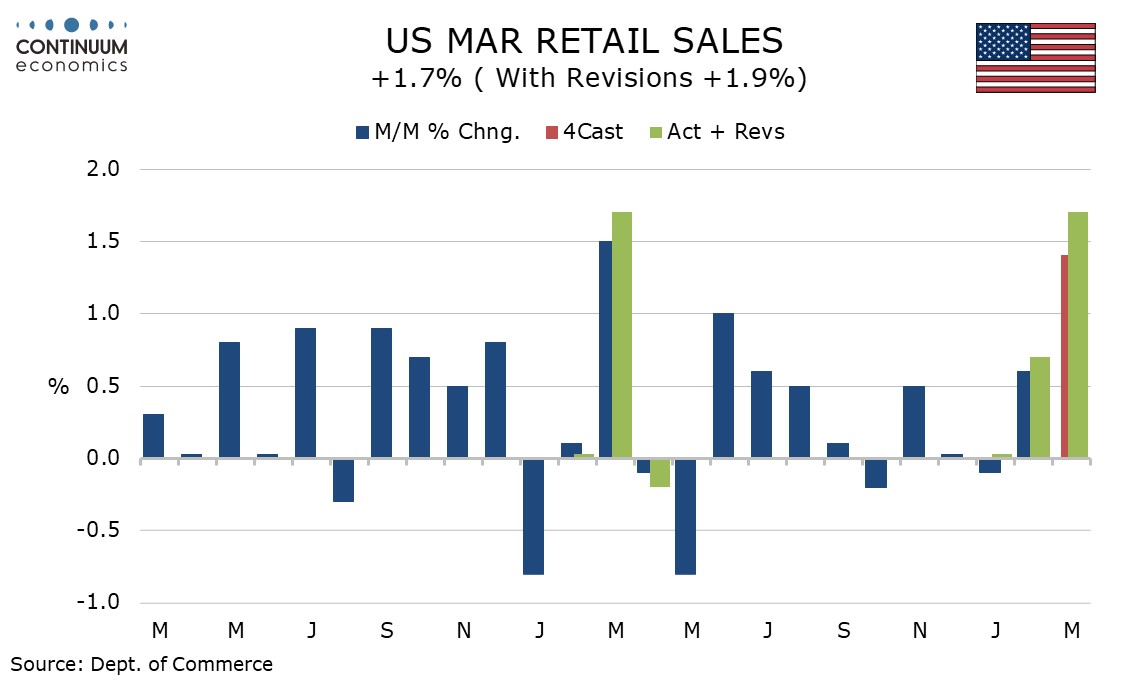

U.S. March Retail Sales Show Underlying resilience

DXY Pushing higher

UK Inflation Being Fuelled But Wages Still on the Wane

UK Labor market Hemorrhaging

Seemingly the ceasefire has been extended, not surprising given Trump’s repeated about-turns (even on Tuesday alone) and the fact that both Iran and the US want peace, the latter enough to temper any attempt by Israel to resume hostilities ahead of its election due later this year. Each side has an obvious different rationale for this; Iran is exhausted economically and militarily while the U.S knows the growing risks to it and the world economy if the Straits remain effectively closed, blocking off oil and other vital commodities. Meanwhile, the U.S is realising at least implicitly that it has persistently over-estimated its ability to use its undoubted military superiority to reach its goals regarding Iran. But the U.S still seems to be over-estimating Iran’s ability and willingness to reach a so-called ‘deal’ in the very short-term. Iran may re-open the Straits in due course (chiming with our base line scenario) but any peace deal may be far off, if at all; after all Iran and the U.S have been at loggerhead of nearly 50 years!

March retail sales with a 1.7% rise, 1.9% ex autos are stronger than expected. Most of the rise is on the surging price of gasoline, though sales ex auto and gasoline with a 0.6% increase are on the firm side of expectations, with February revised up to 0.6% from 0.4% and January to 0.4% from 0.2%. Tax cuts passed in 2025 have lifted tax refunds in early 2026 and are in part offsetting the rise in gasoline prices.

Revisions overall were less strong than for ex auto and gasoline sales, with February revised up only marginally to a 0.7% rise from 0.6% and January now unchanged rather than declining by 0.1%.

Anticipated gains have broken above 98.50 to reach 98.74, where unwinding overbought intraday studies are prompting short-term reactions. Daily stochastics continue to rise and the daily Tension Indicator has turned positive, highlighting room for continuation towards resistance at congestion around 99.00 and the 99.18 high of 8 April. However, negative weekly charts should limit any immediate tests of this range in renewed selling interest/consolidation. Meanwhile, a close back below 98.50 would turn sentiment neutral and prompt fresh consolidation above congestion support at 98.00.

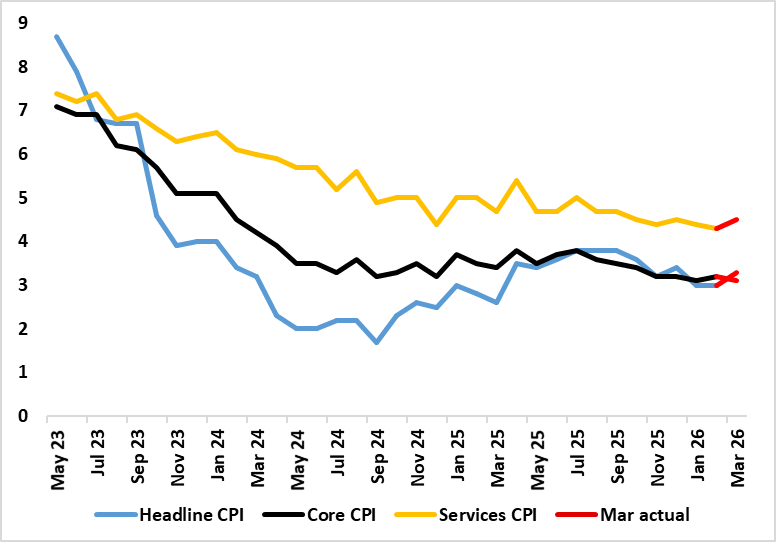

Figure: Headline Stable But Core Higher

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a four-year low (Figure) to .5% on the back if what may have been early Easter induced airfare rises, but the core still edged down a notch due to lower non-energy good inflation (Figure). The markedly and relatively greater surge in diesel relative to unleaded fuel warrants a hardly surprising upgrade to the price outlook for the rest of the year. On the basis of our baseline 4-8 week war thinking, we see the headline CPI falling back for in April before moving back higher in May in Q4 but then dropping back to end the year to 2027 at just over 2.5% but with the 2027 picture little changed, not least as tightening financial condition bite and soft wage pressures persist.

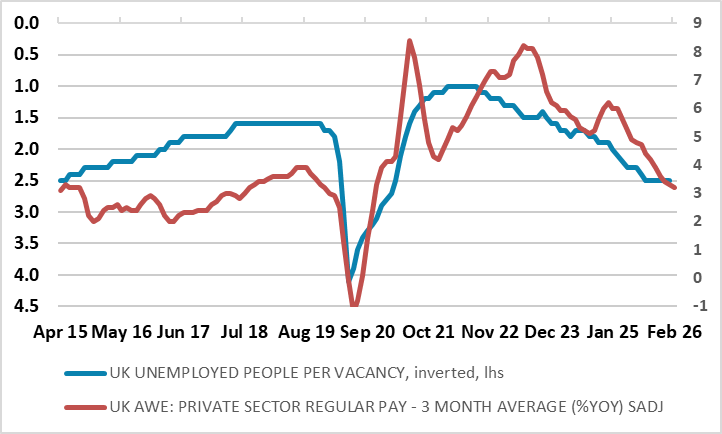

Figure: Labor Market Loosening Taking Toll on Wages

There are further signs that the labor market is haemorrhaging jobs both clearly and broadly with fresh falls in the more authoritative measure of jobs covering payrolls. Indeed, private sector payrolls are still falling, down over 0.5 ppt in y/y terms. Admittedly, headlines may be formed around a surprise fall in the jobless rate to 4.9% but this is in no way any sign of fresh tightening the labor market. Instead, it reflects a rise in in inactivity, possibly reflecting dashed hopes of finding a job, especially among students. This is not surprising given the further fall in vacancies. Indeed, the ratio of vacancies to unemployed – perhaps a better guide of labor market tightness than the jobless rate as it reflects both the supply and demand for labor continues to trend lower (Figure). As a result, it does seem as if this is at least partly behind the further fall in wage pressures. Indeed, private sector regular earnings are now running at below 3%, the lowest since pandemic related pressures softened them in mid-2020.