U.S. Tariffs - the EZ/EU Response?

The U.S is imposing a widespread tariff on the EU of 20%, higher and broader than expected, this based on U.S. calculation of an effective tariff rate of in effect 39 per cent, a figure the EU puts at about 1 per cent. Moreover, rather than including factors such as VAT, and hygiene restrictions on imports, the US tariff estimate seems more indicative of trade in goods imbalances than genuine estimates of barriers to trade, if so, this may be a means through which negotiation can take place and possible with some success. Regardless economic damage is likely to be sizeable, and as far as the EZ is concerned but clear downside to out already anaemic sub-1% GDP estimate for this year, albeit the extent complicated by both how and when the EU will retaliate and global trade diversions, possibly leading to export dumping into the EZ. One worry is that the EU may spread the breath of tariffs via steeper tariffs on digital services, even though the UK has suggested doing the opposite, all threatening a far from concerted response to the U.S. at least from Europe.

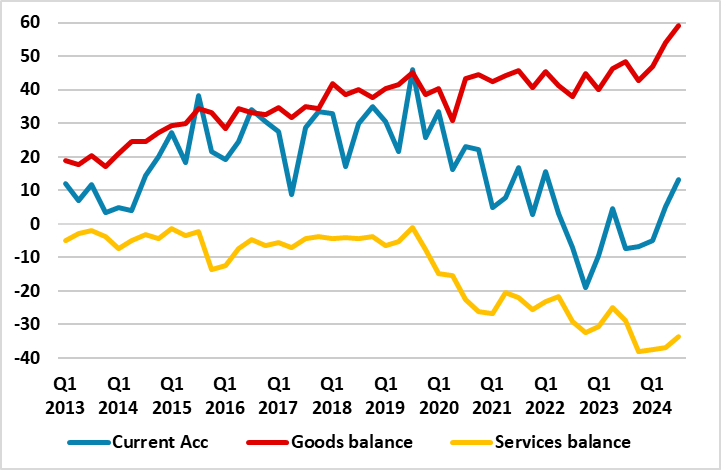

Figure 1: Bilateral Current Account Gap with U.S. Barely Visible

Source: ECB, EUR Billion in trade between EZ and U.S.

What can Possible Negotiations Dwell On?

In regard to negotiations, the EU has given itself a four-week pause before any retaliation is decided, albeit possible outlining what it is considering beforehand as it hopes to negotiate a solution and/or where the US president could do U-turn before then, as he has before. But a foretaste is already in the offing as the EU is now ready to impose duties on up to EUR 26bn of US goods in response to steel and aluminium tariffs but also has yet to identify how it will retaliate against 25 per cent tariffs on car exports announced last week.

A further topic of negotiation will be services. As has been suggested widely, the EZ (and EU) does not actually have a trade gap of any serious proportion with the U.S. certainly once services are taken in to account. Indeed, the bilateral current account was in deficit with the U.S for a period recently (Figure 1). Admittedly, that has now turned into a surplus as the EU goods trade balance improved. But the point we would underline is that this is unlikely to be repaired or even addressed by tariffs as this goods trade reflects weakness in EZ real domestic demand (which tariffs may only extend if not accentuate) which has reined in imports and it is the weakness in the latter which is responsible for the rising trade surplus in goods in recent year.

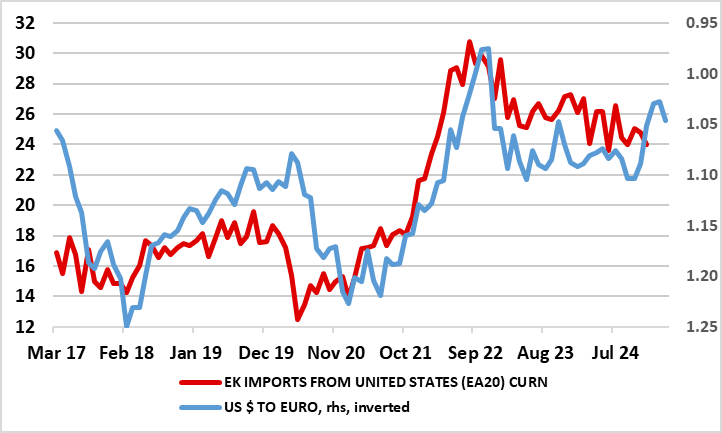

But less well known is that this fresh nominal rise in the bilateral gap as opposed to real goods surplus improvement (which is one underlying issue perturbing Trump) has as much actually been driven by price shifts in the last few years not volumes, this including the appreciation of the USD (Figure 2), and the fall in energy prices both oil and gas. Indeed, the fact that the bilateral trade in goods gap with the US has started to rise is very much due to a fall back in EZ imports from the U.S. rather than increased EZ exports to the latter (Figure 3). As importantly, much if this is being driven by shifts in prices. This includes the EUR/USD exchange rate. During the immediate recovery from the pandemic, the appreciation oi n the USD helped boost the cost to the EZ of purchases from the U.S. But more recently, the fall back in the USD has done the reverse, helping curb the nominal value of EZ imports (Figure 4).

Figure 2: Less Strong Dollar Reducing EZ Import Bill

Source; Eurostat

This has come in spite of what have been marked rise in the volumes of certain EZ imports from the U.S. most notably oil and gas which are first and third in terms of goods most imported by the EZ /EU from the U.S. Most notable in this has been the surge in LNG imports from the U.S. In 2023, the EU imported over 120 billion cubic meters of LNG with the U.S. now being the largest LNG supplier to the EU, representing almost 50% of total LNG imports, this having tripled since 2021 as the EU shifted away from unstable Russian supplies. Similar concerns also mean that the U.S. became the EU's largest oil supplier after Russia's invasion of Ukraine in February 2022 disrupted Europe's energy supplies. But the 15.1% of the EU's petroleum oil imports that came from the US in Q3 last year was down some two ppt on the previous year as lower oil prices reduced the bill (Figure 5. This is even more notable for LNG where the marked drop in price reduced the import bill by around half in 2023 to EUR 30 bln.

Admittedly, the EZ’s imports from the US may rise further this year as a result of increased purchases of gas (not least to restock depleted inventories) and increased military spending, both also attempts to pacify Trump. A faster recovery may also help if fiscal promise bear fruit. But the irony is that two of Trump’s economic aims (lower oil prices and weaker USD) may serve only to widen the goods gap with the US

What’s in Store

The 20% tariff imposition will be fairly significant even though EZ exports of goods to the US were only 3% of its GDP in 2023, especially given what may be termed as second round effects as other countries attempt to shift their exports from the U.S. to Europe, and already-frail EZ business confidence is hit by the added and extended uncertainties. As for the impact, this is obviously hard to judge but work has been done to model some likely effects such as that recently by the London School of Economics. This very concludes that a 10% tariff would hit GDP in the European Union by modest reduction of 0.1% - hence the actual tariffs could be over 0.2%, albeit the full outcome probably worse given the impact of business and consumer uncertainty, trade diversion and retaliation. Within Europe, the impacts would vary significantly: Germany could see a 0.4% drop in GDP, while in Italy the decrease could be negligible and hardly much worse for France. But importantly, the research suggests that retaliatory measures by China and/or the EU would likely worsen economic outcomes for all parties involved, potentially sparking a damaging trade war, this risk even clearer if the EU’s ultimate retaliation stretched out a possible digital services tax.

ECB Response

But while we still point to an anaemic EZ growth rate of less than 1% this year, the high likelihood is this is now too high even though this did encompass at least half of what the U.S has unveiled tariff wise. But the imponderables include the likely trade retaliation by the EU and how and when the alleged EU fiscal expansion will come to pass. It will be interesting n to see how and when the ECB reacts, with a clear factor in its thinking being a likely interpretation that the tariffs will be net disinflationary, not least will trade diversion possibly causing export dumping into the EZ. A further factor will be how banks may react to the added uncertainty. The ECB is now admitting its QT program maybe making banks less willing/able to lend and now with increased real activity uncertainty the ECB will be looking at its Bank Lending Survey due two days before the April 17 Council meeting. It is now more likely than not that the ECB will cut at that juncture even given the uncertainties (eg EU retaliation) that will not have then been resolved by then.