Sweden Riksbank Preview (Dec 19): Flagging a Little Further Easing?

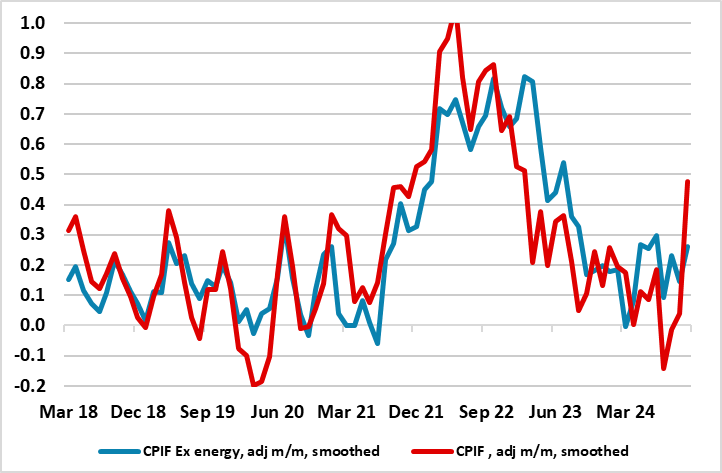

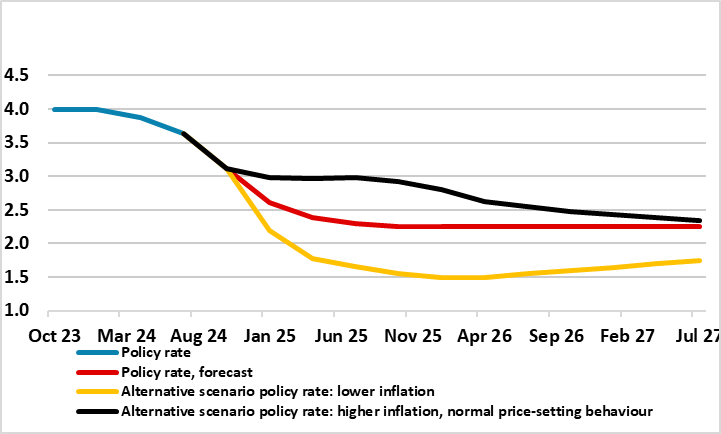

A fifth successive rate cut is seen at this looming December Riksbank meeting, but rather back to a 25 bp move rather than the 50 bp cut last time around (to 2.75% vs the 4.0% peak seen up until last May). This would fulfil the policy guidance advertised at the September Board meeting. But it will be the updated projections that will be the main news, not least given data of late that has been on the high side of expectations, including a small recovery in GDP and CPIF data well above Riksbank thinking (Figure 1). Regardless, this is unlikely to alter policy thinking where inflation worries have subsided to be replaced by clearer worries about the real economy. And in regard to the latter, the Riksbank may revise down its slightly above-consensus GDP outlook out to 2027, the question being whether a lower terminal policy rate will be considered, or merely getting there a little faster. But amid downside growth risks and realties through Europe, we now still see the policy rate troughing at 2.0% by mid-2025, now 25 bp below our previous thinking and Also the same amount below the Riksbank’s terminal rate but one we seeing being arrived at two quarters earlier. But deeper cuts are possible as even the Riksbank acknowledges (Figure 2).

Figure 1: Short-Term Inflation Dynamics Less Favorable?

Source: Riksbank, CE

Admittedly, the inflation surprises have been concentrated inn energy and result of the EU’s new electricity directive which has caused a sharp increase in electricity prices in Sweden since its introduction in late October. But even inflation ex energy has started to flatten out although the CPI measures on the basis is still consistent with target having already been met. Even so, the prices outlook inflation certainly for the next year has become a little more uncertain

But in terms of what has happened, it is clear that while lower inflation has provided the scope to ease policy in this speedier manner, the rationale is increasingly that from a weak economy. Last time around the Board statement was clear that ‘there are still few clear signs of a recovery. To further support economic activity, the policy rate needs to be cut somewhat faster than was assessed in September. It is important in itself that economic activity strengthens, but it is also a necessary condition for inflation to stabilize close to the target’.

Policy Front-Loading?

Since the spring, it has been very much a question of how fast, not if, as far as policy easing was concerned for the Riksbank, with policy thinking having been markedly reshaped this year. From the Board’s perspective, by initiating easing relatively early in May, it was both reacting to weak data (both real and price wise), but more notably in giving itself flexibility to pursue what it then thought needed to be a gradualist approach to further easing. That now has changed and increasingly radically with policy put into a faster gear to front-load, both a result of an undershoot of inflation (partly energy related but ever clearer in terms of short-run dynamics) but as suggested above increasingly due to a still weak economy which has failed to grow on balance since end-2021, albeit with clear quarter-to-quarter volatility.

Figure 2: Alternative Official Policy Outlooks

Source: Riksbank

Terminal Rate Scenarios

The question is, if growth disappoints into 2025, will the Riksbank ease further than it is now flagging. This is entirely possible and is now a view we encompass to some degree – indeed, the Riksbank scenario analysis suggests that the policy rate could drop below 2%, at least temporarily (Figure 2). Supposedly, this would have to be a result of the weaker growth backdrop accentuating disinflation, this all the more likely given that we see the Riksbank’s’ 2024 GDP picture of 0.8% possibly twice too high and where we think is an optimistic 1.9% 2025, turning out nearer 1%.

But other factors may come into play, not least policy moves elsewhere which may result in a greater and unwanted appreciation of the currency than currently envisaged by the Riksbank. A further factor may be he Riksbank’s view of neutral rates. Recent analysis from Deputy Governor Seim suggested that the long-term neutral interest rate, and thus the long-term normal policy rate, is probably between 1.5% and 3%, ie a full one percentage point lower than the range the Riksbank published in 2017. Indeed, it was argued that one cannot rule out the possibility that the policy rate may periodically need to be lowered to levels around zero and that a policy rate cut in the order of 1.5 to 3 percentage points is not particularly exceptional