UK GDP Review: GDP Upside Surprises Continue, Correction Due or Fresh Trend?

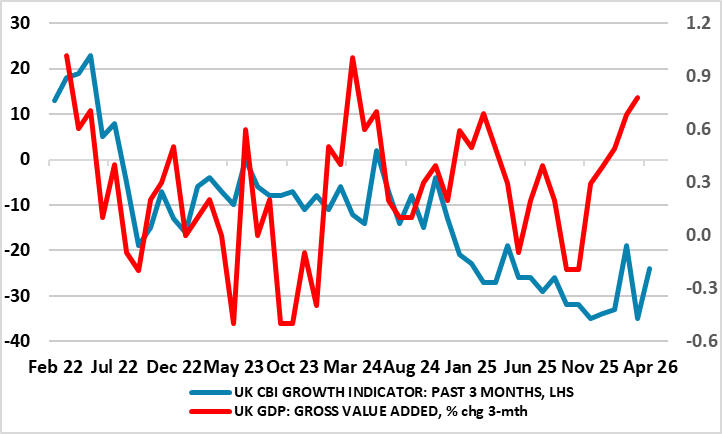

Perhaps it is a supreme irony that just as the Labour government tears itself apart after disastrous election results last week, the actual real economy continues to surprise on the upside. Notably, since taking office in July 2024, the economy has grown a cumulative 2%-plus, ie over 1% per year. Indeed, providing yet more signs of apparent economic resilience and, once again exceeding expectations, GDP grew by 0.3% m/m in March 2026, following growth of 0.4% in February and no growth in January (each revised down by 0.1 ppt). Services and construction output both grew, by 0.3% and 1.5%, respectively the later the main factor behind the overall successive upside surprise but where these growths were partially offset by a 0.2% fall in production. The question is whether this more recent growth is illusory, not chiming with business survey data (Figure 2) and where it may reflect even further inventory building, most recently prompted by the outbreak of the Iran War.

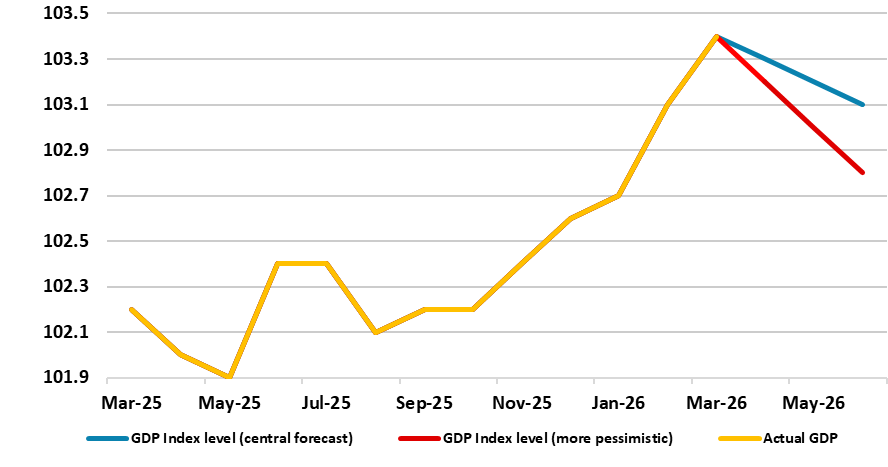

Figure 1: GDP Growth Hardly Strong and With Clear Downside Risks Ahead?

Source: ONS, CE

Before the outbreak of the Iran War there was already a split within the MPC about the policy outlook and such divisions may be accentuated by the much stronger GDP update of late which showed a q/q Q1 rise of 0.6%, the strongest in seven quarters. Indeed, Q1 GDP was boosted by inventories (again) but also by household spending, both probably responsible for a further negative net trade contribution. As for the marked m/m gains of late the question is whether this more recent growth is illusory, not chiming with business survey data (Figure 2) and where it may reflect even further inventory building, most recently prompted by the outbreak of the Iran War. In this regard, the March rise exceeds BoE thinking. With this in mind, base effects are strong enough to mean anything weaker that a timid 0.1% outcome in the current quarter after the 0.6% Q1 result, outcomes enough to push GDP growth this year to over 1% this year (as opposed to our previous 0.6%).

But of course, the conflict has changed everything, very much accentuating uncertainty, economic priorities, all shifting the policy debate from the size and speed of further easing to what extent policy needs to be tightened to dampen any second round effects from the current energy prices surge.

Figure 2: Surveys Offering Much Softer Signals?

Source: ONS, CE, CBI

Notably, Governor Bailey does seem to be suggesting that the BoE will be in no rush to hike and we do not think this dubious GDP data will change his and most MPC thinking Haskell today mentioned some long-lasting skepticism about the GDP numbers. We very much side with Bailey’s thinking, noting that even with the surprise momentum the UK may have had ahead of the conflict, it is still very modest compared to that seen four years ago when the Ukraine War precipitated the last energy price surge. This is especially so in regard to the consumer with clear implications for inflation risks. But with somewhat higher baseline energy price assumption, we no longer see any easing this year, instead deferring the easing we envisaged to 2027. Admittedly, rate hikes still seem to be the more likely policy response more implicit in BoE thinking, with some suggestion that without them then the tightening in financial condition seen of late would not be validated. We think this is misplaced, not least as some of the tightening in conditions reflects the likes of political and fiscal risks