UK GDP Preview (Apr 16): Moving Sideways Even Before Conflict?

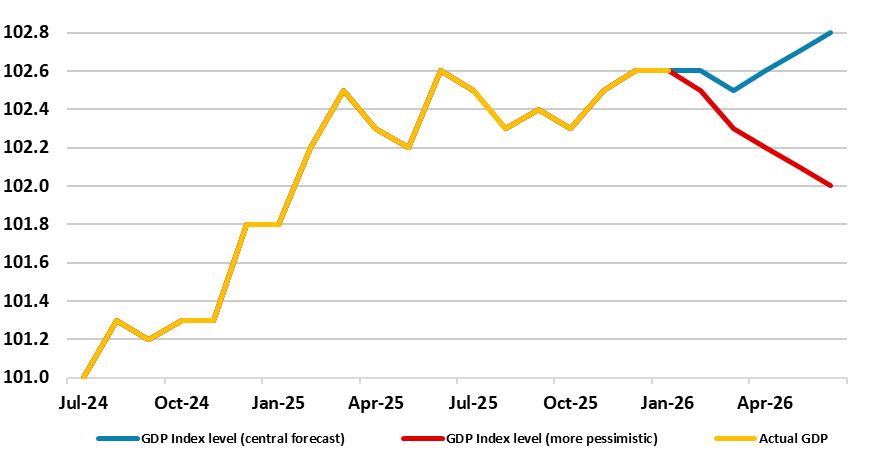

Fresh downside surprises were the story from the January GDP numbers and we expect a similarly muted outcome for the looming February numbers. There were expectations that the economy would enjoy a further successive rise in January, thereby providing the best three-month showing in two years were dashed as GDP instead stagnated and we see a further unchanged m/m figure for February. Weakness or at least lack of momentum is likely to (again) be broad-based in spite of a possible bounce in real estate. But, as is familiar with recent UK real economy data, we still suggest that even with modest war-induced March GDP decline, it looks more likely that growth last quarter will be no better than the 0.1% q/q seen in Q4, less than consensus and BoE thinking, at least as envisaged back in February for the latter. Moreover, there may be downside risks as activity (Figure 1) and sentiment will, of course, be hit either earlier and/or more severely by events in the Middle East (Figure 2).

Figure 1: GDP Growth Hardly Strong and With Increasing Downside Risks Ahead?

Source: ONS, CE - 2023=100

Even without the Middle East conflict impact, we were suggesting a sub-consensus 2026 GDP picture of 0.8%. Now, while recession may be avoided, the economy is likely to be even weaker ahead as the backdrop and outlook has changed - we have highlighted several scenarios as to how the Middle East conflict will pan out, with our 4-8 week war baseline looking somewhat more likely at this juncture. But where we see oil and gas prices largely falling back to the pre-war levels within a year, this still results in UK CPI inflation being some 0.5 ppt higher than otherwise, ending this year at 2.5%. Even so, we are also skeptical about meaningful second round effects occurring, not least given the softer labor market likely to accentuate real income woes. Indeed, even if inflation expectations rise further this is unlikely to result in higher wage deals given the ever-clearer loosening state of the labor market and the likely squeeze on profit margins firms may now face. This will be a reflection of an economic backdrop where GDP growth may be as low as 0.5% this year, ie almost half the BoE’s pared-back projection made in February. This reflects already weak demand which we think at least partly reflects tighter financial conditions.

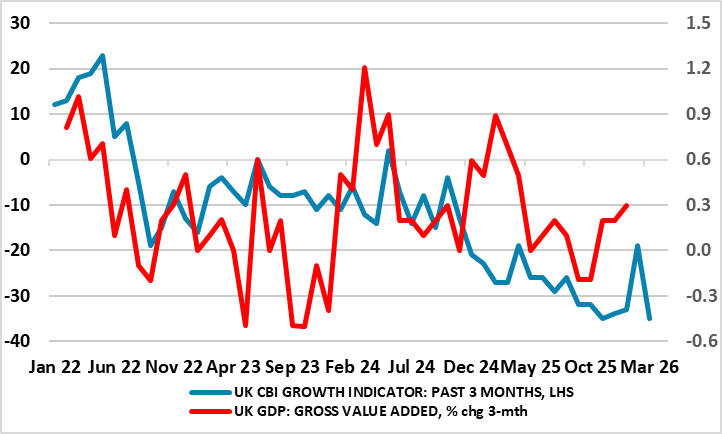

As for the outlook and perspective, 2025 growth was 1.4%, three notches above that seen for 2024. But as suggested above we are pointing to no more than 0.5% this year; this actually encompassing a minor pick-up into H2 from the anemic growth seen in the last two quarters. Regardless, we remain wary about the GDP numbers, even given their relative weakness. Although there have been some better business survey numbers, these seem to have ebbed under the weight of war worries (Figure 2).

Figure 2: Surveys Had Started to Offer Better Signals?

Source: ONS, CE, CBI

But obviously, the inflation and negative growth implications of the Middle East conflict complicates matters to put it mildly. But the February backdrop is somewhat clearer given the hard and soft data available, including the recorded small m/m drop in retail sales, that possibly having succumbed to a month with very heavy and persistent rainfall. The latter may have undermined construction too, this possibly evident in the very much sub-50 PMI readings for the sector. Manufacturing looks to have been flat amid what have been volatile car production numbers of late. Overall, we see a second successive flat m/m GDP outcome in February to be followed by a small drop last month and then a resumption of very gradual growth thereafter – but with clear downside risks (Figure 1).