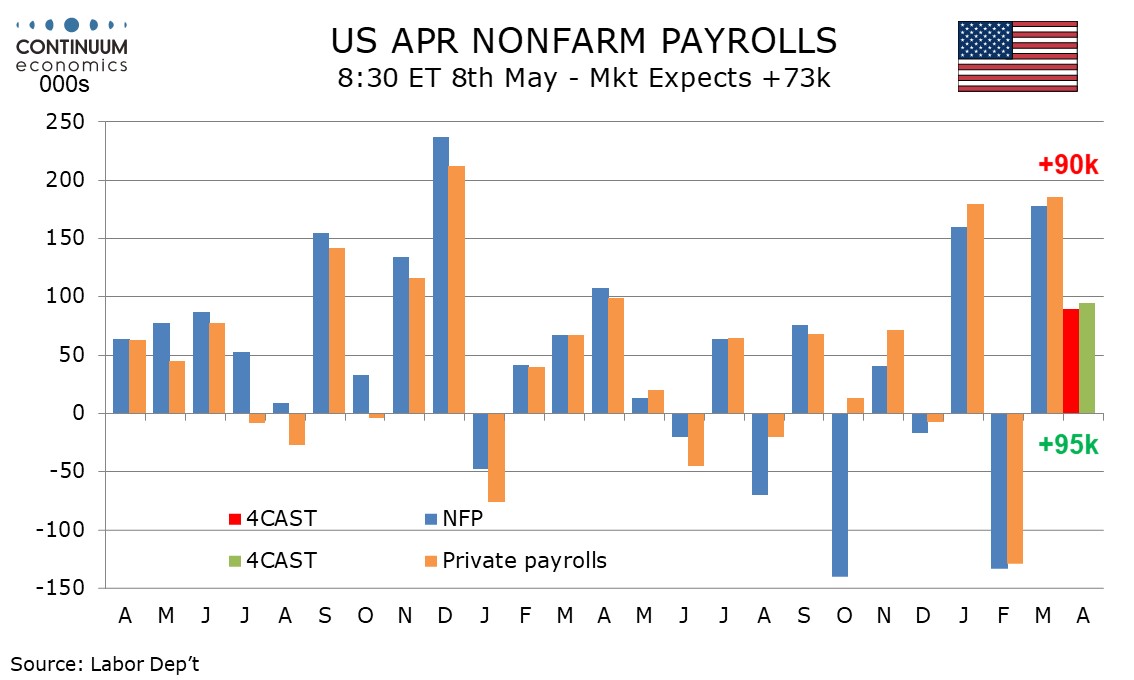

Preview: Due May 8 - U.S. April Employment (Non-Farm Payrolls) - Not as strong as March but some positive signals

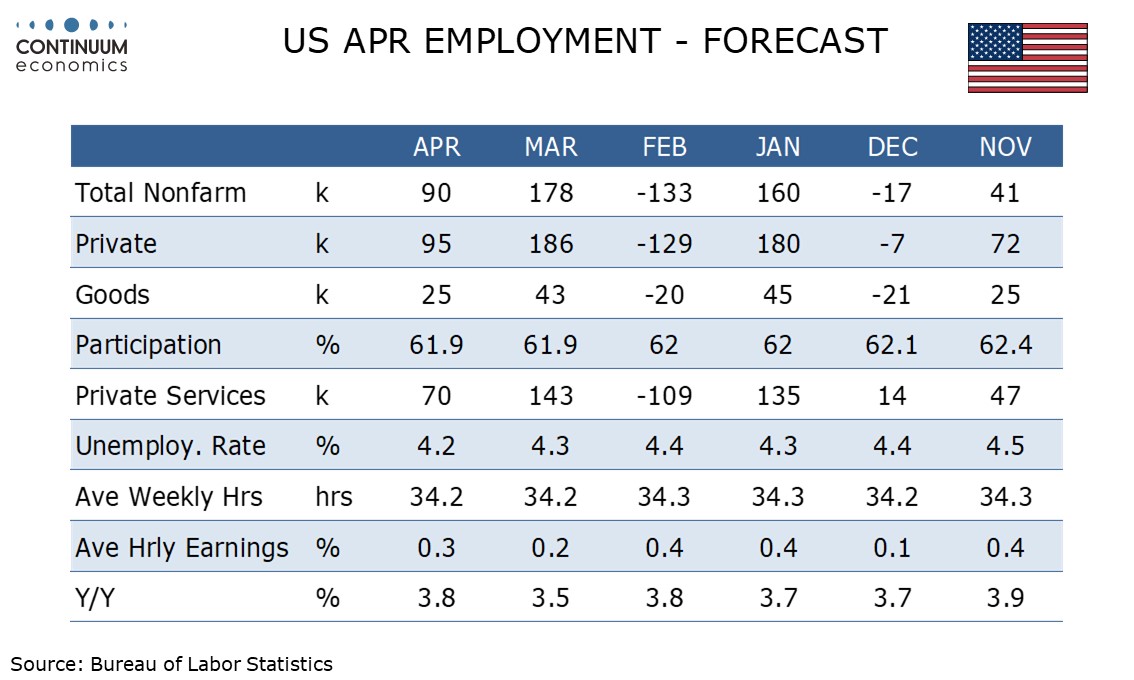

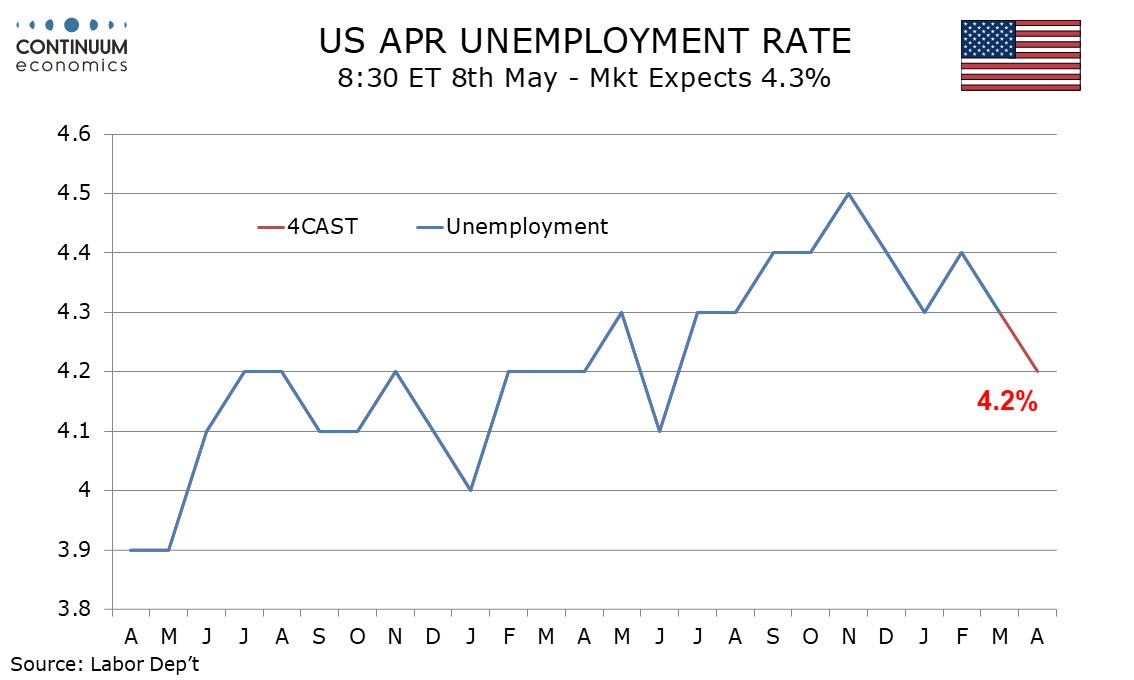

We expect April’s non-farm payroll to rise by 90k overall and by 95k in the private sector, less strong than in March but implying some improvement in trend. We expect unemployment to slip to 4.2% from 4.3% and an in line with trend 0.3% increase in average hourly earnings.

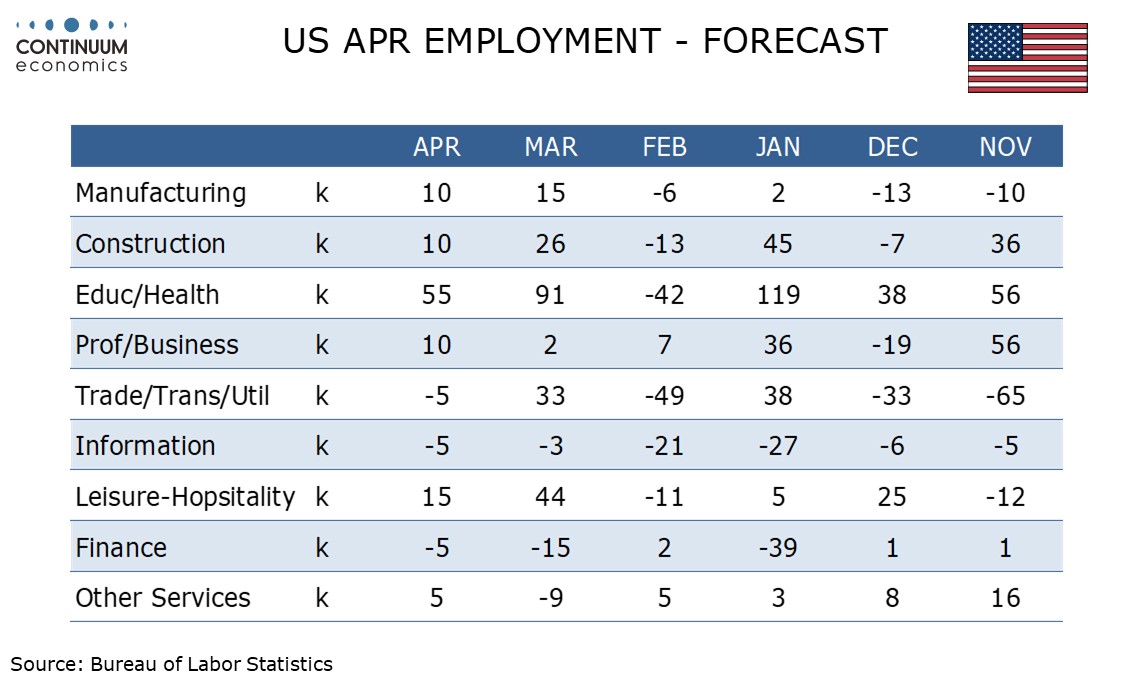

March’s 178k increase in non-farm payrolls was flattered by 32k returning strikers, who exaggerated a 133k decline in February. February’s weakness was also in part due to bad weather. March bounces in weather-sensitive sectors such as construction and leisure/hospitality will be difficult to match in April.

However our forecast is significantly higher than the average of February’s and March’s payrolls, and also a 4-month average of 47k (57.5k for private payrolls) which includes a strong January and a weak December too.

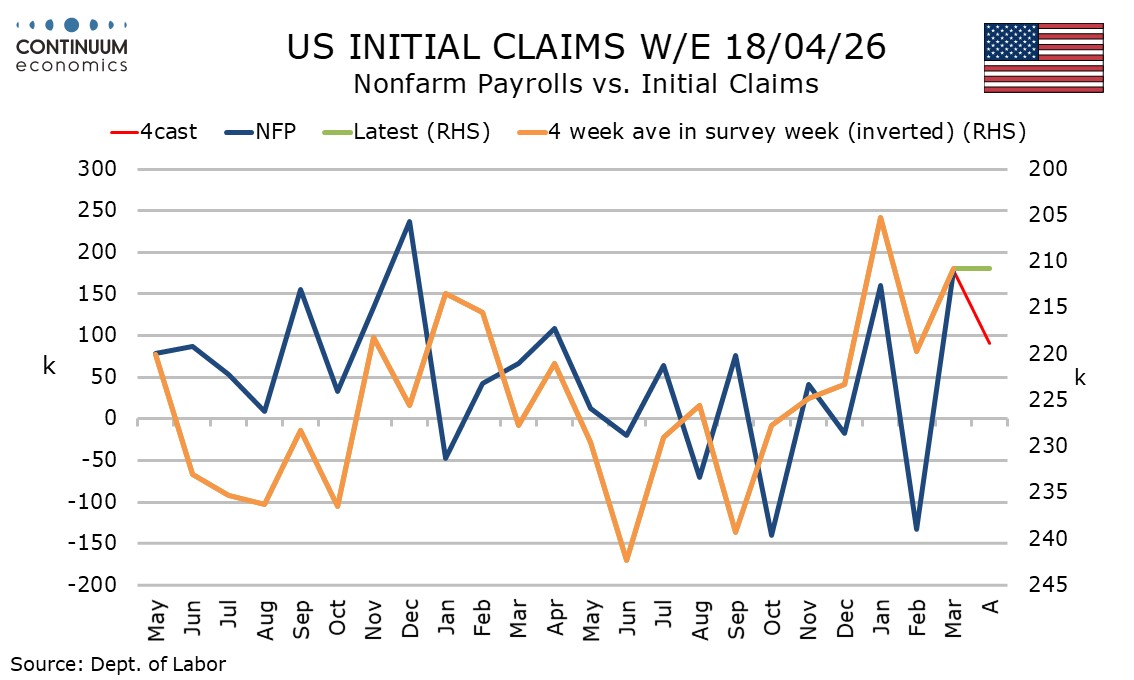

There are a number of signals for labor market improvement, with initial claims remaining low and continued claims resuming a downtrend. Weekly ADP data suggests job growth is averaging 40k per week, though this may be catch up with March’s strong payroll which ADP data underperformed.

Several manufacturing surveys hint at improvement in that sector, though payroll growth is likely to be led, as in most recent months, by health care. There is however some downside risk from higher energy prices, particularly in trade, transport and utilities, while AI is likely to be behind recent deteriorations in trend in finance and information.

The Conference Board’s consumer confidence report showed increased optimism on the labor market and this series has a good relationship with the unemployment rate. We expect both the labor force, by 150k, and the household survey’s estimate for employment, by 200k, to rebound from negative March data, seeing unemployment fall to 4.22% before rounding from 4.26% in March.

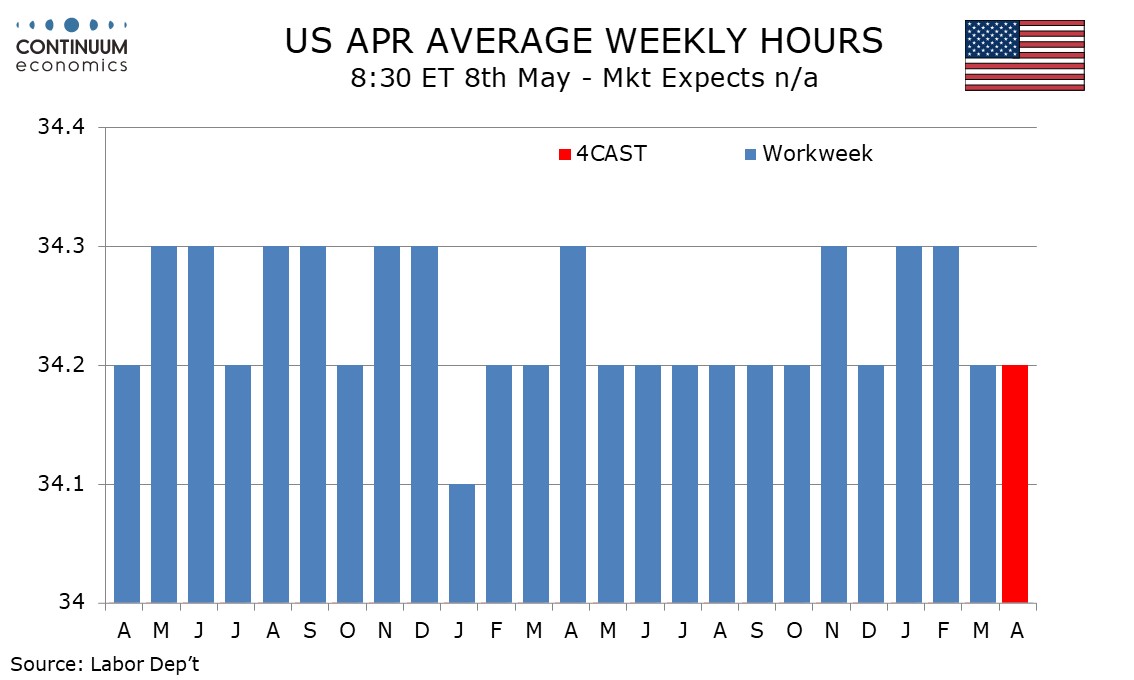

We expect a stable workweek of 34.2 hours though a return to the January and February level of 34.3 is more likely than a second straight slowing. We expect a modest 0.1% increase in aggregate hours worked.

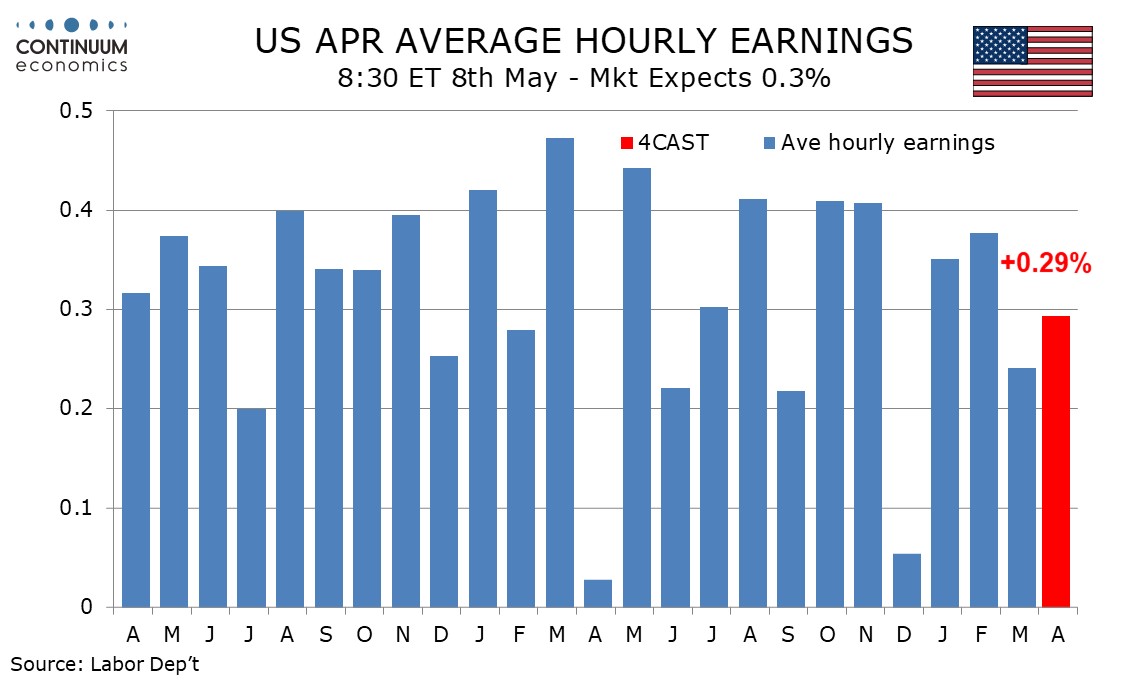

We expect average hourly earnings to rise by 0.3% for the first time since July 2025. Since then we have seen five increases of 0.4%, two of 0.2% and one of only 0.1%. Our forecast would see yr/yr growth pick up to 3.8% from 3.5% in March, which was the slowest since May 2021