UK Consumers: Rent the Growing Hit to Spending Power

The UK has faced a series of cost-of-living shocks in the last few years. Some such as the surge in food prices may even be reversing, while it now looks likely the BoE hiking cycle may also start to reverse, although rising market rates may mean little further fall in effective mortgage rates in coming months. Even so, the BoE is its upcoming n Monetary Policy Report is likely to suggest that an even greater proportion of the interest rate hikes may have come through already than the two-thirds estimate it offered in February, albeit with the full impact only to come well in to 2025 (Figure 1). We estimate that this will damage the spending power of household s with mortgage some 10% cumulatively by end 2025 and then start to reverse as lower interties rates filter through. But a further and also sizeable –and possibly more prolonged – hit to spending power is now hitting those renting as rent inflation has risen to a 30-year high of over 7% (Figure 2). This has already hit spending power for such renting households by some 5%, albeit with the proviso that the full impact may be relatively greater given that households that rent (at some 37%) are a larger segment of the economy than mortgagees (30%).

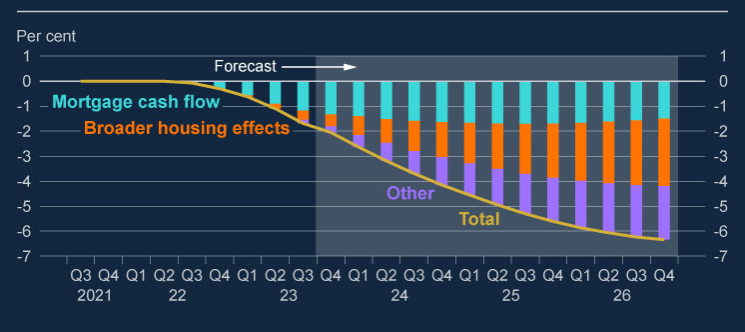

Figure 1: Increases in interest rates are expected to continue to reduce Household consumption

Source: BoE Nov MPR

BoE Rate Hikes – the Direct impact on Households

It is possible to dissect the impact of the hikes in BoE interest rates since August 2021 on the level of household consumption, both do date and into the future. According to BoE estimates, the total effect is split into broad categories that show the relative size of some of the channels of monetary policy transmission (Figure 1). The mortgage cash-flow channel captures the direct impact of changes in household mortgage costs. The broader housing channel represents the impact of changes in the value of housing. This includes, among other effects, changes in the available collateral against which households can borrow and effects on households’ saving behavior. Other channels are captured in the purple bars. This includes a range of mechanisms such as the impact of interest rates on financial wealth, and ‘second-round’ effects in which a reduction in demand then leads to households cutting consumption as the wider economy weakens.

Overall, the estimates suggest that full impact of higher interest rates will not be felt until well into 2025, but the pertinent question is how much of the impact has already occurred. BoE estimates that may be updated in the upcoming May Monetary Policy Report (MPR) on May 9 are likely to suggest this may now be over two-thirds, albeit with the proviso that this is uncertain as it is not possible to gauge to what degree some of 80%-plus of those with mortgages on fixed rates may have altered their spending behavior well before facing an actual rise in their debt servicing bills – surveys suggest this maybe over 30%. But more likely than not the BoE may upgrade this estimate, partly on the basis of the recent rise in re-mortgaging.

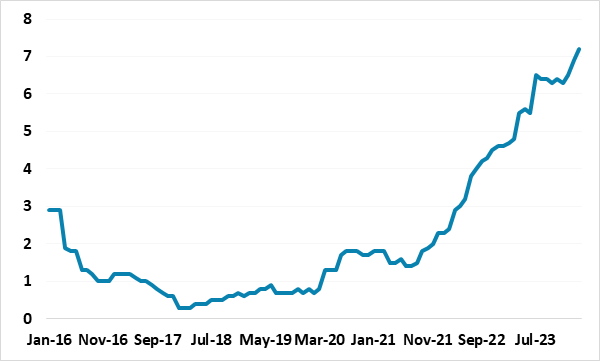

Figure 2: Surging Rental Costs

Source: ONS, annual UK rental inflation

The (Forgotten) Rental Channel…

We estimate that with an average outstanding UK household mortgage of £ 200K, and where a 1 ppt rise in mortgage costs adds some £ 600 to the yearly debt servicing bill, households with mortgages may have seen their effective spending power, ie disposable income post mortgage payments fall by some 10% since the trough in mortgage rates in Sep 2021. The impact would have been greeter some months ago given how much higher mortgage rates were then – we are using an average rise of just over 4 ppt. But of course, the impact will be limited, unless the BoE is forced to hike even further, something we regard to be highly unlikely.

…Supply…

But there is a further channel to the ones spelled out above in terms of how BoE rate hikes may and have hit the consumer and this is via rents. Rent inflation reached a 30-year high of 7.2% last month and is even higher at almost 10% in the private sector (well over half the rental sector). This reflects a series of factors, one of which is very much an indirect consequence of BoE policy, namely that landlords, many of whom do not own their rental properties, have had to face higher mortgage rates and are keen/forced to pass these on in the form of higher rents. This has been made more onerous given regent legislation (Finance No. 2, Act 2015, (Section 24), which has meant landlords can no longer deduct mortgage repayments from their taxable income. There are possible ways around such this such as creating a company to hold investment property – also called incorporating – but this throws up an increased chance of paying capital gains tax. Overall, it has been suggested that as a consequence of these factors, 10% of rental properties have been taken off the market in the last year.

…And Demand

But there are demand factors too, not least that the modest fall in property prices, alongside rising mortgage costs, has made housing purchase all the more elusive, especially given the impact that inflation has had on the cost of living. In addition, the shortages of properties has been accentuated by rigidities in the housing market related to relative house price moves rather than sustained demand increases and is also evident in ever weaker housing market transactions.

In terms of the net impact, rents have risen some 14% since the trough in mortgage rates of Sep 21, enough to have erased spending power for such households by some 5%. This is obviously less than the 10% hit for those households with mortgages, but the telling factors here are twofold. Firstly, those that rent account for 37% of households, some seven ppt more than for those with mortgages. Secondly, given the more structural nature of the emerging rise in rent inflation, we see it persisting, meaning not just sustained damage to household spending but increasing such damage! This just another reason why we continue see below somewhat below consensus activity ahead, but with downside risks.