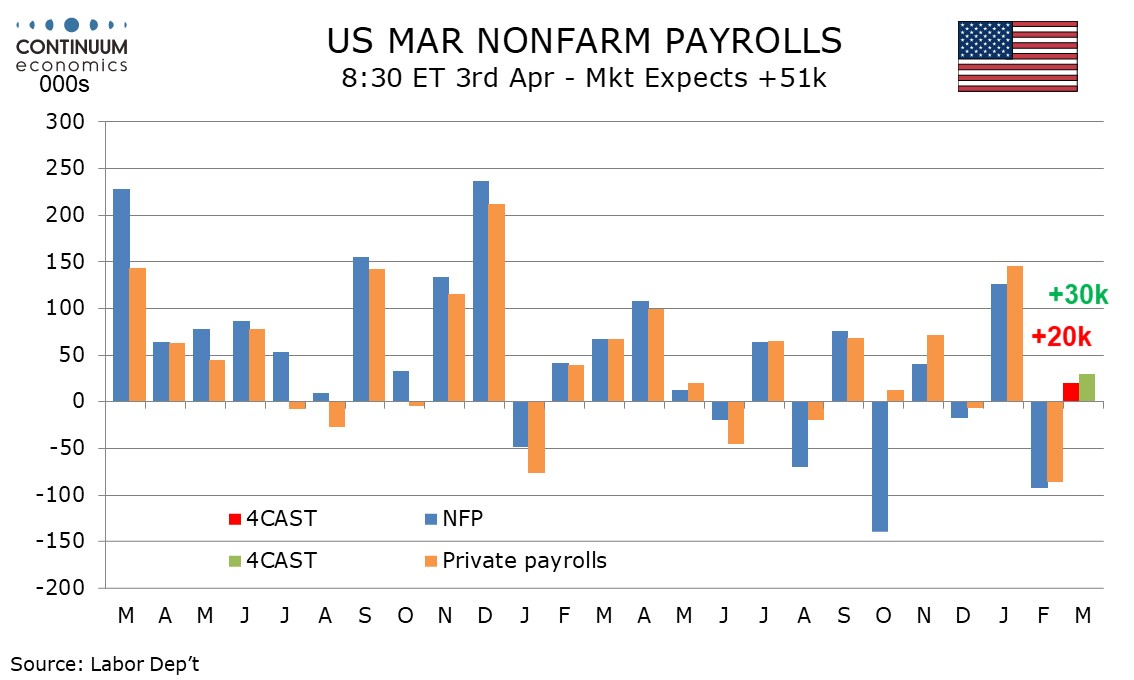

Preview: Due April 3 - U.S. March Employment (Non-Farm Payrolls) - Back to subdued trend after strong January and weak February

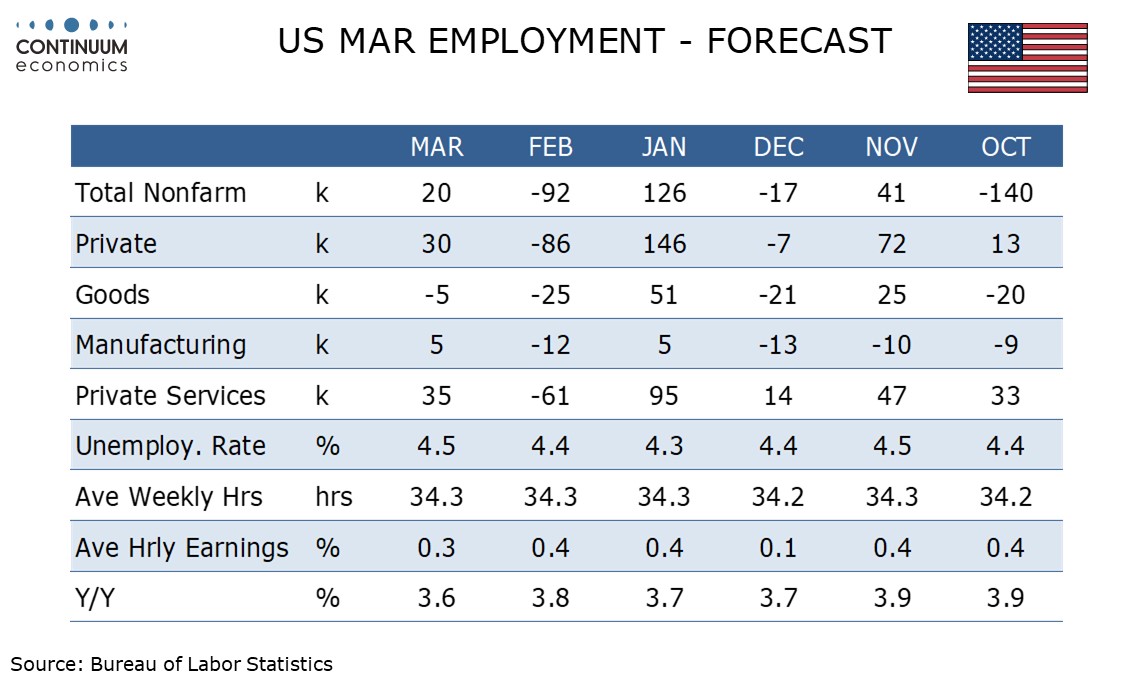

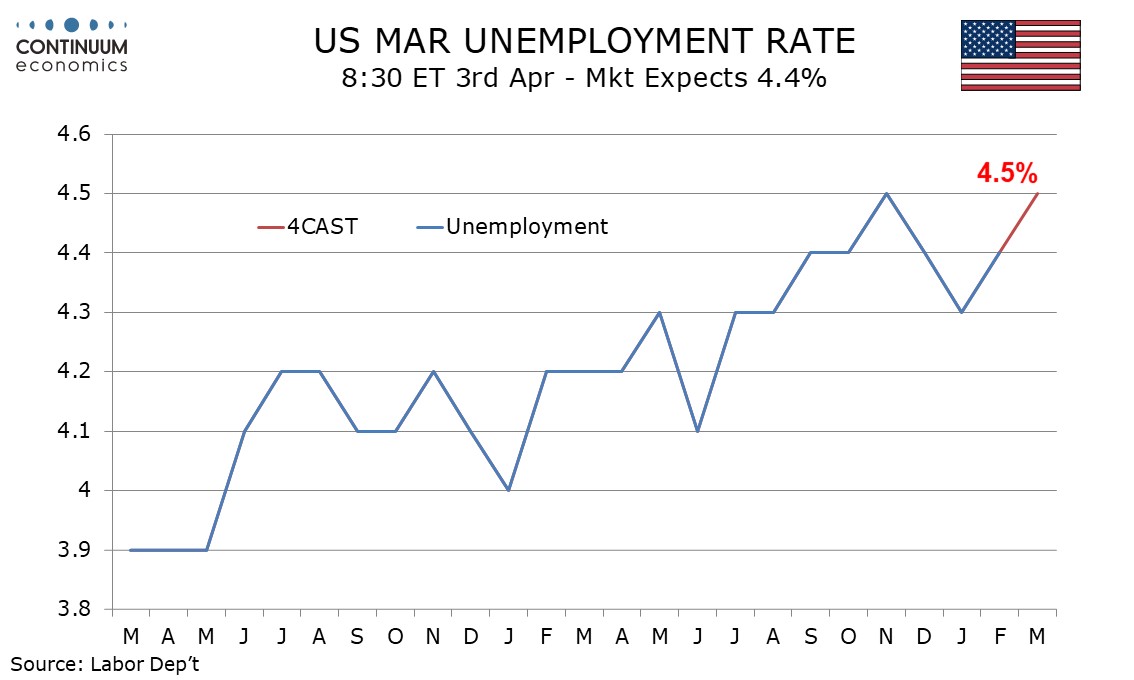

We expect March’s non-farm payroll to rise by a marginal 20k overall and by 30k in the private sector, returning to a subdued trend after a strong January increase was mostly reversed in February. A rise in unemployment to 4.5% from 4.4% and a slower 0.3% increase in average hourly earnings would further suggest a subdued labor market picture.

The average of January’s 126k increase and February’s 92k decline is 17k, while for the private sector a 146k January increase and a fall of 86k in February leaves an average of 30k. In December the three month private sector average was 32k and that for overall payrolls negative at -7k, depressed by particularly heavy public sector layoffs in October, as DOGE layoffs came through.

30k appears to be where the private sector trend is and government is likely to remain slightly negative even if the DOGE layoffs are now history. 30k may even overstate trend and risk for revisions is negative, though this month they are likely to be modest, insufficient to turn the private sector trend negative.

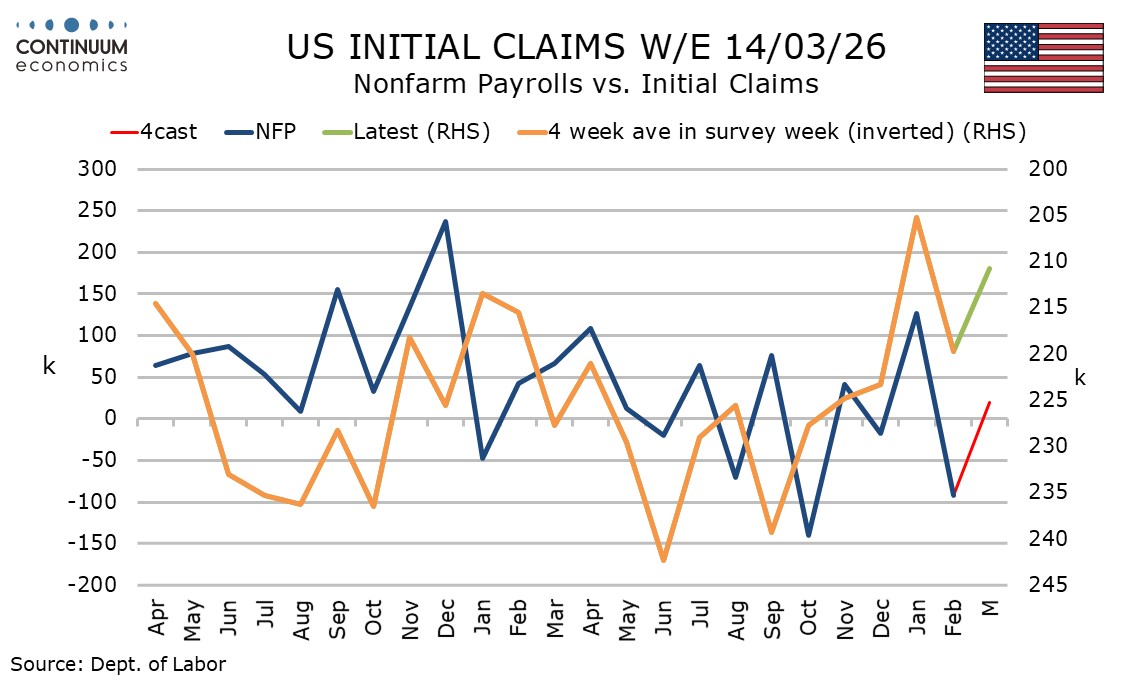

Initial claims remain low and were particularly so in the survey week for March’s payroll, when weather was unusually mild, though we do not expect weather to be a major net factor in March’s payroll with late February having seen some bad weather after that month’s payroll was surveyed. Low initial claims suggest limited layoffs, but continued claims have stabilized after slipping into January, suggesting hiring is limited too. Seasonal adjustments get increasingly negative in the spring, which adds to downside risk, but it is too early to expect a significant impact from the situation in the Middle East.

With payrolls unlikely to change much overall, few individual sectors are likely to change much. Most recent payroll growth has come from health care, and this was particularly volatile in January, surging by 116k before correcting lower by 19k in February. A return to trend is likely in March.

February’s unemployment rate was 4.44% before rounding suggesting risk is for a rise to 4.5% at least after rounding in March. The change is likely to be marginal, though we expect growth in the labor force to be marginally above that for employment. February’s participation rate of 62.0% was the lowest since December 2021. We expect a marginal rise to 62.1% in March.

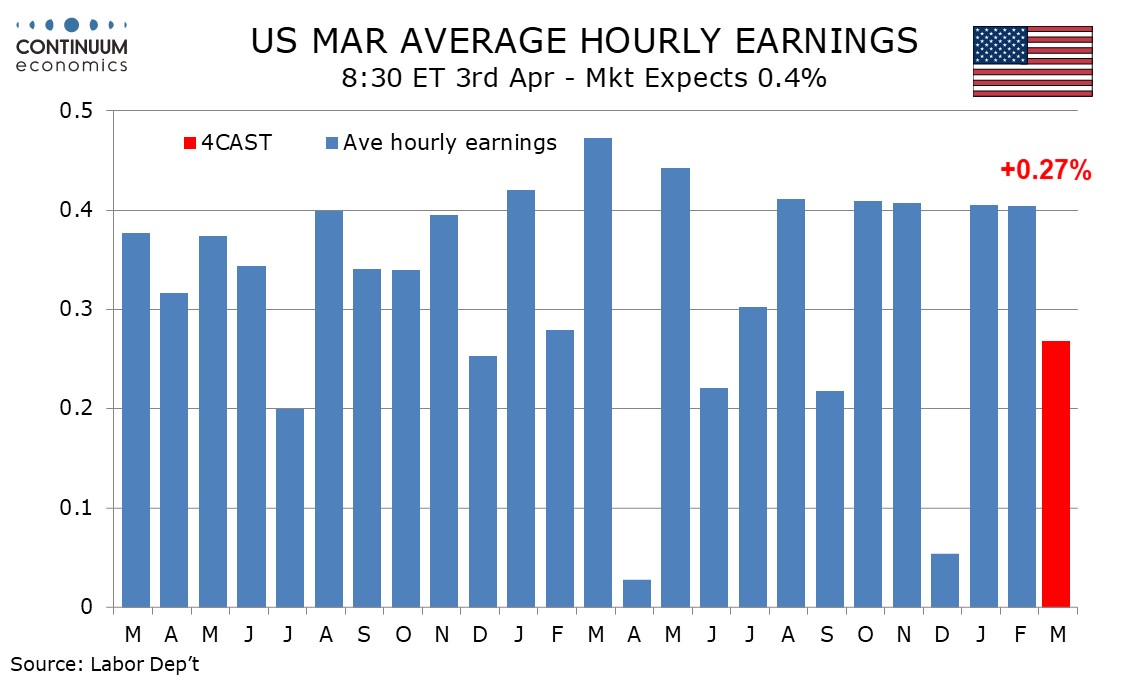

The last five months have seen average hourly earnings increasing by 0.4% in four but by only 0.1% in December. We expect March to increase by 0.3%, 0.27% before rounding, on the low side of trend after two above trend months. Yr/yr growth would then slow to 3.6% from 3.8%, which would be the lowest since July 2024. Higher gasoline prices may boost wage demands, but only if sustained.

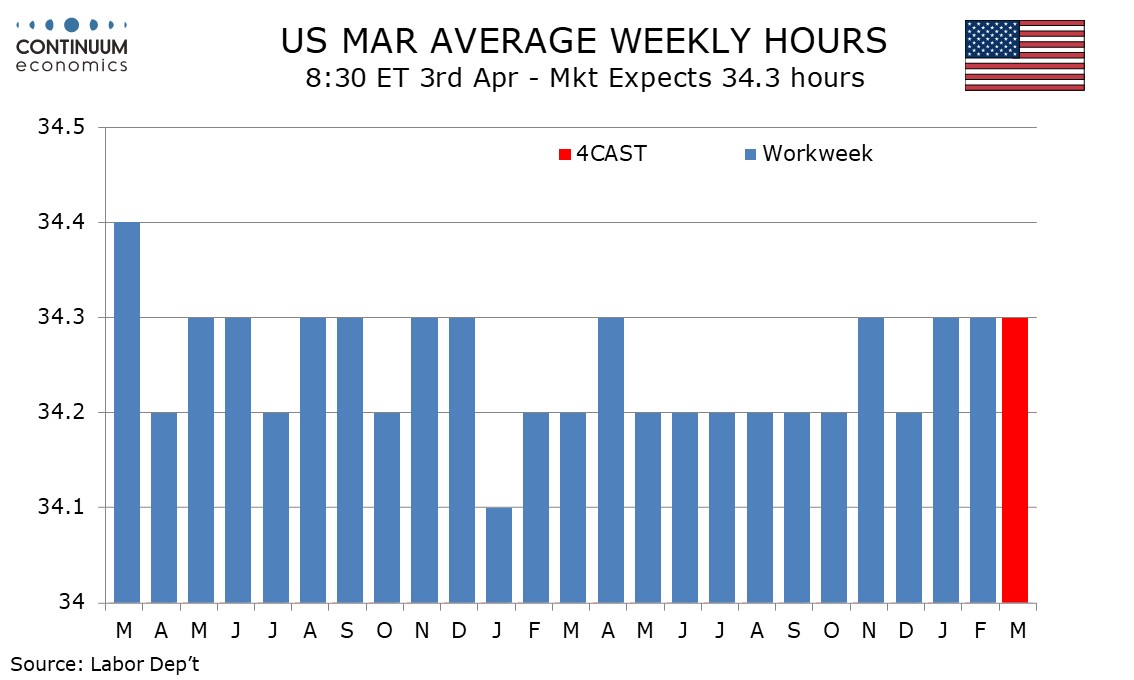

Three of the last four months, including January and February, have seen the average workweek at 34.3 hours, an improvement from six straight months at 34.2 ending in October. This is consistent with the economy still having some underlying momentum, with the slowing in employment in part due to reduced labor supply.