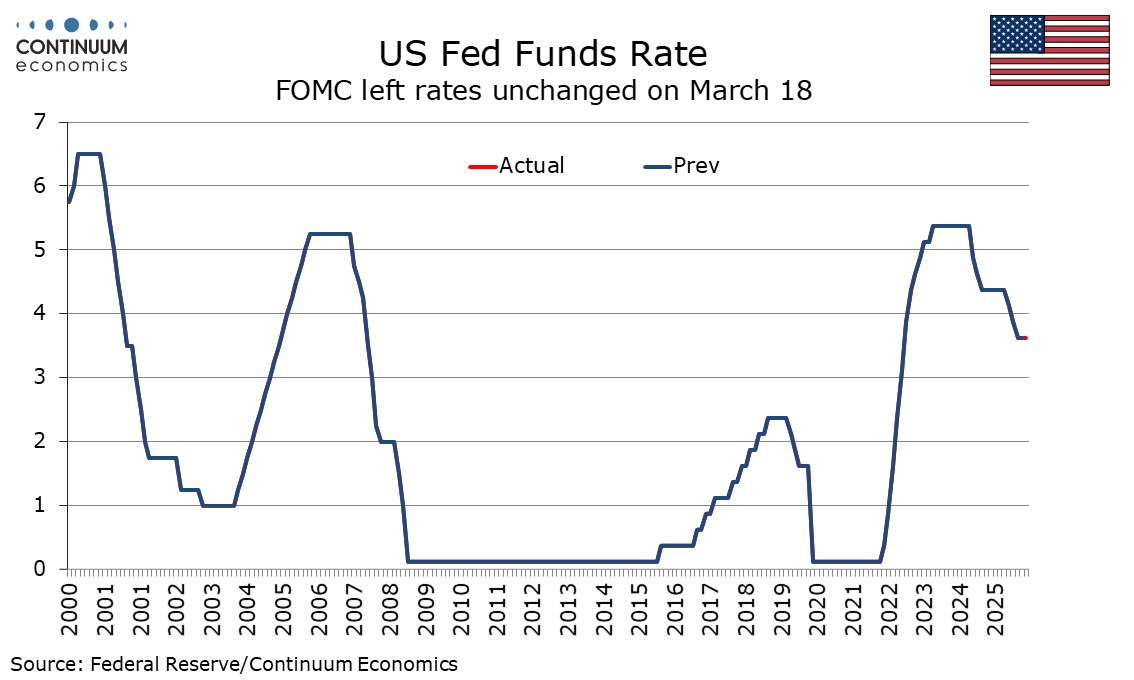

FOMC Minutes from March 18: Increased risks, but still a dovish leaning

FOMC minutes from March 18 show greater concern over inflationary risks but with concerns also seen on risks to employment, do not appear to be hawkish. It still appears that the next move is more likely to be an ease than a hike, even if the timing for rate cuts may have been pushed back somewhat.

The vast majority of participants noted that progress towards the 2% inflation objective could be slower than previously expected. A prolonged conflict in the Middle East was seen as likely to see energy prices passed onto core inflation and persistent inflation was seen making expectations more sensitive to energy price gains. Some noted further progress on inflation had been absent and core goods prices stronger than what is consistent with Fed objectives, and while price increases in housing services had slowed, non-housing core services remained elevated. The labor market was seen as broadly in balance and February’s weak payroll was seen as restrained by a health workers strike and bad weather, suggesting that stronger March data may not have come as a major shock to the Fed. However, the vast majority saw employment risks as skewed to the downside with the labor market appearing vulnerable to adverse shocks. Still, participants generally agreed GDP growth would remain solid in 2026.

Almost all participants favored leaving rates unchanged though one (Miran) backed a 25bps easing. Most agreed it was too early to judge the situation in the Middle East. Many judged that it would likely become appropriate to lower rates if inflation declined in line with expectations, though a couple pushed the timing of this further into the future. Some judged that there was strong case for a two sided description of future rate decisions in the statement, but this does not seem to be a majority view. Most raised the concern that a protracted Middle East conflict could lead to a further softening in labor market conditions, leading to additional rate cuts, while many pointed to the risk of inflation remaining elevated for longer could call for rate increases. That most appears to exceed many suggests the balance of Fed opinion leans dovish within a wide variety of views. Our call remains for 25bps easings in September and December of this year, though risk is later rather than earlier.