EZ HICP Preview (Apr 3): Core Disinflation Signs Start to Flatten Out?

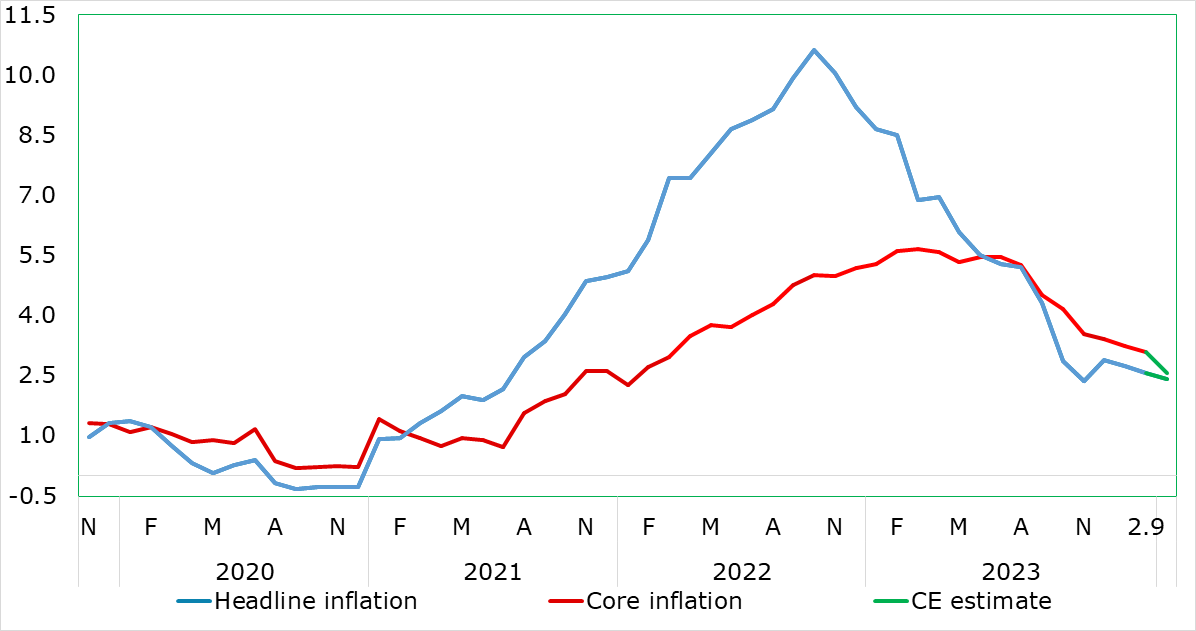

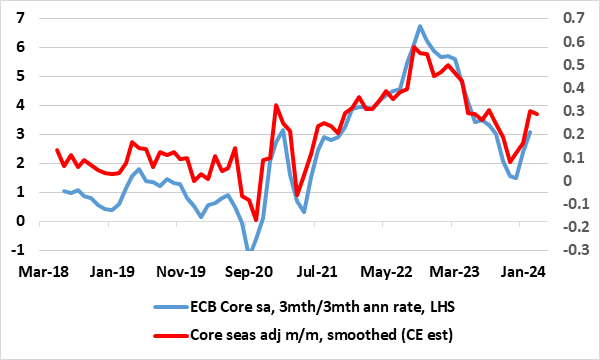

Enough to have affected ECB thinking, there has been repeated positive EZ news in the form of plunging inflation. This continued in the February numbers, albeit with the 0.2 ppt drops in both headline and core being less that most anticipated. Regardless, the headline, at 2.6%, continued its recent decline while the latest core is still on course (Figure 1) to meet the ECB Q1 projection of 3.0%. This is on the basis of our March HICP projections; we see the headline down to a 31-month low of 2.4%, the latter encompassing more discernibly softer y/y services inflation, in turn pointing to the core rate dropping a notch to 3.1%. This is notable as the ECB has been somewhat troubled by the failure of services inflation to have fallen in the last few months, and the fact that it slowed just a notch to 3.9% y/y In February may harden some of the hawks worries about aspects of price resilient not least as monthly adjusted numbers (Figure 2) have also shown some fresh resilience, if not revival, notably on a core basis.

Figure 1: Headline and Core Inflation Falling Further?

Source: Eurostat, CE

On-Target Inflation Looming in H2 As Resilient Services Succumbs Modestly!

February saw services fall albeit only modestly in y/y terms, this taking the core down in turn. The upside risks from fuel prices and from rents/eating out may also have been behind the slightly firmer than expected numbers. Regardless, possibly encompassing added volatility from the early Easter this year, we still envisage that the headline now hit target us in summer 2024, well over a year earlier than the ECB envisages, and then undershoot through 2025, while the core should continue to fall in the interim regardless.

As for March details, we see a further and broader to a 31-month low of 2.4% in the headline HICP data, dominated by a clear fall in food inflation, and a belated drop in services, both possibly held up somewhat by the earlier Easter this year – if so, there may be softer numbers in the subsequent 2-3 months. Energy will act as a boost to the headline, however, this very much evident in already-released Spanish HICP numbers.

But Disinflation is Not All Plain Sailing

There are ever-clearer signs of soft underlying inflation at least in terms of non-energy goods and also in terms of persistent price pressures which are now running around the 2% target on an overall basis and even more so for core measures. However, there are signs that such underlying measures have stopped falling (Figure 2), not least on the ECB’s preferred short-term inflation indicator. Moreover, services inflation has hardly fallen in y/y terms, a stability seen in seasonally adjusted m/m numbers, the question is whether this is true price persistence linked to high wages or reflection of one-off factors such as indirect tax moves. At this juncture, this is something we think this is more noise than fresh trend but will continue to monitor closely.

Figure 2: Adjusted m/m Price Pressures Stable Around Target But No Longer Falling

Source: ECB, CE