German Data Review: Mixed Inflation News but Politics Dominate?

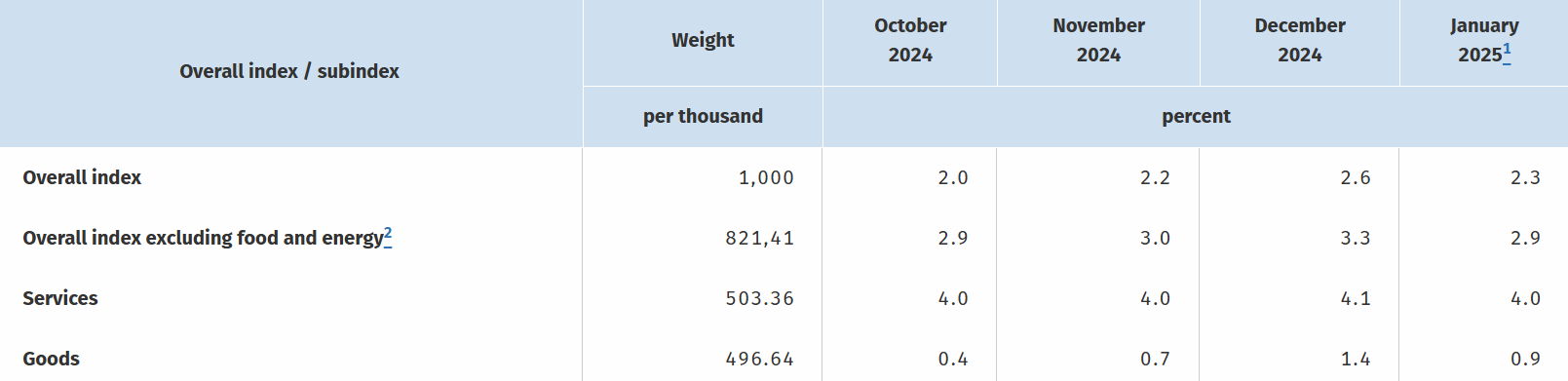

As Germany faces possibly deeper and more prolonged political deadlock, its disinflation process continues, but there are signs that the downtrend is flattening out and this may be the message into the rest of 2025. Indeed, January HICP inflation stayed at 2.8% an outcome largely as expected. But perhaps clearer disinflation news was event in the national CPI news which fell 0.3 ppt to 2.3%, thereby reversing most of the energy-led jump seen in December. It is likely that the discrepancy between the CPI and HICP may lie on the fact that the latter’s resilience may reflect re-weighting issues, but may also be consistent with the marked 0.4 ppt reversal in the January core rate, but with the main softening coming via lower food inflation as services inflation was little changed.

Figure 1: Services Inflation Persistence?

Source: German Federal Stats Office, % chg y/y

While a further fall in the next month beckons, again due to energy base effects, survey data are pointing not only to more real economy weakness but significant falls in cost and output price pressures. This chimes with weak adjusted core CPI readings from Germany, something we think continued in the January data. Overall, we see HICP headline inflation averaging around, if not just under 2% this year!

But the inflation news is of secondary importance in Germany to politics with immigration now dominating the headlines as the election looms next month. Election favourite CDU are suffering internal strife over an immigration bill they have put forward but which would need the support of the alienated right-wing AfD party. What this means is that the CDU which may still be the targets party after the election may find it difficult to find stable coalition partners and thus the risk of prolonged political uncertainty is rising, thereby impairing forming and carrying out policy. However, there are suggestions that the CDU is negotiating with both the SPD and the Greens (ie the likely coalition partners) about the possibility of getting a majority without the AfD, by amending the proposed legislation.