China: Modest Bounce at Start of 2026, But

· Though the January-February data was better than expected, we expect high oil prices and an adverse effect from the Iran war to hurt China’s export growth. We still feel that the economy remains too dependent on high tech manufacturing and modest consumption will act as a drag on GDP growth. Additionally, China’s authorities remain reluctant to be aggressive. We stick with 4.2% GDP growth for 2026.

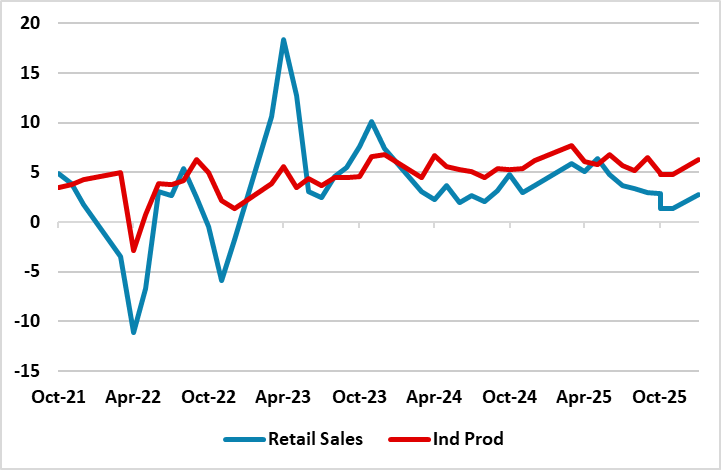

Figure 1: Industrial production and Retail Sales (Yr/Yr %)

Source: Datastream/Continuum Economics

The January-February data was better than expected, but should not be regarded as a sign of a pick-up in the economy.

· Retail sales helped by Lunar New Year. 2.8% YTD Yr/Yr versus 2.5% came largely from the longer than normal lunar new year holidays, with catering up 4.8% v 2.2% seen in December. New car sales remain weak showing that households remain reluctant in buying big ticket items.

· Industrial production helped by exports. The 6.3% rise YTD Yr/Yr is better than market expectations of a 5.3% rise and is likely to be partially due to the surge in exports. However, it is questionable whether this will be continued, both with the slowdown in the global economy with the Iran war and also as other countries are getting wary of China export dumping. Meanwhile, fixed investment surprised and rose 1.8% YTD Yr/Yr versus expectations of 5.1% decline, as infrastructure investment surged in the first two months of the year. This appears to reflect better coordination of spending by central and local governments, which had hurt investment in H2 2025.

· Residential investment less bad. Residential property investment beat expectations at -11.1% YTD Yr/Yr versus the -19.3% expected. This should be viewed as the situation in housing getting less worse at the start of the year. New home sales were still down 13.5% Yr/Yr, while an excess of complete and incomplete homes remains.

· 4.2% GDP growth for 2026. Though the data was better than expected, we expect high oil prices and an adverse effect from the Iran war to hurt China’s export growth. We still feel that the economy remains too dependent on high tech manufacturing and modest consumption will act as a drag on GDP growth. Additionally, China’s authorities remain reluctant to be aggressive, with the 4% central budget deficit for 2026 being in line with the modest 2025 fiscal stimulus. Meanwhile, PBOC remains reluctant to cut interest rates, as it could squeeze bank margins and hurt bank lending. Even so, we would still see a 10bps cut in Q3 2026 in the seven day reverse repo rate.