UK GDP Preview (Mar 14): Surprise Resilience Despite Surveys Suggesting the Opposite?

After upside surprises in December, the odds are increasing that current quarter GDP will be decidedly positive as opposed to the weak(ish) picture we perceive but which contrasts with a much softer impression from surveys (Figure 1), the latter now showing weakness spreading into hitherto strong construction. Regardless, and despite a clear bounce in retail sales for the month we think, that corrections in other parts of services and continued weakness in industry will cause a small m/m drop in January of around 0.1% m/m. But upside risks stem not just from the sales data, but also cold weather boosting already below-par utility output as well as what may be changing seasonal factors post pandemic which may mean the UK economy in early 2025 sees similar but short-lived strong growth as seen in in the same period of last year.

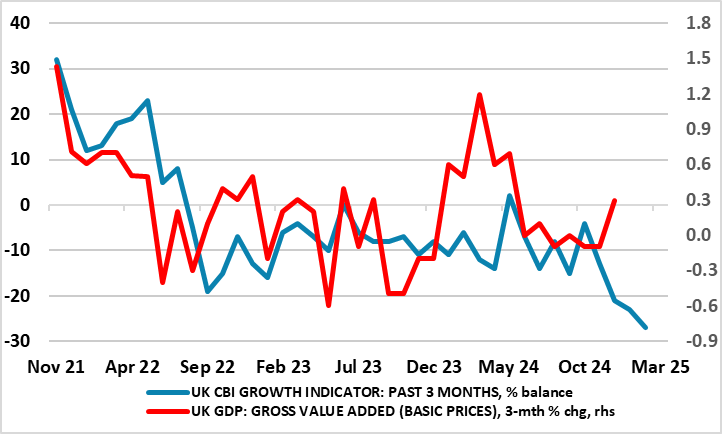

Figure 1: Momentum Recovering Despite Continued Downside Risks From Surveys?

Source: ONS, CBI - Growth Indictor which combines results from three separate sector surveys

At the moment we envisage growth of 0.2 q/q this quarter, but those upside risk suggest it could be double that and this four times what the BoE envisage. The question is what markets and the BoE prioritizes in assessing the policy outlook – weak survey data or apparently resilient official numbers.

As for the backdrop, GDP data for the end of 2024 very much surprised on the upside albeit still failing to convey an impression of UK’s economy displaying solidity, if not strength. Admittedly GDP rose by 0.4% m/m in December, the largest such gain in 11 months and enough to have allowed Q4 see growth of 0.1% as opposed to the largely expected same-sized fall. The data means the economy grew 0.9% in 2024 but amid what looks to be a possible involuntary rise in inventories that supported Q4 GDP and a suspect (ie survey conflicting) jump in manufacturing that boosted December numbers, we doubt that genuine fresh momentum has emerged – GDP per head actually fell. Indeed, we still see growth around 0.7-0.8% for the whole of this year, despite the looming fiscal boost that has persuaded some forecasters to upgrade their projection for the year. Instead we note the sobering message from business surveys as well as from payroll data, all more consistent with tepid if not negative growth (Figure 1) rather than the upbeat growth aspiration of the government.

As we then envisaged, November saw hardly any growth, this almost-0.1% rise came after October saw a second successive m/m drop of 0.1%, all below expectations. But the December rise changes this somewhat weak backdrop even though GDP has declined in half of the last eight months of data during which the economy has growth a mere 0.4%,

This all the more notable as it suggests a weaker trend that dates back prior to the election of the new government let alone its October Budget and its mixed policy measures. Indeed, the Q4 picture shows no growth in consumer spending and a fall in business investment and with the growth very much a result of a build in inventories, albeit this partly offset by a jump in imports.

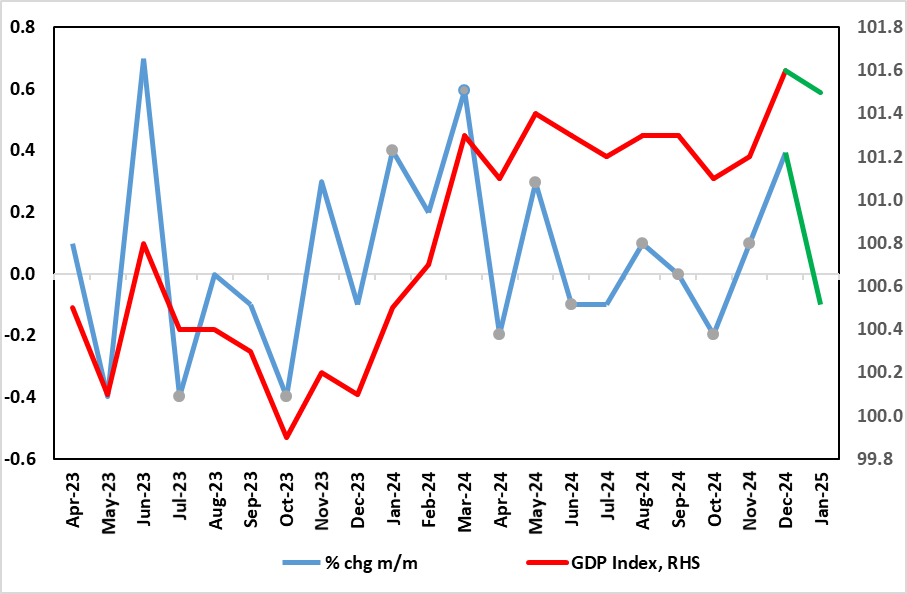

Figure 2: Actual GDP Looking Better into Early 2025

Source: ONS - CE forecast in green

Regardless, and as suggested above, our relative weaker GDP outlook is something that chimes more with labor market and public borrowing data and where HMRC payrolls paint a much softer backdrop and possible outlook. However, while the BoE may still look to a clear recovery later in 2025, any further signs that Budget apprehension and what may now be damaged business and consumer confidence from actual fiscal measures may warrant a reassessment, especially given the added risks posed by likely US tariffs – even if they are now levied significantly on the UK!

Seasonality Shifting?

given what looks to be a weak economic picture in neighbouring Eurozone. In addition, the ONS has noted that the recent CPI volatility may reflect shifts in seasonal activity possibly a result of the pandemic. If so this may mean that seasonal adjustments are failing to capture actual activity. In this regard, it is notable that survey data are painting much more sobering picture, even though they too are reflecting what may be imprecise seasonal adjustments. We note the CBI growth indicator partly as it encompasses a wider measure of private sector activity than used in the PMI, namely retailing, bit also note PMI construction data that have tumbled of late, now suggesting the fastest downturn in construction output since May 2020. Regardless we do note that January GDP could rise clearly again given poor weather boosting utility output and the impact of an already-published bounce in retail sales. If so, we may be looking at a Q1 GDP outcome that could be twice the 0.2% q/q picture we are envisaging (Figure 2).