UK CPI Review: Inflation Being Fuelled But Wages Still on the Wane?

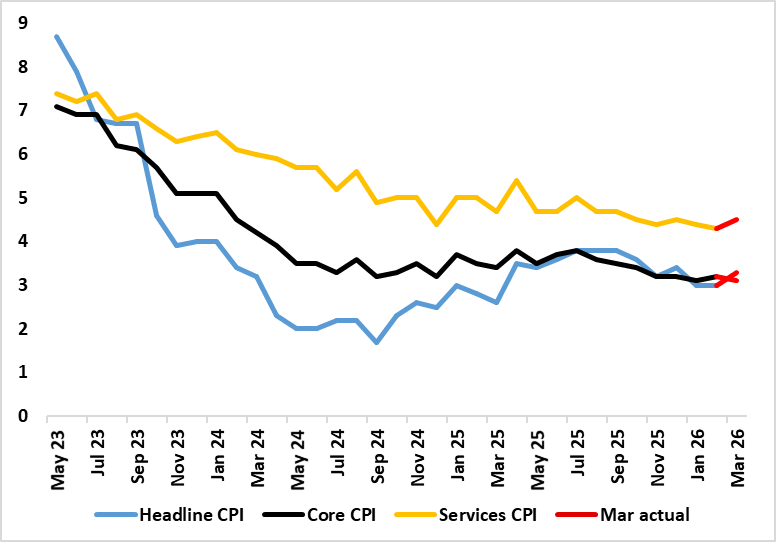

What are energy induced price rises are now very evident, most notably in PPI data as well as the more closely watched CPI figures. Thus after a stable 3.0% (a 10-mth low) February’s headline – matching the consensus, headline CPI jumped to 3.3% in March. Services, however, rose from 4.3% a four-year low (Figure 1) to .5% on the back if what may have been early Easter induced airfare rises, but the core still edged down a notch due to lower non-energy good inflation (Figure 1). The markedly and relatively greater surge in diesel relative to unleaded fuel warrants a hardly surprising upgrade to the price outlook for the rest of the year. On the basis of our baseline 4-8 week war thinking, we see the headline CPI falling back for in April before moving back higher in May in Q4 but then dropping back to end the year to 2027 at just over 2.5% but with the 2027 picture little changed, not least as tightening financial condition bite and soft wage pressures persist (Figure 2).

Figure 1: Headline Stable But Core Higher

Source: ONS, Continuum Economics, % chg y/y

This outlook is above consensus thinking (but below that of the BoE) for next few months so that we see an average headline this year of 3.0% (0.2 ppt higher than in the Outlook a month ago), with this nearly all a result of the relatively greater jump in diesel prices. Indeed, the current jump in diesel relative to unleaded is both marked and unusual and a clear contrast to the 2022 energy shock which was more gas price orientated. But we see the current 2.4% 2027 CPI headline consensus being undershot with actually a base effect induced below target period for a few months around the middle of next year.

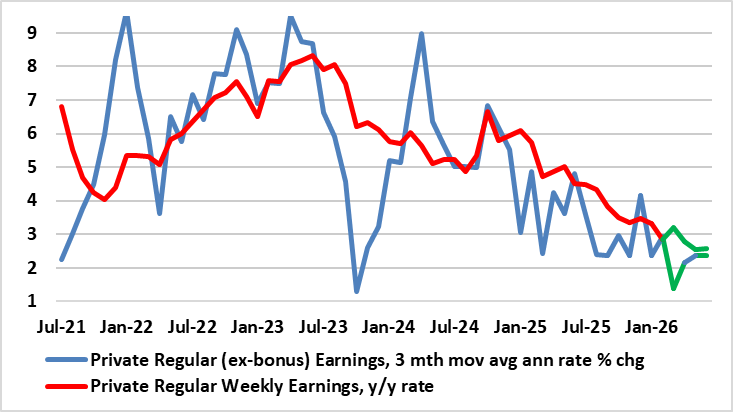

This latter view very much reflects a position where we see little second round effects, with even BoE Governor Bailey suggesting firms do not have much pricing power and we would argue that households will not have much wage bargaining power either even if their inflation expectations do rise. This comes against a backdrop where wage inflation has slowed continually and clearly

Indeed, private sector regular earnings are now running at below 3%, the lowest since pandemic related pressures softened them in mid-2020 (Figure 2). This private and regular measure of earnings is the barometer the BoE use to gauge wage pressures and is now running at a pace consistent with the 2% CPI target, this on the assumption of productivity growth of around 1%. Admittedly the data reflect pre-Iran War dynamics and may not affect what will be divided BoE thinking. But what is key is that private sector earnings are growing well below the 7%-plus pace seen before the Ukraine War started four years ago.

Moreover, there are other clearly reassuring aspects most notable in still low lower rental inflation which at just over 3% has more than halved in the last year, surely yet another sign that the housing market is in the doldrums. But while February also saw a fresh rise in non-energy goods inflation, this revered last month chiming with our view that both weak global demand and dumping of goods by China once destined for the U.S. will weigh on such price pressures

Figure 2: Weaker Wage Pressures Increasingly Evident?

Source: ONS, CE