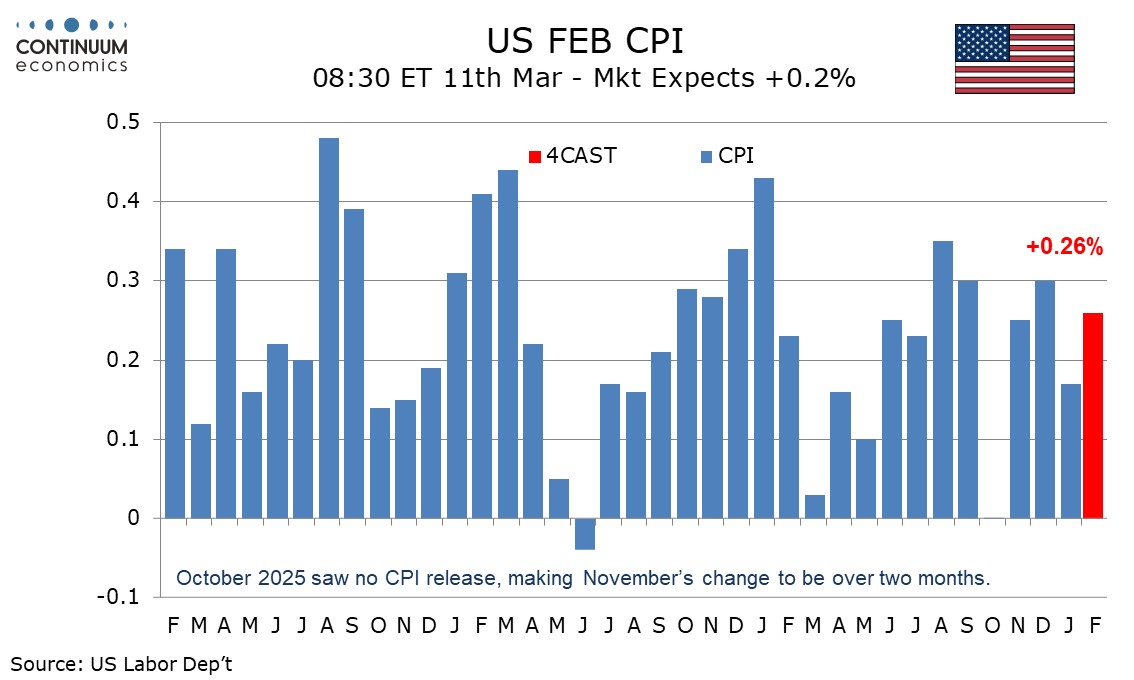

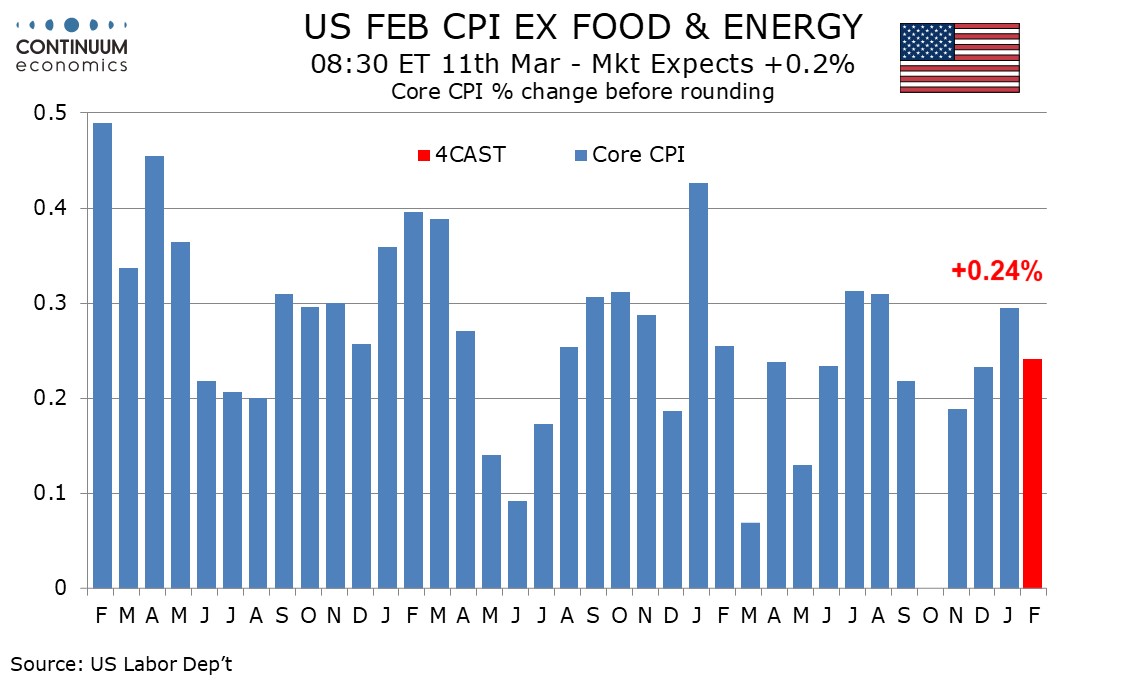

Preview: Due March 11 - U.S. February CPI - A moderate gain, but inflation not yet defeated

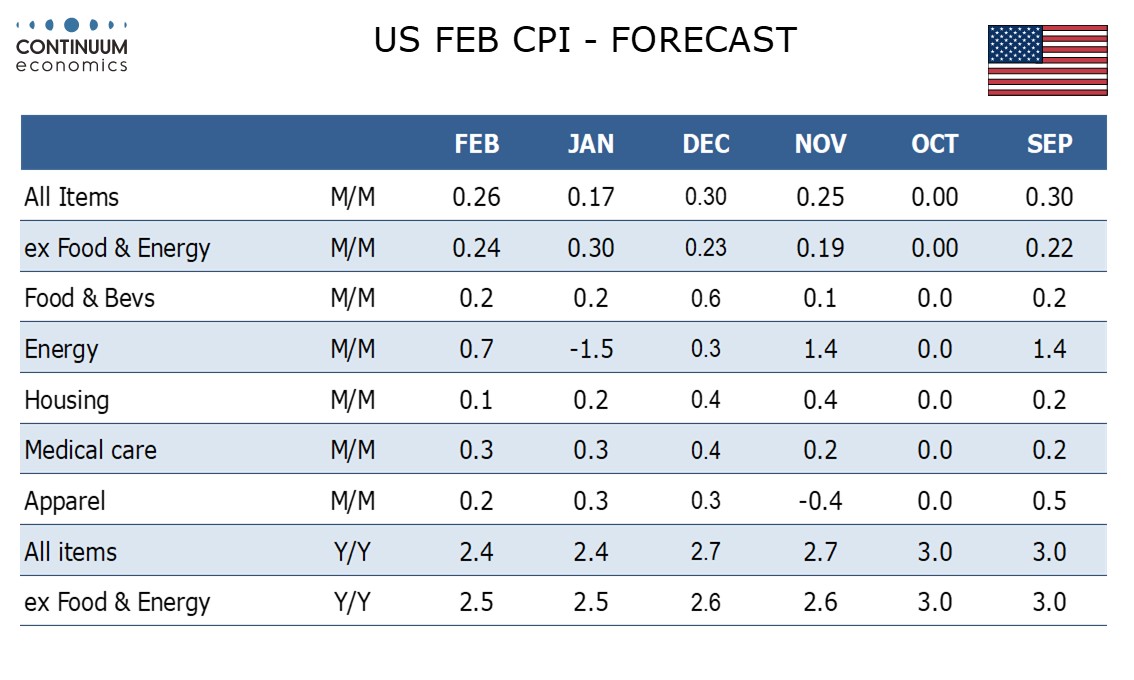

We expect February’s CPI to increase by 0.3%, with a 0.2% increase ex food and energy. Before rounding we expect the gains will be similar, with the overall CPI rounded up from 0.26% and the core rounded down from 0.24%. CPI has slowed, but it is too soon for the Fed to declare victory.

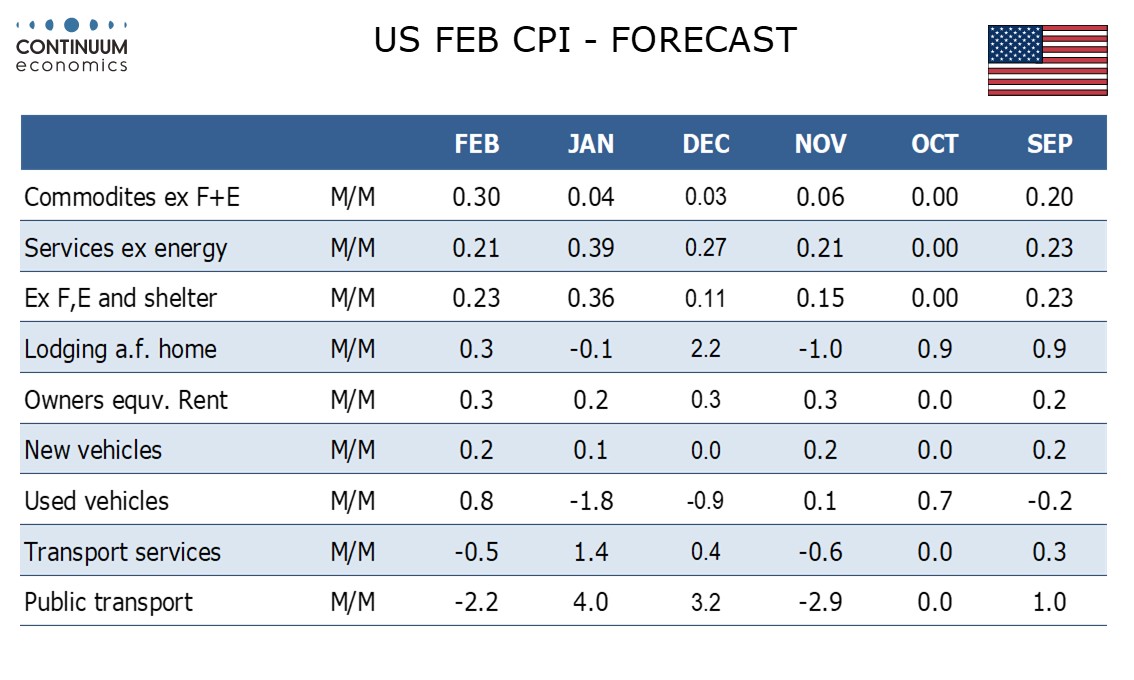

Gasoline prices fully reversed a January decline before seasonal adjustment, but after seasonal adjustment only a partial correction is likely. Gasoline prices look set for a stronger bounce in March in response to the situation in the Middle East. We expect food to remain subdued with a second straight rise of 0.2%. PPI food prices have lost momentum in recent months.

January’s core CPI increase of 0.3% was the strongest since August and with January having a tendency for volatility as new year pricing decisions are made, we would be surprised if February was quite as strong. Still, it is too early to declare inflation defeated with PCE prices having unusually exceeded the CPI in Q4 and core PPI having seen a strong gain in January. We do not expect a very soft February core CPI.

There are more components that look likely to pause or correct after strong January gains than are due for a bounce. Particularly notable are air fares which surged by 6.5% in January, while the other goods and services category saw some strong gains in January, including from tobacco and funeral expenses, which look like one-time gains. Used autos however look likely to pick up from a 1.8% January decline, and lead a 0.3% rise in commodities ex food and energy after two near flat months. Services ex energy however look set to slow to a rise of 0.2% from 0.4% in January.

We expect yr/yr growth to be unchanged from January, at 2.4% overall and 2.5% ex food and energy. We expect the ex food and energy rate to remain very close to 2.5% even before rounding, and at its slowest since March 2021, but overall CPI to edge up to 2.43% from January’s 2.39%.