SNB Preview (Dec 11). Still Staying at Zero – And For Some Time?

Along with just about everyone, we see unchanged SNB policy when it gives it next quarterly assessment on Dec 11. It is likely to retain what were modest growth outlook for this and next year and still see inflation nearer zero than the 2% upper target (figure 1). But this will be enough to justify stable policy. However, explicit will be a retained not so much an easing bias but an acknowledgement that the policy rate could go negative again, but with a high bar to make this occur. Indeed, financial stability issues may feature more in the Board’s discussions as the summary of this month’s discussion (Jan 8) may highlight (Figure 2). Regardless, we point to stable policy out through 2026 at least, with only a slight possibility of a return to sub-zero rates.

Figure 1: SNB Inflation Outlook Likely to be Unchanged

Source: SNB

Very much as expected, both in deed and word, the SNB kept the policy rate at zero in September having cut by 25 bp back in June in June. Indeed, ahead of the September decisions, markets priced out what was previously seen as a good chance of rates turning negative, even against a backdrop of the punitive tariff scheme the Swiss economy was then seemingly facing. Notably, that U.S. threat of 39% tariffs have been pared back to the 15% most other countries, this may also apply to yet to be confirmed pharmaceuticals which account for 40% of exports. Admittedly, probably related to tariff uncertainty, Swiss GDP contracted by a surprise 0.5% q/q in Q3. But this makes it only more likely that the SNB will continue to see 2025 GDP growth at the lower end of the 1%-1.5% range it offered three and six months ago – albeit where overall and certainly sports adjusted GDP growth next year may be below 1% and thus some 0.5 ppt below potential. However, this unchanged growth outlook makes it likely that the inflation outlook will not be altered materially, even with recent undershoots of expectation and which show clearer signs of domestic price pressures receding.

The strong Franc, more recently against the USD, is also unlikely to have any policy impact. While still pointing to possible FX intervention and a continued willingness to adjust policy accordingly, the updated statement will (probably deliberately) be vague about both taking rates below zero and what the consequences would be. But any overt attempt to weaken the current via intervention or lower rates may be shunned for fear it would court U.S criticism and possibly fresh retaliation.

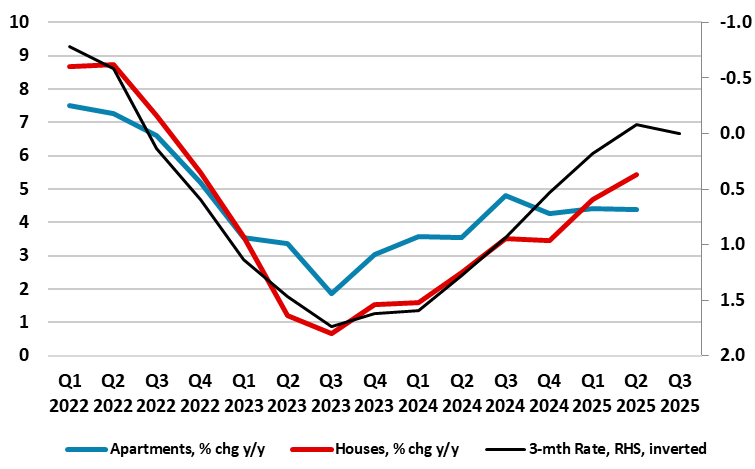

Figure 2: Property Price Recovery Linked to SNB Easing?

Source: SNB

As for the high bar for any return to negative borrowing costs the SNB has been clear this is because of the adverse impact on savers and pension funds. Indeed, SNB President Schlegel stressed in a recent interview adverse impact of negative rates on the likes of savers and pension funds, going on to warn that doing so may need stronger countermeasures later on, this possibly a result of the fresh pick-up in property prices now emerging. The latter is all the more notable given the continue pick-up in real estate prices, this very much correlated with SNB policy (Figure 2).

But the irony is that while mortgage lending and house prices have started to rise afresh, banks seem reluctant to lend overall with private sector credit actually hardly growing. However, the updated inflation forecast from the quarterly assessment confirms continued but not greater disinflationary price pressures. Moreover, the SNB target being a less explicit sub-2% offers policy makers more flexibility. Though the medium-term forecasts are likely to be hardly changed but where the SNB statement again likely to note that these are consistent with price stability!