UK GDP Preview (May 14): March GDP Drop Expected, Correction or Fresh Trend?

Before the outbreak of the Iran War there was already a split within the MPC about the policy outlook and that such divisions may have been accentuated by the much stronger than expected February GDP update which showed a m/m rise of 0.5%, the strongest in 14 months. This is likely to have been aberrant figure and we expect to see some correction of 0.2%-0.3% in the March update even with further warm weather, consumers hoarding and the impact of the early Easter. Notably, this projection tallies with BoE thinking but the question is whether any such a drop is merely a correction to the February upside surprise or heralds a much weaker trend in the aftermath of the surge in energy costs and related added uncertainty. In this regard, tend to the later and see a fresh q/q dip in the current quarter after a 0.5%-0.6% Q1 result, enough to curb GDP growth this year to just 0.6%, this actually being notch below the BoE’s adverse persistent energy shock scenario.

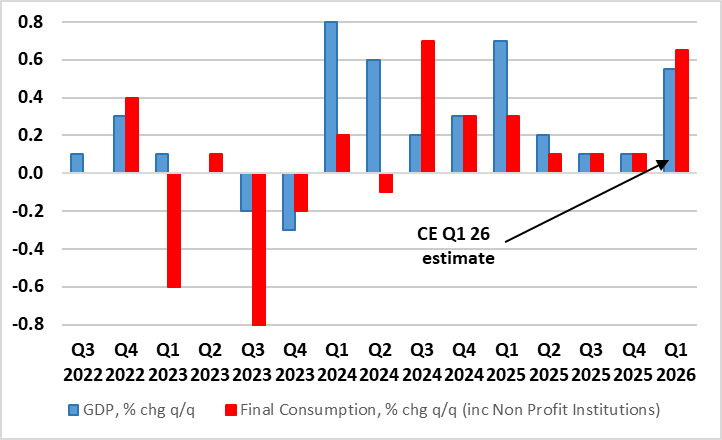

Figure 1: Despite Likely Q1 Jump, GDP Growth Hardly Strong and With Increasing Downside Risks Ahead?

Source: ONS, CE

And of course, the conflict has changed everything (Figure 1), very much shifting the policy debate from the size and speed of further easing to what extent policy needs to be tightened to dampen any second round effects from the current energy prices surge.

Notably, Governor Bailey does seem to be suggesting that the BoE will be in no rush to hike. We very much side with Bailey’s thinking, noting that even with the surprise momentum the UK may have had ahead of the conflict, it is still very modest compared to that seen four years ago when the Ukraine War precipitated the last energy price surge. This is especially so in regard to the consumer with clear implications for inflation risks.

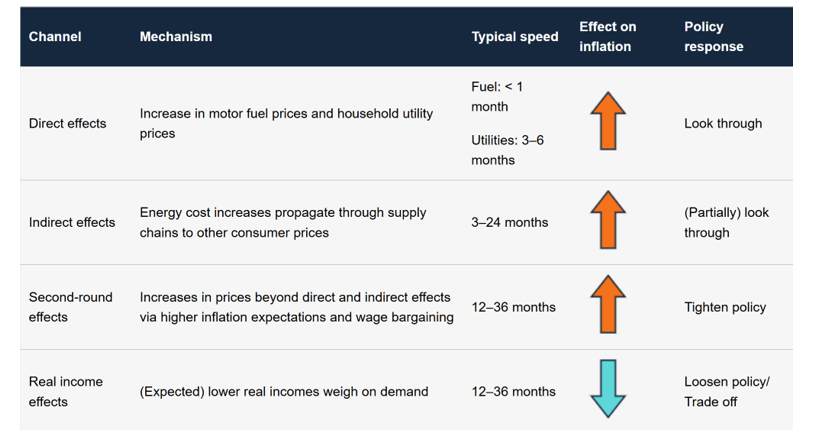

Admittedly, rate hikes still seem to be the more likely policy response more implicit in BoE thinking, with some suggestion that without them then the tightening in financial condition seen of late would not be validated. We think this is misplaced, not least as some of the tightening in conditions reflects the likes of political and fiscal risks. As for the three BoE scenarios in the April MPR (A seeing energy prices follow market thinking while C sees not only higher energy costs but more persistently too) we are puzzled that the combination of the energy shock and more restrictive policy not only fails to deliver any kind of recession even in the most severe scenario, this being important as demand damage is an important component of the BoE reaction function (Figure 2). Indeed, all three outcomes see little variation in the growth outlook – ie just 0.1 ppt per year between each outlook – albeit this variation being much larger than in the similar ECB scenarios.

Figure 2: Demand Damage Key Part of BoE Reaction Function

Source: BoE Apr MPR – How global energy shocks can affect UK CPI inflation and possible monetary responses

Instead, and as the IMF last month underlined the real economy fall-out the UK may face could be the most sizeable for any major economy. This is very much evident already in business survey data, perhaps best seen in the aggregated numbers produced by the CBI which chime with the GDP data in suggesting some improvement in February but which also suggest that such a pick-up was very short-lived.

As for the actual March numbers, m/m GDP grew by 0.5% in February 2026, following growth of 0.1% in January (revised up from zero previously) and 0.1% in December 2025. We see half that rise being corrected back, even with several supportive factors. Indeed, March saw further warm weather, consumers hoarding (particularly petrol) and there was also the impact of the early Easter

Even with this likely correction in March we now see that Q1 GDP may rise by over 0.5%-0.6% q/q but some of this will be countered by what may now be a flat(ter) Q2 outcome or more likely a small q/q dip. If so, this would mimic what has been seen in recent years when GDP showed relative strength early in the year, only to falter into the second halves, thereby questioning seasonal adjustments. Regardless, we now see 2026 GDP a notch or two higher than previously expected but a 0.6% projection would still be below consensus and under that anticipated by the BoE even under is more pessimistic scenario.