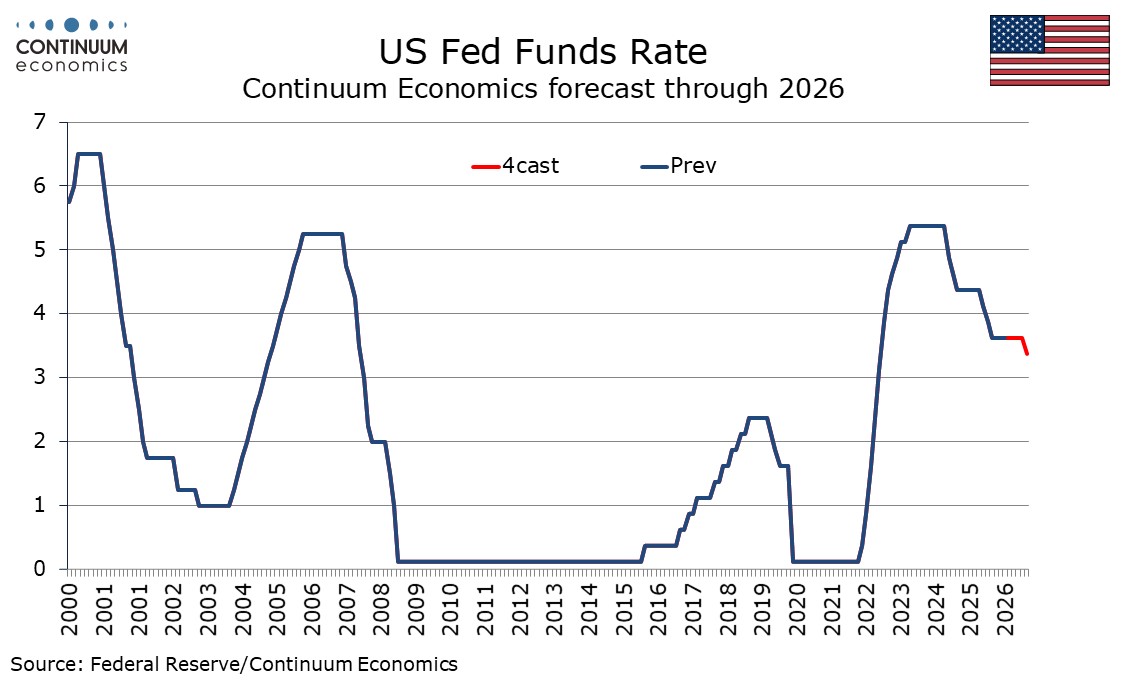

FOMC - Easing call moved to December from September

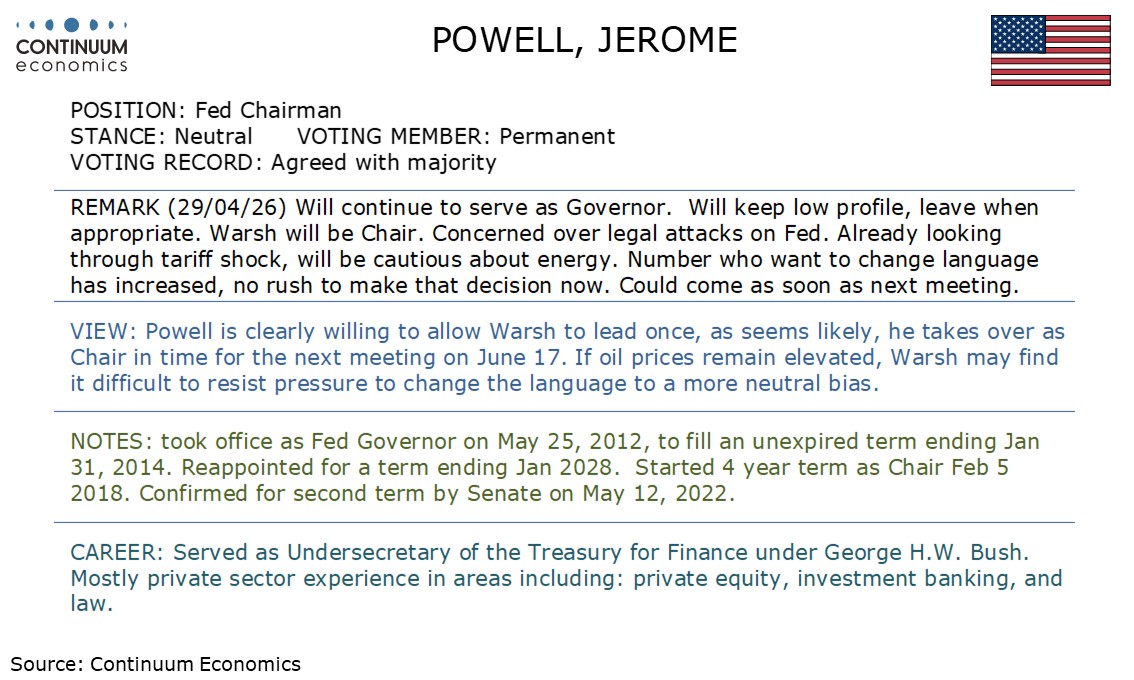

The Fed is now entering a transition from Chairman Powell to Chairman Warsh, who looks set to be in place at the next meeting on June 17. The final meeting of Powell’s term saw three hawkish dissents on the language and Powell announce he will continue as Governor after his term as Chair ends. We no longer expect a 25bps easing in September, though continue to expect a 25bps easing in December.

Rates were left unchanged at 3.5%-3.75% at the latest meeting but a total of four dissenting votes was the highest since 1992. One was dovish, Miran continuing to call for a 25bps easing, though Miran will exit once Warsh enters. The three hawkish dissents came from district presidents, Cleveland’s Hammack, Minneapolis’ Kashkari and Dallas’ Logan. They were in agreement with the decision to leave rates unchanged but objected to the inclusion of an easing bias, preferring language suggesting that the Fed could move in either direction. This argument has been visible in recent minutes. Three of the four rotating regional voters made hawkish dissents, the exception being Philly Fed’s Paulson. None of the permanent voters dissented though it is possible some were leaning in that direction but decided not to cast a dissenting vote. Several non-voting district Presidents are likely to agree with the hawks. Powell saw no rush to change the language but saw the possibility of this being done at a future meeting, even as soon as the next one in June. That meeting will see participants updating the dots.

Powell’s decision to continue as Governor is due to concerns over the legal attacks on the Fed. The action against him has been dropped by the Justice Department but the issue has not been conclusively closed to his satisfaction. Powell stated he would take a low profile as Governor and leave when appropriate, suggesting he will not act as a shadow Chair leading opposition to any changes Warsh may try to push. However, Powell’s continued presence means Trump will not have another seat to fill. Should Democrats take control of the Senate in November’s elections, Trump’s ability to appoint a like-minded individual to the Fed once any vacancy emerges would be diminished.

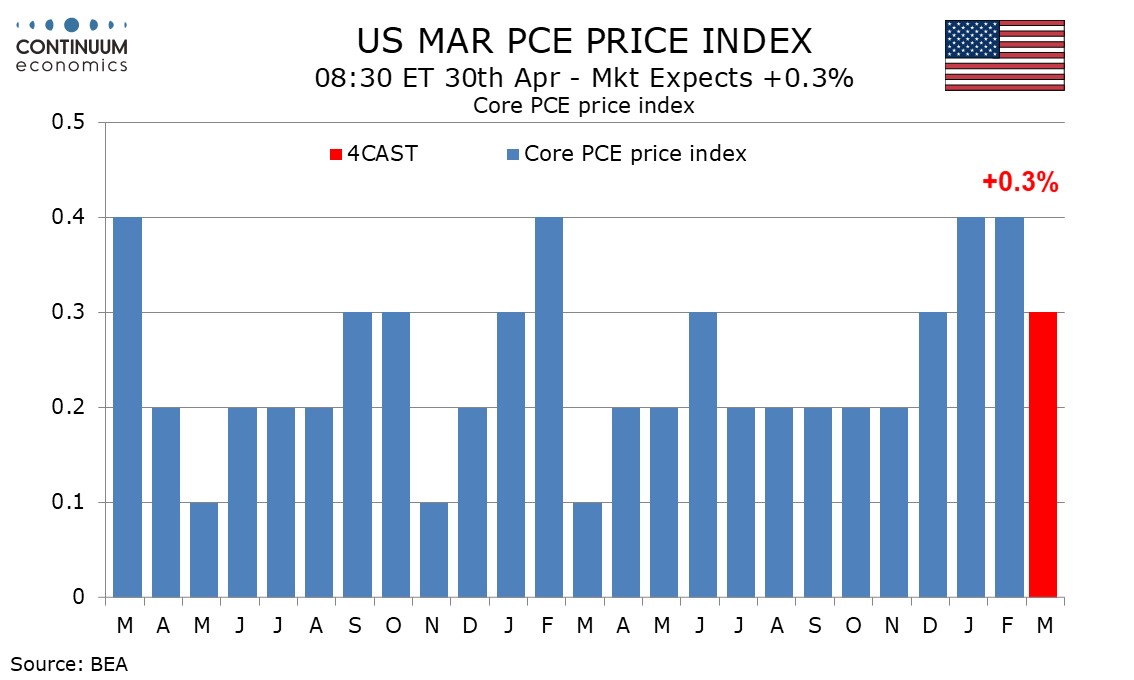

Forecasting the Fed is particularly uncertain at the moment given the uncertainty over how Warsh will approach the job as well as the obvious uncertainty over the Middle East. Warsh looks set to have a dovish lean, and the permanent voters at the FOMC will be cautious about publicly dissenting from the Chair. However, to be able to justify an ease we are going to need confidence that the Strait of Hormuz is open on a sustained basis, and we will need moderate data from core inflation, something that has nit been seen in recent data from core PCE prices. Powell stated he expects March data to show a 3.2% yr/yr increase in core PCE prices with overall PCE prices at 3.5%, consistent with consensus expectations for respective monthly gains of 0.3% and 0.7%. Recent indicators on the labor market do not suggest downside risks there are increasing. The statement added a qualifier on average to its assessment that job gains remain low, as well as removing the qualifier somewhat to a view that inflation is elevated.

While things could change, there do not appear to be any strong advocates for tightening at the Fed at this point. Should energy prices start to fall, and core inflation lose momentum as the boost from tariffs fades, something Powell stated he expects, the debate is likely to return towards easing. However, it now looks unlikely that Warsh will be able to get a majority to vote for easing right at the start of his term. A lot can happen between now and September, so a move then cannot be ruled out, but it requires a lot to change before then. We no longer expect a move in September, though continue to expect a move in December, and an eventual move towards a near neutral rate of 3.0-3.25%. We now expect that to be reached in Q1 2027 rather than Q4 2026.