USD flows: Feeling the stretch (DXY, AUD, EUR, GBP)

A clash of themes coming to a head as over-accelerating AI, risk and commodity complex trades run into ongoing Iran standoff and the mini dollar squeeze

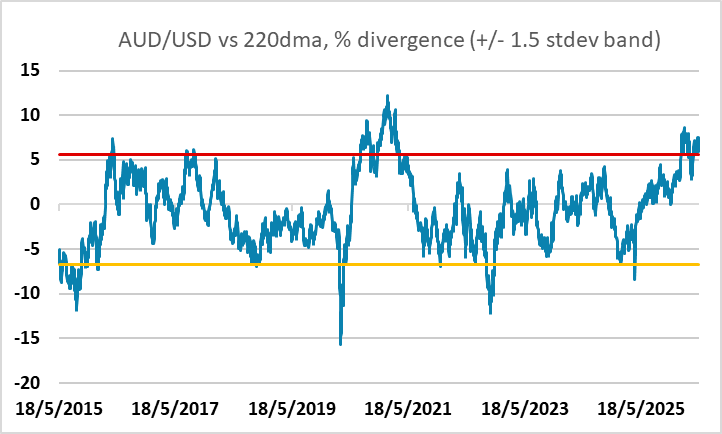

The likes of AUD, semiconductors, Kospi, metals, have been overrunning m/t trends, not to maximum excess, but to degrees that are vulnerable to a loss of patience on Iran, re-focus on supply risks, and a dollar squeeze

Without good news, sharper profit-taking / squeeze action could be seen in a flurry

One of the key themes highlighted over the week has been the divergences and tension between low volatility and high uncertainty and risk, and between ongoing oil strength and other (AI fever) risk on surge. Not that the themes are wrong but they demonstrate an increasing 'timeframe divergence' that can be hard to maintain indefinitely however high the convictions. And at a more basic level still, the extent of some of the over-acceleration stretches seen on the bullish side of the equation become problematic given this more multi-dimensional backdrop.

The stretched elastic bands are showing some signs of snapping back today when you look across the tech space, starting with the heated Kospi overnight, and the commodity complex.

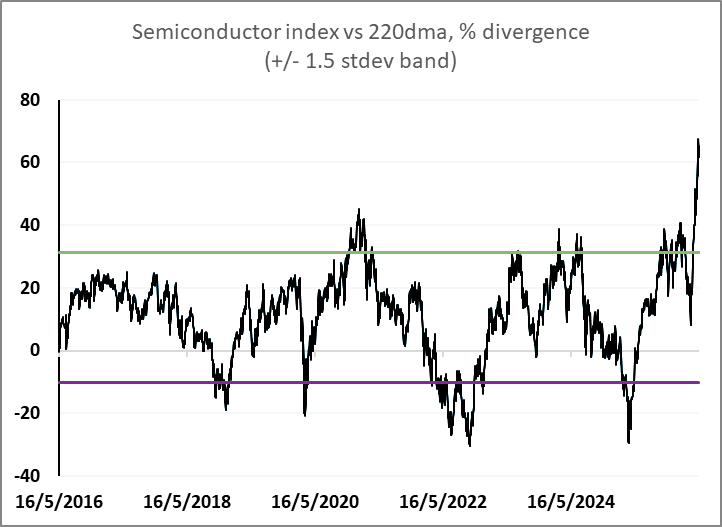

Semiconductors and related build-out indices and materials have been really stretching that band, however high the 1-2 year investment conviction - out accelerating trend to some +4 standard deviations, compared to the last decade. It's seen more dramatic acceleration excesses than that during the 1999-2000 blow off top, so it's not impossible to sustain. But the current backdrop, as the Iran war rolls on, is much more challenging for such divergence to last unchallenged.

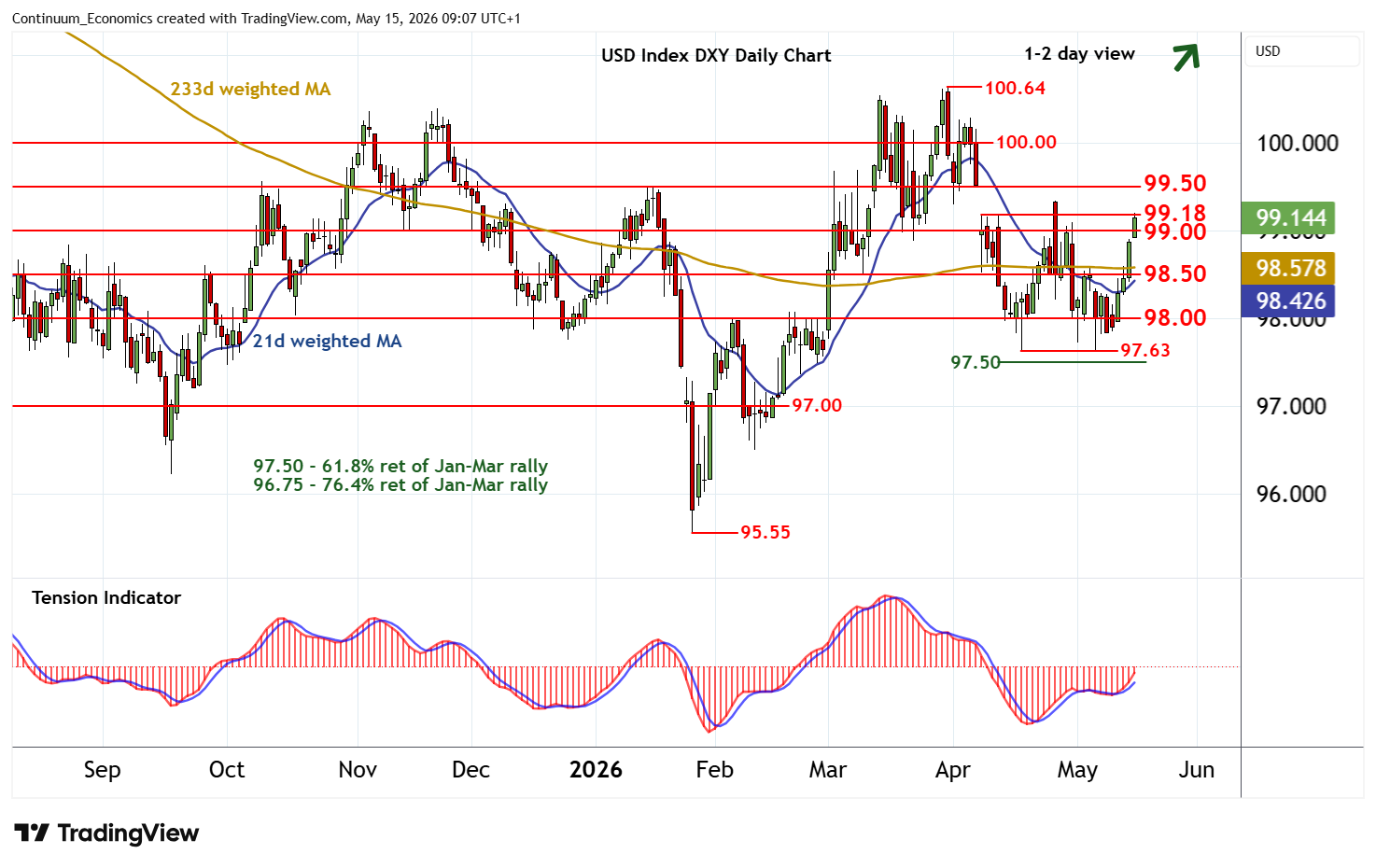

Likewise, AUD/USD, for example, has been more stretched of course, and the accelerations can be steeper. But the extent of the outrun of trend driven medium-term cycle drivers is tougher to sustain without snapback when risk turns off, the global growth picture remains challenged by lack of resolution in Iran and the associated supply worries, and the dollar squeeze itself adds to the mix. We've noted a dollar rally near-term is the most inconvenient trade for the market, and a break higher is in a sense also being a tail to wag the dog on the risk correction too.

The risk buy the dip mindset has been real but unless we hear some positive news over the weekend, current stretched short-term positional unwinds could gather some steam, especially if the options market dynamics that had been feeding the moves also turn around. Shakeouts can be short and swift when they come.