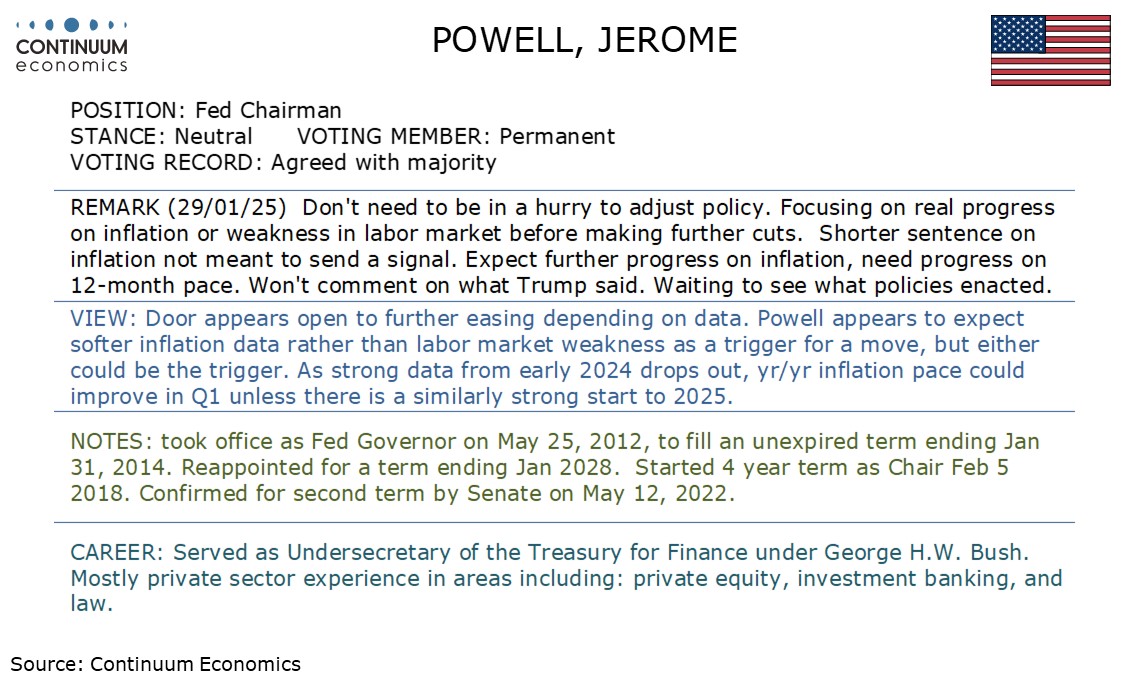

FOMC still data dependent in uncertain policy environment

A more hawkish interpretation of the data in the statement appears to be more a justification for the FOMC’s decision to leave rates on hold at this meeting rather than a signal for a protracted period of steady policy. There is still scope for renewed Fed easing if either inflation or labor market data weakens, and we will see two months of employment and CPI data before the FOMC next meets on March 19.

The most significant adjustment to the FOMC statement was a removal of a reference to inflation making progress toward the 2% objective, though Chairman Jerome Powell stated at the press conference that this was not intended to send a signal. He added that he expects further progress on inflation, with focus on yr/yr growth. As strong data from early 2024 drops out, yr/yr rates look likely to slip in early 2025.

The statement was also adjusted to reflect a stabilizing unemployment rate rather than modest increases seen since early 2024. Powell suggested that a weakening of the labor market could also be a trigger for renewed easing, but that does not appear to be the Fed’s expectation. We expect slower payroll growth in January due to bad weather, though we would probably need a weak February as well for the Fed to be seriously concerned.

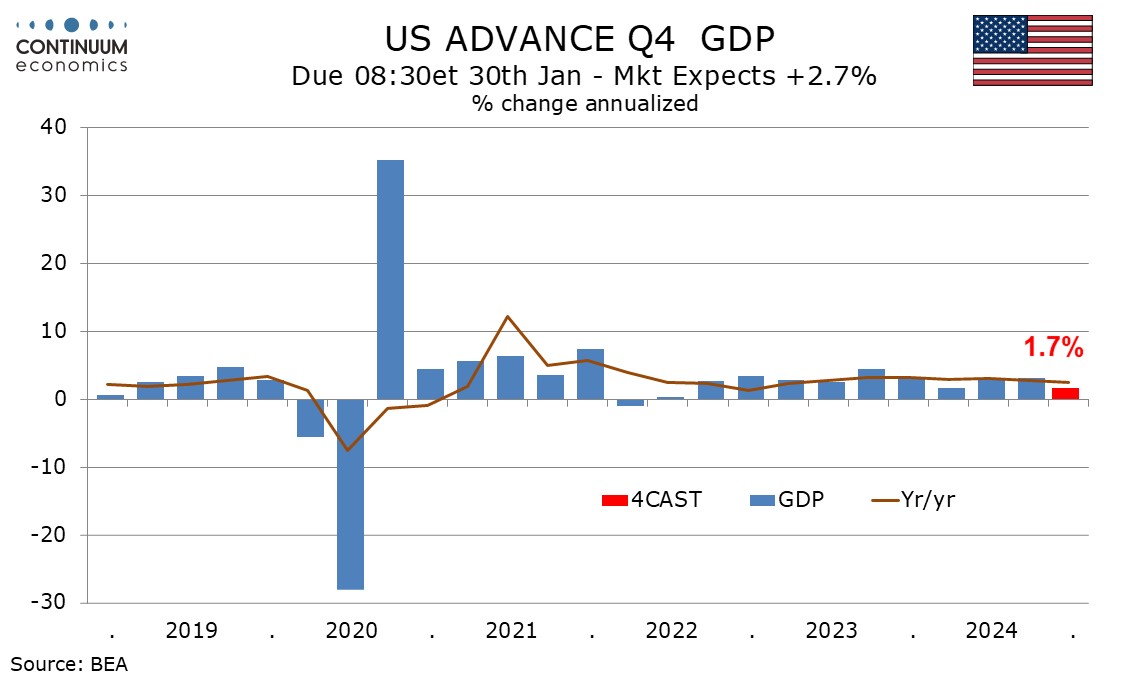

The statement continued to see the economy as expanding at a solid pace, though in the morning before the decision weak December trade and inventory data prompted us to revise our forecast for Q4 GDP down to 1.7% from 2.6%. Powell also suggested business investment had slowed in Q4, pointing to a further downside risk. Powell was careful not to be drawn into discussions on President Trump and potential policy changes under his administration. While acknowledging uncertainty, he added uncertainty is always with us.

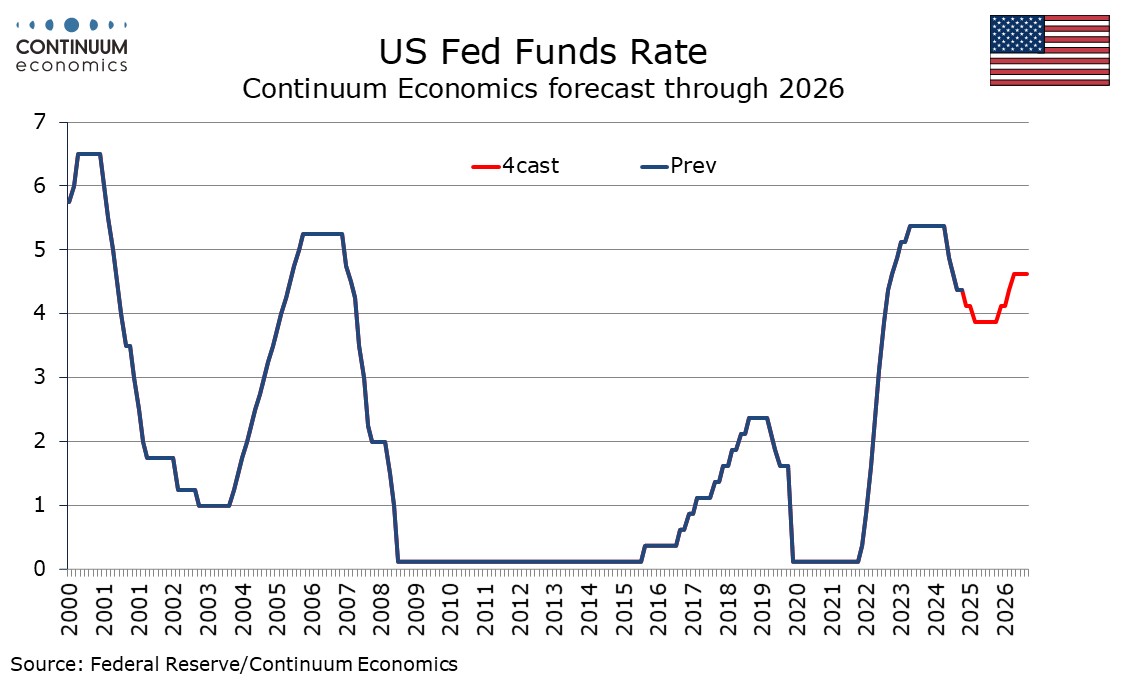

Our current FOMC projection looks for two 25bps easings in 2025, currently penciled in for March and June, though the March call looks like quite a close on dependent on data. We are looking for 75bps of tightening in 2026, on a view that tariffs and a smaller labor force will lift inflation, though if and when policy changes that lift inflation are implemented is highly uncertain. Our current view is that Trump will not rush into tariffs, expecting no action against Canada and Mexico that has been threatened for February 1. However, if significant cuts in government spending are not implemented, tariffs may look increasingly attractive as a potential revenue source later in the year.