BoE Review: MPC Playing Its Cards Safely (For Now)?

Very clearly, the BoE kept rates on hold with the MPC last month and the same decision was both expected and delivered this time around but with only token fresh dissent, with Chief Economist Pill wanting an immediate hike from the current 3.75%. But splits were more evident in the individual MPC member statements (as expected) where more diverging views in an around the three scenarios that the BoE is now projections all based on modest hiking of around 50 bp over the coming year. We still think that the BoE is offering too much information in these individual views and as a result is confusing markets just as it did in March. But among the key and relatively common themes is that financial conditions have tightened even without actual hikes and that the labor market is loosening. And it this tightening that pulls policy severely back towards conditions when Bank Rate peaked that makes up see a much softer real economy outlook than the strangely similar GDP outlooks in all of the BoE scenarios.

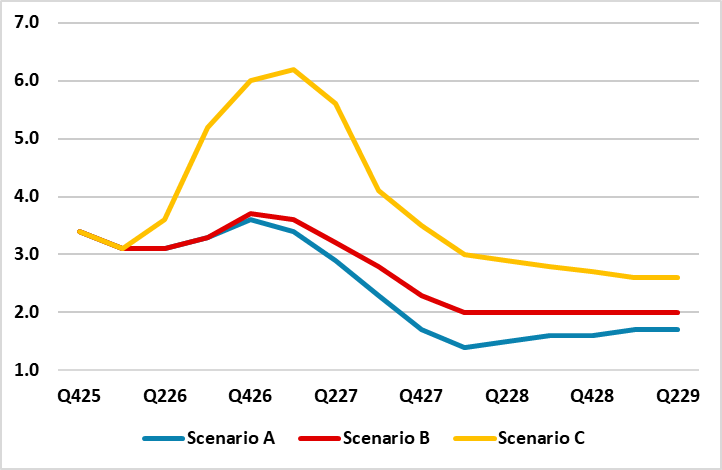

Figure 1: The BoE’s Three Scenarios

Source: BOE

What is notable and as the updated projections do show, is that this energy shock is justifiably viewed by the BoE as being different to that of 2022, occurring at a point when the economy is operating with a margin of spare capacity and where policy is already restrictive. We think this very much reduces the chances of second round effects as does the already loosening labor market where earrings growth have slowed to a rate consistent with the 2% inflation target.

Given ever tighter financial conditions, which received several mentions in the BoE updates, we still see at least two and probably three more 25 bp rate cuts ahead but now deferred to starting no sooner than Q4 and then extending into 2027. Admittedly, rate hikes still seem to be the more likely policy more implicit in BoE thinking, with some suggestion that without them then the tightening in financial condition seen of late would not be validated. We think this is misplaced, not least as some of the tightening in conditions affects the likes of political and fiscal risks. As for the three scenarios (A seeing energy prices follow market thinking while C sees not only higher energy costs but more persistently too) we are puzzled that the combination of the energy shock and more restrictive policy not only fails to deliver any kind of recession even in the most severe scenario but that all three outcomes see little variation in the growth outlook – ie just 0.1 ppt per year between each outlook and little more difference from the baseline outlook offered in February

It is notable that Governor Bailey has recently referenced the approach of the BoE in 2011, which kept rates on hold even as UK energy inflation soared to 20%, citing its mandate to tolerate deviations from target in a bid to avoid unnecessary harm to the economy and jobs. A BoE survey of senior executives released of late offered tentative support for Bailey’s implicit wait-and-see approach (or what he prefers is an ‘active hold’), with evidence that companies will resist inflation-fuelling pressure from workers for higher wages in response to the current crisis. The expected wage growth reading in the regular BoE-compiled Decision Makers Survey is among the weakest since 2022 and would also point to pay growth on track to be broadly consistent with the BoE’s inflation target. The survey also showed expectations for employment growth falling into deeper negative territory, while consumer price expectations were higher for the coming year but stable at three-year horizon. All of which adds to a picture of a UK economic backdrop vastly and increasingly different to four years ago.