UK GDP Review (Apr 16): Fresh But Fleeting Momentum Before the War

Without the outbreak of the Iran War there was already a split within the MPC about the policy outlook and that such divisions may have been accentuated by this latest GDP update which showed a very much above consensus m/m rise of 0.5%, the strongest in 14 months. But of course, the conflict has changed everything (Figure 1), seemingly shifting the policy debate from the size and speed of further easing to what extent policy needs to be tightened to dampen any second round effects from the current energy prices surge. Notably, Governor Bailey has just suggested the BoE will be in no rush to hike, all the more notable as his comments seem to suggest that he is speaking on behalf of the MPC as a whole or at least a large majority. We very much side with Bailey’s thinking, noting that even with the surprise momentum the UK may have had ahead of the conflict, it is still very modest compared to that seen four years ago when the Ukraine War precipitated the last energy price surge. This is especially so in regard to the consumer (Figure 2) with clear implications for inflation risks.

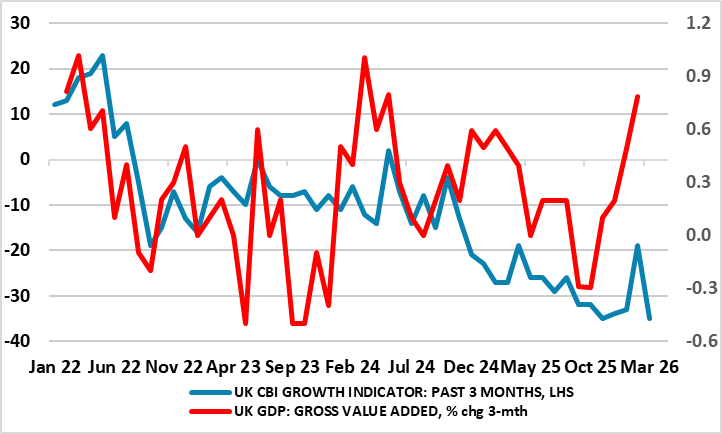

Figure 1: GDP Growth Hardly Strong and With Increasing Downside Risks Ahead?

Source: ONS, CBI, CE

Instead, and as the IMF this week underlined the real economy fall-out the UK may face could be the most sizeable for any major economy. This is very much evident already in business survey data, perhaps best seen in the aggregated numbers produced by the CBI which chime with the GDP data in suggesting some improvement in February but which also suggest that such a pick-up was very short-lived.

As for the actual February numbers, m/m GDP grew by 0.5% in February 2026, following growth of 0.1% in January (revised up from zero previously) and 0.1% in December 2025. As for sectors, services and production both grew by 0.5%, and construction grew by 1.0% in February 2026. This still means that GDP rose by only 1.1 in y/y terms, ie still below what may be feeble potential.

Even with a likely correction in March (envisaged even given some upside risks posed by the early Easter) we now see that Q1 GDP may rise by over 0.4% q/q but some of this will be countered by what may now be a flat(ter) Q2 outcome. If so, this would mimic what has been seen in recent years when GDP showed relative strength early in the year, only to falter into the second halves, thereby questioning seasonal adjustments - this backed up by the manner in which GDP has departed fro what surveys have been suggesting (Figure 1). Regardless, we now see 2026 GDP a notch or two higher than previously expected but a 0.6% projection would still be below consensus and under that anticipated by the IMF this week.

But for the likes of the BoE this data is interesting but still largely history as Bailey’s remarks (‘we’re not going to rush to judgments on those things, because there are a lot of uncertainties around this’) suggest data is needed to asses both the real economy and inflation repercussion of the conflict. Indeed, even the MPC hawks point to some circumspection; Megan Greene said yesterday markets were justified in scaling back speculation on interest rates hikes which at one stage recently factored in up to four 25 bp increases, although she suggested the current market position of not more than two hikes is ‘about right’.

Figure 2: Consumer Far Weaker than Four Years Ago?

Source: ONS, CE – q/q % chg in consumer spending

What is important is the marked difference in the current position of the UK economy to that of four years ago, not just in terms of the current policy stance, where prevailing inflation is and how tight the labor market is. But also there is a clear contrast in terms of demand, particularly that of the consumer, this being vital in assessing the size and length of any impact in determining how persistent any inflation surge may be. As Figure 2 shows, even on the basis of Q1 2026 consumer spending growing by around ¾% q/q as he consensus currently expects, this would still be far less that that seen both before and then in the first one-two quarters of the energy prices shock four years ago.

This is just an added consideration that the BoE will have to assess, but we think that with more negative survey data due in the coming few weeks, a stable policy decision is likely on Apr 30 when the BoE gives both its next policy verdict ad updates its projections. As for the outlook beyond then, the current weak demand backdrop alluded to above at least partly reflects tighter financial conditions. The latter is increasingly important given the manner in which they have tightened of late, practically nullifying recent curs in Bank Rate. As for the latter, given the economic fall-out alluded to above, we side with Governor Bailey's apparent skepticism that the MPC will raise rates and instead continue to think policy will be eased afresh by late-year.