UK GDP Review: More Mixed Messages Give BoE Food for Thought

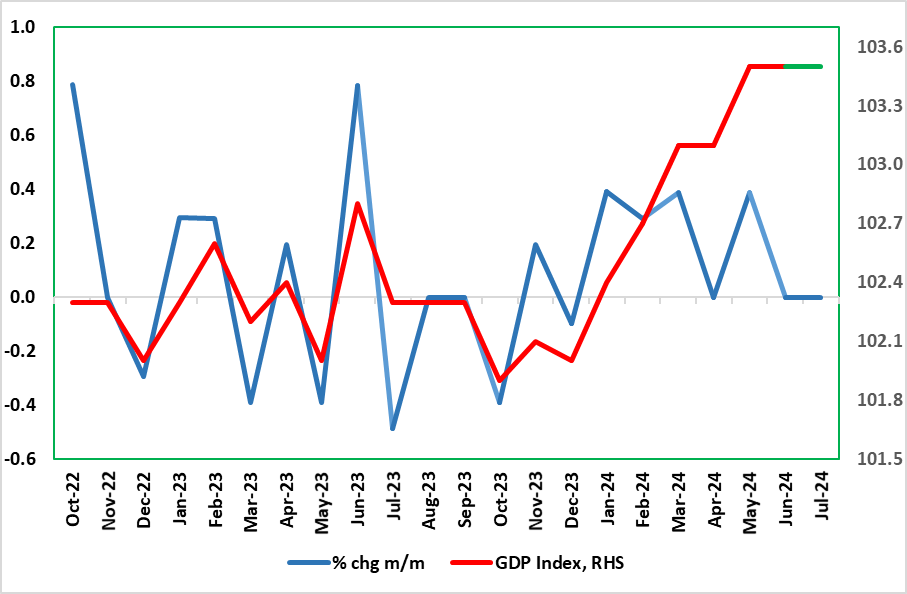

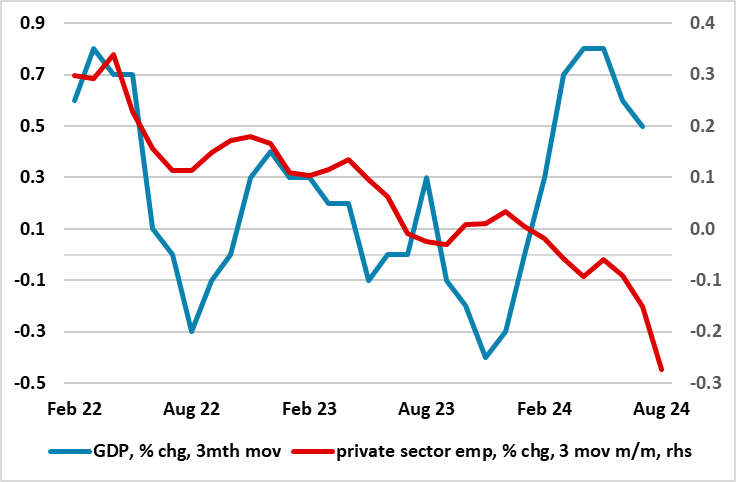

Surprising to the downside, the economy failed to show more positive signs with the July GDP data. Indeed, GDP was flat in m/m terms for the second successive month, compared to a 0.2% m/m rise widely envisaged. Thus the data still show showing volatility, as GDP growth has been positive in only one of the last four months of the last quarter (Figure 1) with the latest softness large due to a divergence between (solid) services and fresh goods output declines. Regardless, the lack of growth in Jun/Jul has created a soft base effect for Q3 growth which we see advancing just 0.1%, a quarter of the BoE estimate. This weaker immediate GDP backdrop is something that chimes more with labor market (Figure 2) and public borrowing data and where HMRC payrolls paint a much softer backdrop and possible outlook that also conflicts very much with PMI survey numbers. Indeed, it could be argued that the labor market data released earlier this week may have more impact on BoE thinking, albeit with the marked drop in average earning growth that occurred being something the MPC also expected.

Figure 1: Momentum Ebbing?

Source: ONS

After the mild recession in H2 last year, the ‘recovery’ now evident is much clearer than any expected with GDP growth notably positive but in only one of the last four months. Indeed, amid weaker retail sales, property transactions and car production data, GDP failed to grow in June and failed to do so again in July despite better weather. But this still left Q2 GDP numbers (released alongside the monthly data) showing a 0.6% q/q rise after the 0.7% gain in Q1. That Q1 ‘strength’ was partly due to a further fall in imports, but that was not be the case in the Q2 breakdown, albeit with consumer spending softening, with growth instead boosted by an import-fuelled jump in stock-building. And it does seem as if import gains may Have acted to weigh on July GDP

Regardless, the H1 GDP data is too historic to have any major impact on BoE thinking. As for Q2, on the supply side, as suggested above, the economy was boosted mainly by services with manufacturing contracting (in spite of a clear June bounce), this divergence being something very much evident across W Europe.

Regardless, these national account data have prompted BoE thinking to be much more positive and make it now suggest growth of around 1.25% for the whole year, more than double the previous estimate, albeit we think a little too optimistic, this view borne out by what we think will be Q3 GDP outcome of just 0.1%, a quarter of BoE thinking – GDP would have to rise by 0.3% in both Aug and Sep to reach the BoE projection! Our reticence reflects that this apparent resilience, if not strength, in the GDP data contrasts increasingly with employment weakness (Figure 2) and is partly a result of public sector gains. But the strength in GDP is chiming with PMI survey data and this resonates with the BoE, even though those PMI data (covering the private sector) also conflict with what (possibly more) authoritative private sector payroll suggest.

Figure 2: GDP Strength Conflicts with Payroll Weakness

Source: ONS, CE

Regardless, the economic backdrop will obviously be important for the Chancellor as she crafts her Budget due on Oct 30. Very much her aim is to lift (trend) growth, but it is unlikely that the Office for Budget Responsibility (OBR) can make any upgrade to its economic outlook purely on the basis of government aspirations. In any case, the OBR already has a very upbeat GDP outlook built into its fiscal projections, with GDP growth of around 2% in both 2025 and 2026, numbers well above current consensus thinking. The OBR may have to revise up its 2024 projection as its current estimate is slightly below the 1% we and the majority are envisaging. But the OBR too may have reservations about the growth backdrop, also noting that the more recent monthly public borrowing numbers are actually higher than it expected despite the apparent GDP strength.

Indeed, central government borrowing (perhaps a better underlying gauge) is already overshooting by £10bn just one-third of the way through the fiscal year), something that partly validates the government’s claim about a fiscal hole. Indeed, the question may be just how much there are possibly significant upside risks to the OBR borrowing projections, not least from above-inflation public sector pay rises.