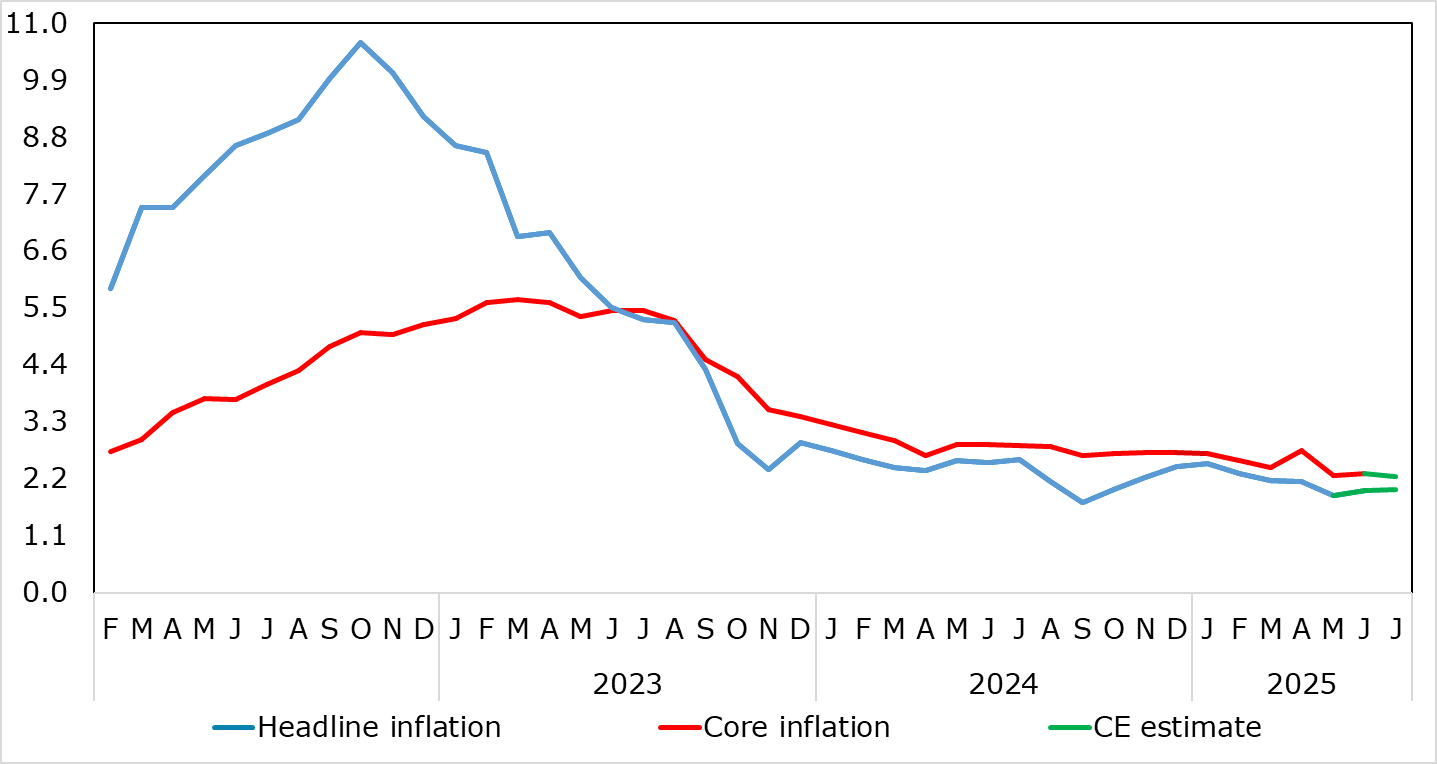

EZ HICP Preview (Aug 1): Headline at Target as Services Inflation at Fresh Cycle-low?

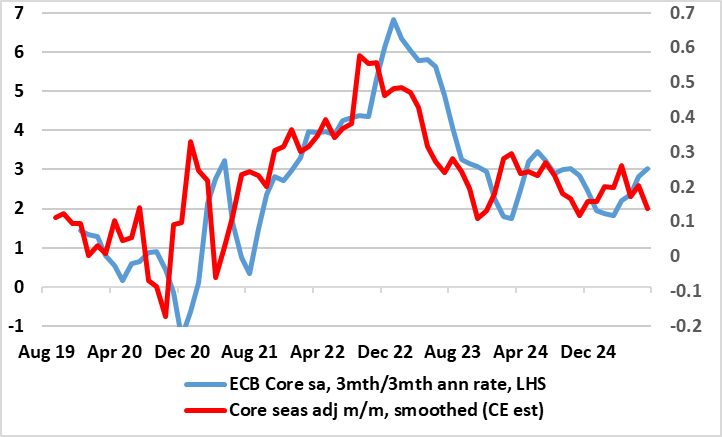

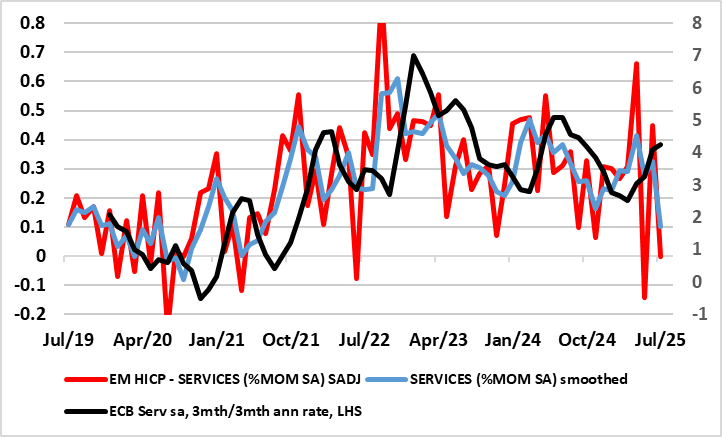

HICP, inflation – now at target – is very much a side issue for the ECB at present, albeit with the likes of oil prices and tariff retaliation possibly accentuating Council divides. Despite adverse energy base effects, we see the flash July HICP staying at June’s 2.0% but up from May’s eight-month low and below-target 1.9% (Figure 1). More notably, and something to calm the hawks, having jumped to 4.0% in April, very probably due to the impact of the timing of Easter we see further calendar effects taking it down to 3.0% in July - the softest since Mar 2022. As a result, the core rate may drop 0.1 ppt to 2.2%, which would be the lowest since Oct 2021. Moreover, as the calendar distortions unwind, what has looked like fresh price pressures in seasonally adjusted short-term m/m movements for core and services are reversing and notably so (Figure 2 & 3)!

Figure 1: Headline Back at Target as Services Hits Cycle-Low

Source: Eurostat, CE, ECB

As for recent HICP swings, Easter effects may have been behind the jump in April unprocessed food inflation too, and also reversed in May but where calendar effects failed to prevent a small fall back in June. Even so, holiday related price distortions reoccurred into June, this possibly explaining services inflation ticking higher again, albeit temporarily.

That April services data may have caused some prevarication within the ECB while some Council hawks may still cite the recent pick-up in supercore and PICC inflation as a cause for concern, alongside more debatable worries related to a fragmentation of global supply chains which they suggest could raise inflation by pushing up import prices while a boost in defence and infrastructure spending could also raise inflation over the medium term. NB such worries will have been diluted by global supply gauges, such as that computed by the NY Fed, still show no sign of anything but sideways, if not downward pressure, on prices! Moreover, while the Q2 HICP met ECB thinking at 2.0%, the core came in 0.1 ppt lower at 2.4%!

Figure 2: Core Inflation Already Around Target in Shorter-Term Dynamics?

Source: Eurostat ECB, CE

Notably, the softer services message seen in recent data was evident even in shorter-term price momentum data where such 3-mth averages still encompass the April surge and the June jump. But this is now unwinding so that, short-term core inflation has slowed and is running around, if not below target (Figure 2) as is the case for services. What this reflects is the emerging impact of softer core pressures, most notably regarding wages. As a result, while the drop in services inflation to 3.0% we seen in July is partly technical and arithmetic, it chimes with softening underling cost pressure trends, most notable wages.

Figure 3: Services Inflation Moving Back to Target in Shorter-Term Dynamics?

Source: Eurostat ECB, CE