UK GDP Preview (Jan 16): Continued Weakness?

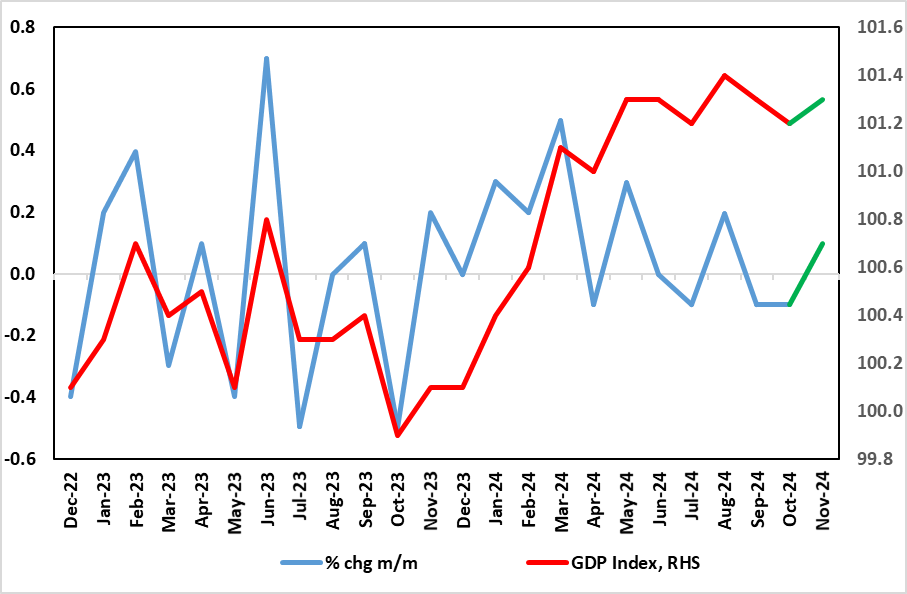

The last set of GDP data add to questions about the UK’s economy’s apparent solidity, if not strength, as seen in sizeable q/q gains in the first two quarters of the year of 0.7% and 0.5% respectively. As we envisaged, October saw a second successive m/m drop of 0.1%, well below expectations, this adding to what have now been only two positive outcomes in the last seven months of data in which the economy has ‘grown’ a cumulative 0.1%. Moreover, even this may be revised away as the monthly data are made to chime with downwardly revised quarterly numbers released just prior to Xmas worth some cumulative 0.2 ppt. Thus the 0.1% m/m rise we envisage for November must be seen in that weak and pared –back context and the likelihood remains that Q4 2024 may have seen a small q/q contraction, ie even weaker than the BoE’s recent downgrade to zero.

Figure 1: Momentum Ebbing – Amid Continued Downside Risks?

Source: ONS, green line(s) are CE forecasts

This all the more notable as it suggests a weaker trend that dates back prior to the election of the new government let alone its October Budget and its mixed policy measures. Although most evident in a further drop in manufacturing, construction weakness re-emerged while services stagnated again. This raises the important policy question as to whether any such weakness suggests that the support from services to the economy seen of late, thereby offsetting manufacturing weakness, is faltering (Figure 2) and where even hitherto upbeat construction activity may be starting to reverse.

Certainly business surveys suggest that may be the case, this putting more emphasis on the PMI update due on 24 Jan. But the data suggest that even with an assumed recovery in the two remaining months of the current quarter, Q4 GDP may not have growth and with a risk that t may have fallen afresh. This is an important consideration for the likes of the BoE which had projected a more upbeat 0.3% GDP rise for the last quarter, albeit that pared back to a zero projection in an update last month.

To suggest that the unexpected GDP drop in September and now October was a result of pre-Budget apprehension is wide of the mark; after all, GDP stopped growing between March and when the new government took office in July. As for the latest details, m/m real GDP is estimated to have fallen by 0.1% in October, largely because of a decline in production output; this follows a fall of 0.1% in September 2024. Admittedly, according to monthly numbers, GDP is still estimated to have grown by 0.1% in the three months to October 2024, compared with the three months to July 2024, with growth in the services and construction sectors in this period. But in m/m terms, services output showed no growth in October 2024 after also showing no growth in September 2024, while production output fell by 0.6% in October 2024, because of falls in manufacturing, and mining and quarrying output, following a fall of 0.5% in September 2024; production output fell by 0.3% in the three months to October 2024. Notably, construction output fell afresh by 0.4% in October 2024, and where a recovery in utility production helped temper the weakness elsewhere. This picture may be revised somewhat as the monthly data are made to fir =t with downgrade quarterly data which now see no growth in Q3

There was a clear boost from real estate given a sizeable jump in house sale, but with something of an imponderable being the public sector which had been clearly boosting activity in H1, but may now be flattening out, if not reversing, at least outside of education. Such weakness has been flagged both by a series of m/m drops in payrolls during the month and by business surveys. As for November, there may be some boost from retailing and utilities (the latter recovering but far from a cyclical development), this offset by weaker car (manufacturing) and possible a slide back in real estate and maybe a weaker public sector. Regardless, the monthly real economy data may be becoming an increasingly important factor in shaping BoE policy ahead, especially if more weakness of the kind we envisage duly occurs.

Figure 2: Are Services Ebbing?

Source: ONS