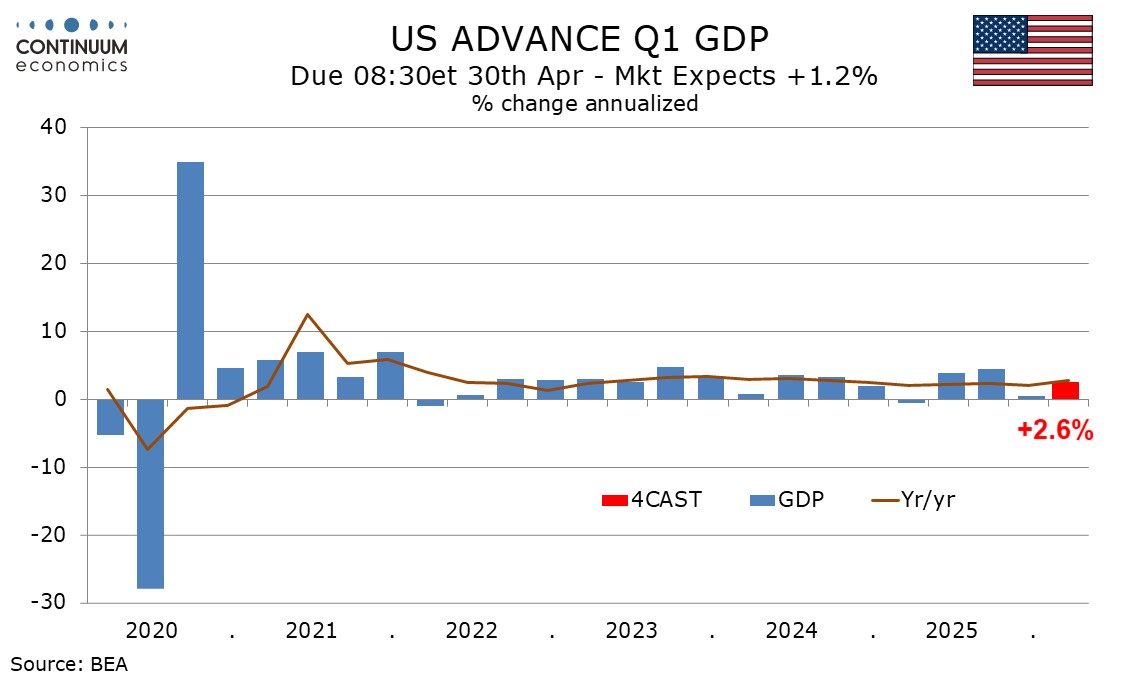

Preview: Due April 30 - U.S. Q1 GDP - Government to lead bounce from weak Q4, Core PCE prices stronger

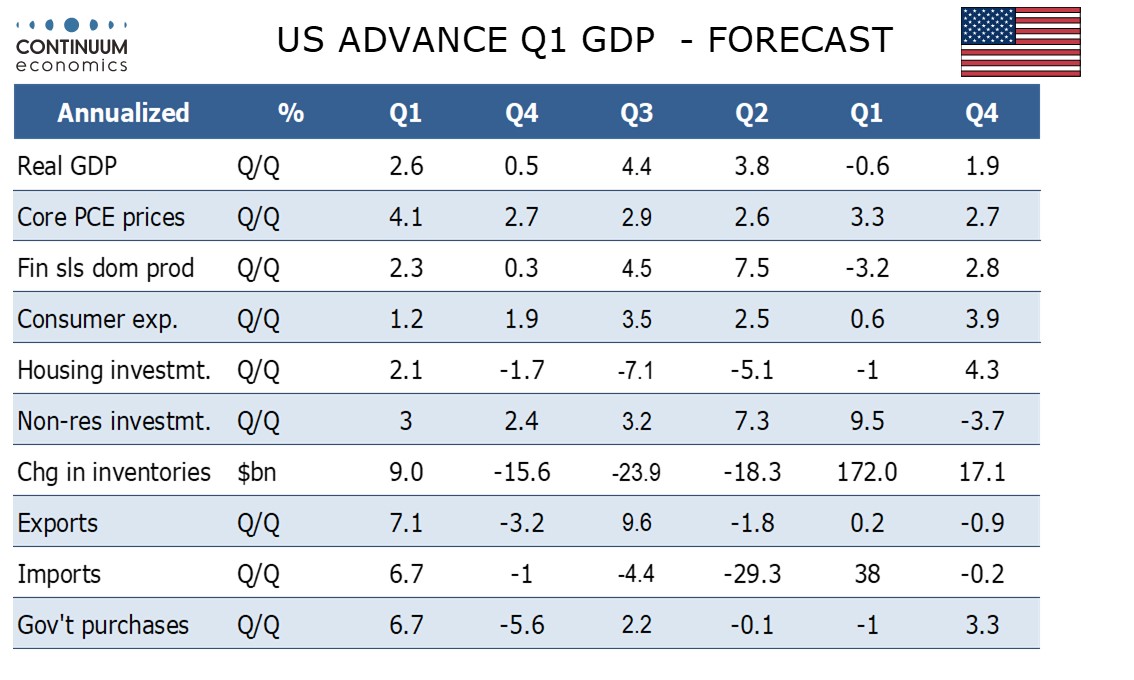

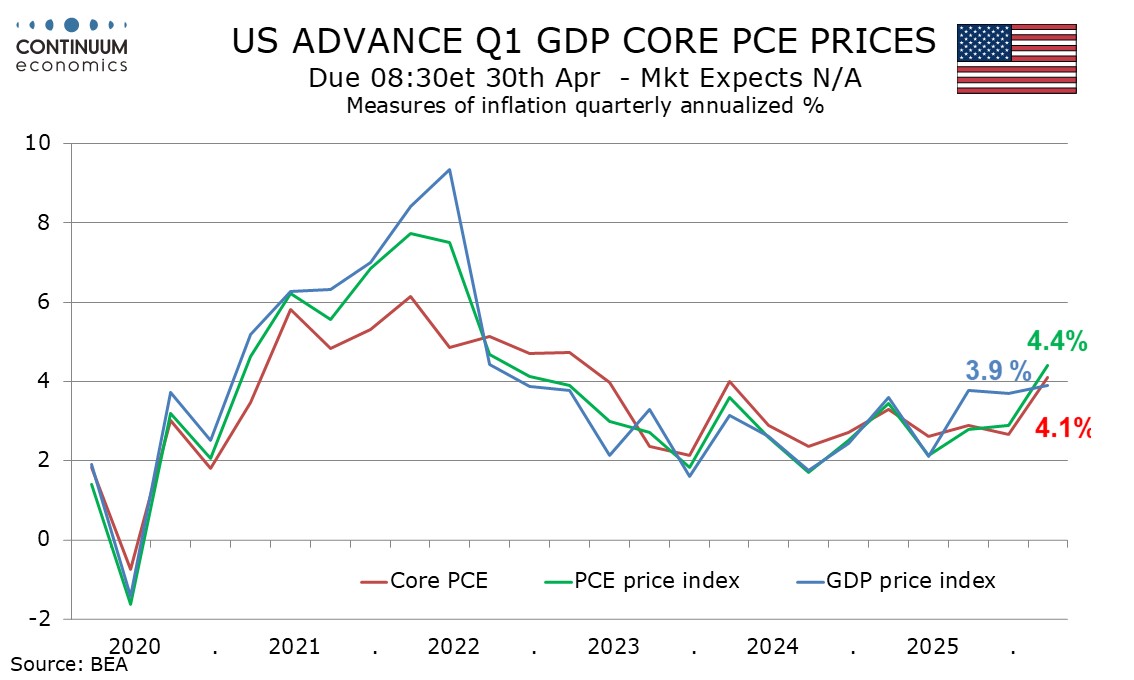

We expect a 2.6% annualized increase in Q1 GDP, improved from a weak 0.5% in Q4 largely due to a rebound in government from Q4 data that was depressed by a shutdown. Excluding government we expect a second straight quarter close to 1.5%. We expect a significant acceleration in core PCE prices, to 4.1%, the highest since Q1 2023, from 2.7% in Q4.

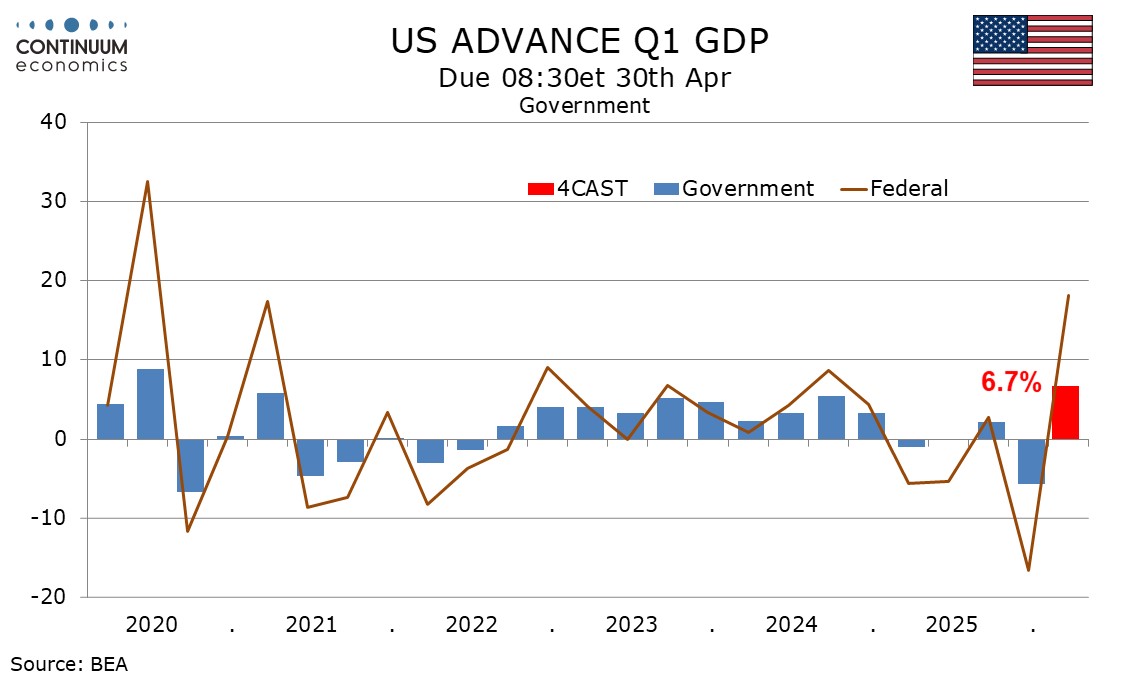

We expect government to rise by 6.7%, more than fully reversing a shutdown-induced 5.6% decline in Q4. However we expect slower growth from state and local government and within the Federal detail so not expect a full reversal in non-defense Federal spending. Government did return to growth in Q3 after DOGE-related declines in Q1 and Q2, and we expect moderate growth going forward.

We expect final sales to domestic buyers (GDP less inventories and net exports) to increase by 2.4% after a 0.6% increase in Q1. We expect business investment to remain firm at 3.0% with strength in equipment and intellectual property outweighing weakness in structures. We expect a 2.1% increase in housing, the first rise in five quarters, supported by the resumption of Fed easing in late 2025.

Consumer spending is likely to lose momentum, rising by a 4-quarter low of 1.2% due to a dip in retail, even with March data having exceeded expectations. We expect services to increase by 2.4% even with a subdued March assumed (March’s personal income and spending report will be released alongside GDP). Despite the slowing, we expect consumer spending to exceed real disposable income for a fourth straight quarter, with the latter rising by only 0.8% in Q1.

Prices are restraining real disposable income, with our forecast of a 4.1% annualized rise in core PCE prices assuming a 0.3% increase in March. We assume a 0.7% increase in overall March PCE prices, though the Q1 rise in overall PCE prices at 4.4% will not be sharply above the core. We expect the overall GDP price index at 3.9%, similar to the preceding two quarters, with a slowing in government from Q4 data that may have been inflated by the shutdown weighing against the acceleration in PCE prices.

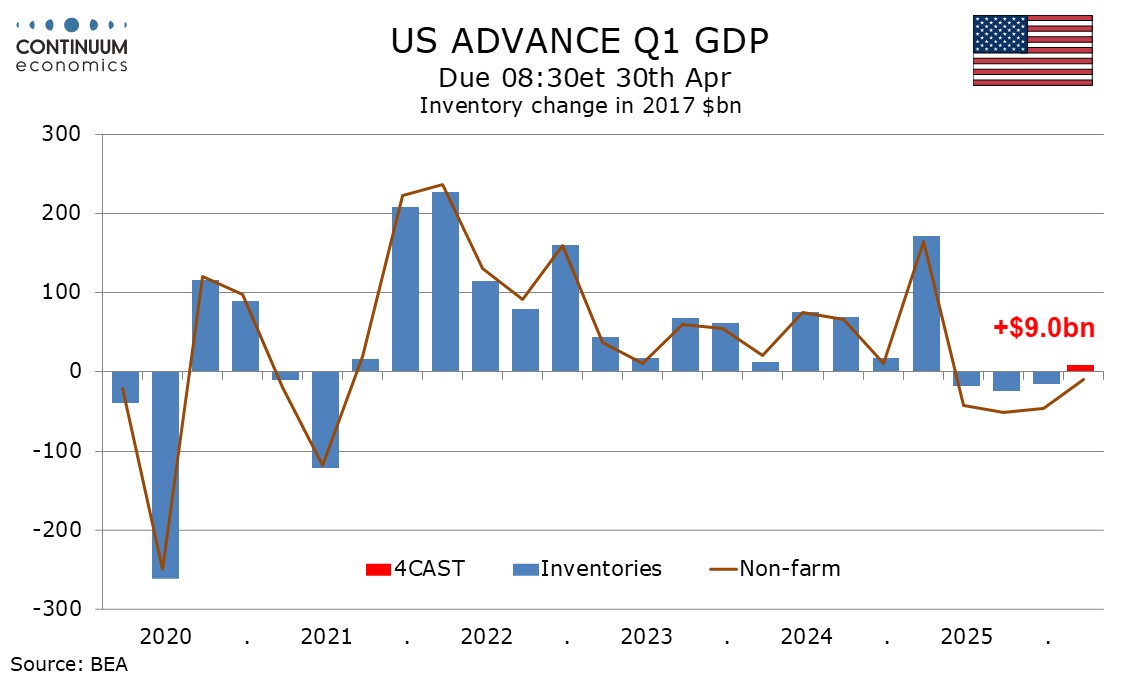

We expect inventories to return to growth after three straight declines that corrected a pre-tariff surge seen in Q1 of 2025. However the impact on GDP is likely to be modest, adding only 0.3%. We expect final sales (GDP less inventories) to rise by 2.3%.

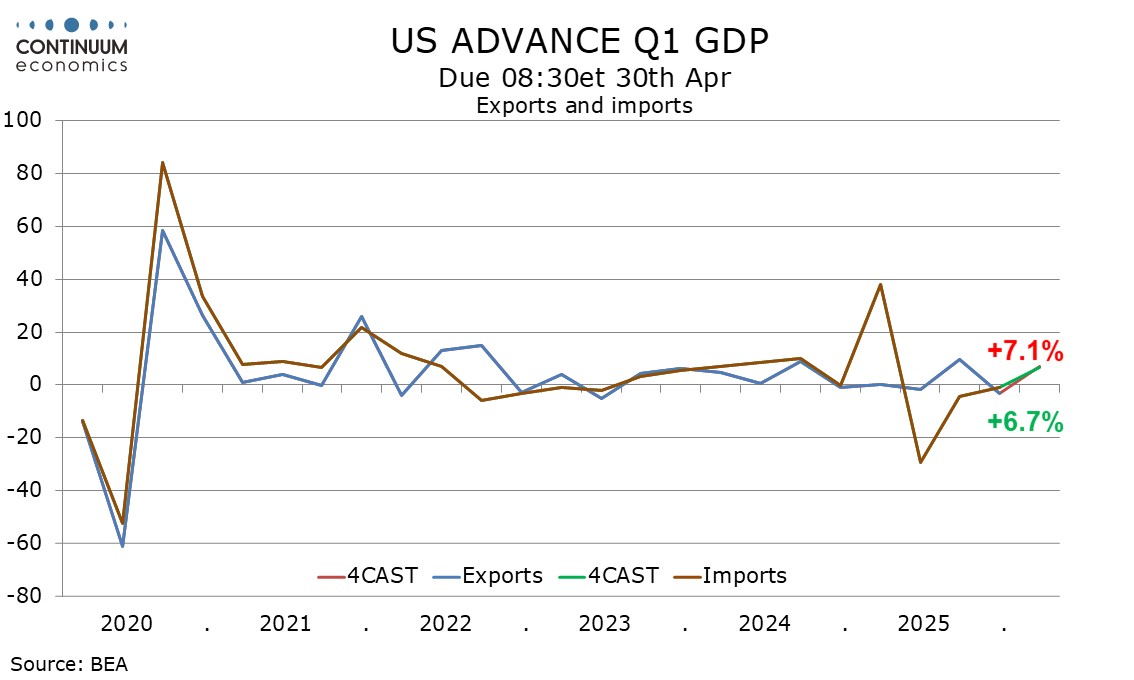

This means a negative contribution of 0.1% from net exports, with exports and imports both set to see respectable gains in Q1, we expect by 7.1% and 6.7% respectively. Imports would see a slightly stronger rise in USD terms. Advance March goods trade data, as well as data for durable goods, retail and wholesale inventories, will be released the day before GDP on April 29 and could have some impact on the GDP picture.