Sweden Riksbank Preview (Sep 25): Rate Cuts – Faster and Further?

A third successive 25 bp rate looms at this month’s Riksbank meeting verdict (Sep 25) to 3.25%. More notably, updated forecasts are likely to more formally validate the rationale for the two added cuts by end-year that the Board hinted at after the August easing and which now seem all but certain. Indeed, the new projections in the fresh Monetary Policy Report (MPR) may highlight that while lower inflation has provided the scope to ease policy in this speedier manner, the rationale is increasingly that from a weak economy. The latter is likely to be highlighted by a marked downgrade to the Riksbank’s’ 2024 GDP picture, but where its above trend 1.9% 2025 may be kept intact, albeit solely a result of the faster easing in its monetary stance bow being flagged. The big question is whether the Riksbank will point to additional easing over and beyond the circa-2.5% terminal rate its existing projections suggest may be the case. We think not, at least not at this juncture, but think eventually that the Board will embody a resting rate of 2.25% to be in place by early-2006.

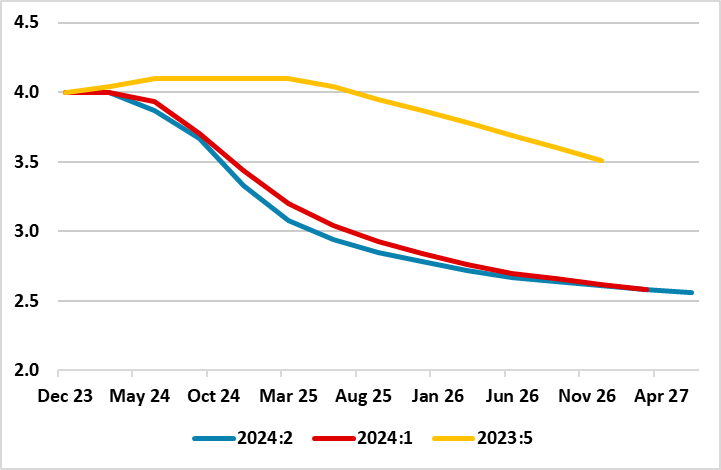

Figure 1: Policy Outlook Details – Out of Date?

Source: Riksbank last three Monetary Policy Reports

Since the spring, it was very much a question of how fast, not if, as far as policy easing was concerned for the Riksbank, with Figure 1 underscoring how policy thinking has been markedly reshaped this year. From the Board’s perspective, by initiating easing relatively early in May, it was both reacting to weak data (both real and price wise), but more notably in giving itself flexibility to pursue what it then thought needed to be a gradualist approach to further easing. That now seems to be changing with policy put into a faster gear to front-load, both a result of an undershoot of inflation (partly energy related but ever clearer in terms of short-run dynamics) but also due to a still weak economy which has failed to grow on balance since end-2021, albeit with clear quarter-to-quarter volatility.

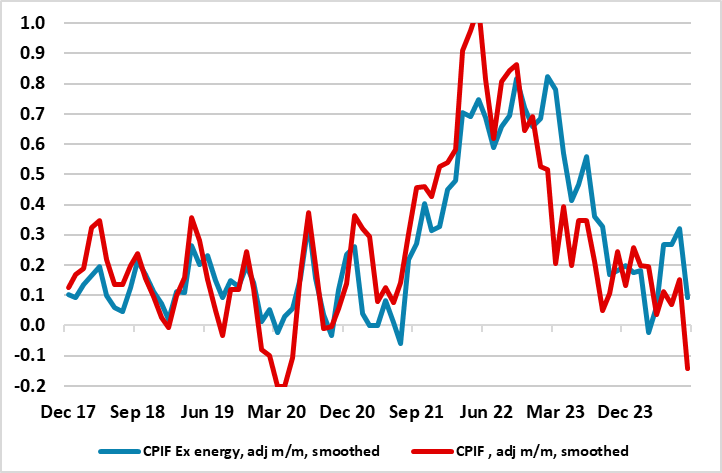

Figure 2: Short-term Inflation Dynamics Down Markedly

Source: Stats Sweden, CE, smoothed it 3-mth mov avg

Terminal Rate Considerations

Especially given the seemingly-feeble Q2 GDP reading, this reinforces our relative pessimism about the scale of the recovery. But even with the Riksbank pointing to the economy picking up and growing in 2025 at and then above trend at over 2% in 2026, this still generates a negative output gap of over 1% of potential GDP and only turns positive into 2027. We think this growth outlook is somewhat optimistic. But the point is that the Riksbank still accepts that even this more upbeat real economy outlook delivers price stability, if not a risk of a persistent slight target undershoot. Admittedly the updated MPR may rein in growth expectation somewhat but probably keep the profile after this year largely intact. This would reflect not only the faster easing but the fact that Sweden is far more sensitive to short-term Rate changes given that the bulk of the housing market is still biased to variable rate mortgages.

The question is, if growth disappoints into 2025, will the Riksbank ease further than it is now flagging – much may depend on fiscal policy with the 2025 Budget due next month! But given our economic projections, we now see two further cuts this year over and beyond that envisaged this month but also to the slightly speedier and more extended journey to a 2.25% policy rate we now see occurring by end-2025!