EZ HICP Review: Headline Higher, But Core Messages Still Friendly?

There were mixed messages in the November flash HICP. Matching consensus thinking, the headline rose 0.3 ppt to 2.3%, but where the core stayed at 2.7%, partly due to what is seemingly stable services inflation. Higher energy costs, mainly base effects, were the main factor behind the rise back from October, having fallen to a well-below target 1.7% in the previous month (Figure 1). Regardless, shorter-term price momentum data already suggest that core and even services inflation are running around, if not below (Figure 2), target and given sharp, falls in wage tracker data, headline services inflation may succumb more clearly soon, something backed up by surveys for the sector. However, there are some signs in retailing surveys suggesting disinflation may have stalled (Figure 3). But this may be of increasing secondary importance to most of the ECB Council as a) inflation is already consistent with target and b) a fresh and more demand driven disinflation could be triggered by what seems to be weaker real economy backdrop that could also exacerbate financial stability risks.

Figure 1: Headline Rises Back as Services Resilience Persists

Source: Eurostat, CE

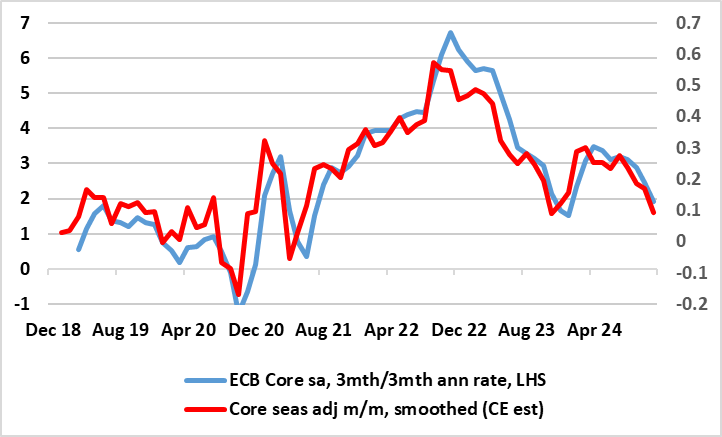

Regardless the headline HICP rate may edge up a notch or two in December, but with the core staying put. Adverse energy base effects will (again) be the cause, making it all the more important to look at shorter term price dynamics, (ie adjusted m/m data), which suggest on target core inflation even on the ECB’s preferred measure (Figure 2)

This backdrop has persuaded the recalcitrant ECB into a reassessment. In fact, the ECB has brought forward inflation hitting target durably now to be in the course of next year as opposed to late 2025 as suggested in the September projections and this is likely to be made clearer in the December forecast update. But amid tentative signs of consumer recovery and resilient services inflation, it would be premature to expect anything more than 25 bp at that looming December Council meeting. However, the question arising is if the ECB flags faster easing into 2025 as we think is increasingly likely.

Figure 2: Core Inflation Around or Below Target in Shorter-Term Dynamics?

Source: Eurostat ECB, CE

Indeed, it seems that worries about weaker growth are reverberating more discernibly within the ECB. Moreover, the worries are twofold. Clearly, weaker growth risks possible (added) downside risks to inflation. But the ECB is now also flagging elevated financial stability vulnerabilities according to its just-released Financial Stability Review (FSR). It notes risks to economic growth that have shifted to the downside and where growth fears have resurfaced as a key source of uncertainty particularly to firms where debt servicing is possibly more of an issue. All of which chimes with our long-standing concern of downside risks that may be materialising to what we still see is a below-consensus growth outlook. It could be argued therefore that ECB easing is needed not only to minimise downside inflation risks but also help repair debt servicing capacity (for sovereigns and companies) and persuade households to run down elevated savings!

In this regard, for us, and seemingly now the ECB, recent survey data, rather than just inflation, may be increasingly influential. Such data are pointing not only to more real economy weakness but also to significant falls in cost and output price pressures, albeit less so in regard to retailers’ price expectations (Figure 3). These considerations are all the more important as the ECB hierarchy has made clear policy will be shaped by an array of data rather than any particular data points. Indeed, this survey weakness remains the main reason we expect a further 75-100 bp of cuts by next summer.

Even though the services rate is well below that seen in many other DM environments, ECB hawks on the Council will point to is apparent resilience. But the doves may counter by pointing to what is a much earlier than expected drop below target as well as recent much softer wage inflation news, most recently in terms of a sharp drop in the monthly Indeed Wage tracker (at 3.25% is the lowest since early 2022), something that augurs well for lower services inflation in due course.

Figure 3: Retailing No Longer Reining in Price Expectations - For Now?

Source: Eurostat, European Commission, Continuum Economics