ECB Review: Disinflation Still On Track But Policy now ‘Work in Progress’

Unsurprisingly, the ECB verdict was less important that the rhetoric. A sixth 25 bp discount rate was widely expected – and delivered - to 2.5%, but how wide the door is left open for further cuts may be more opaque. This both reflects gauging the extent of any lingering degree of policy restriction and by the likelihood that even with the updated ECB forecasts with inflation under target from 2026 onwards thereby consistent with policy rates falling to around 2%, those projections now look out of date. The possible fiscal and defence initiatives now emerging for the EZ have to be counterbalanced by opposing and downside risks from US imposed tariffs. Hence why amid what was termed phenomenal uncertainty, ECB policy guidance was far from resounding this time around. Some added clarity should be available by the next (Apr 17) Council meeting but we are less confident that another 25 bp may arrive at that juncture. Given what may be offsetting emerging upside and downside risks but where our perceived result of what being data dependent will bring about, we adhere to the discount rate falling to 2% but it may be later than the mid-year estimate we previously envisaged.

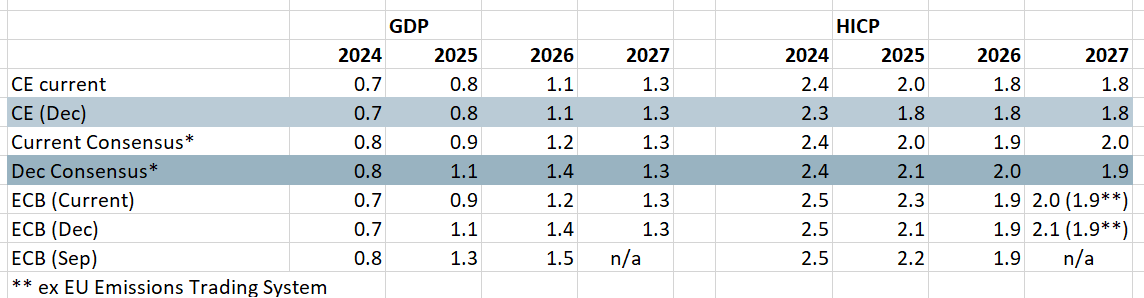

Figure 1: ECB Shifts Down to Consensus on Growth?

Source: ECB, Bloomberg, CE

Gauging Restriction

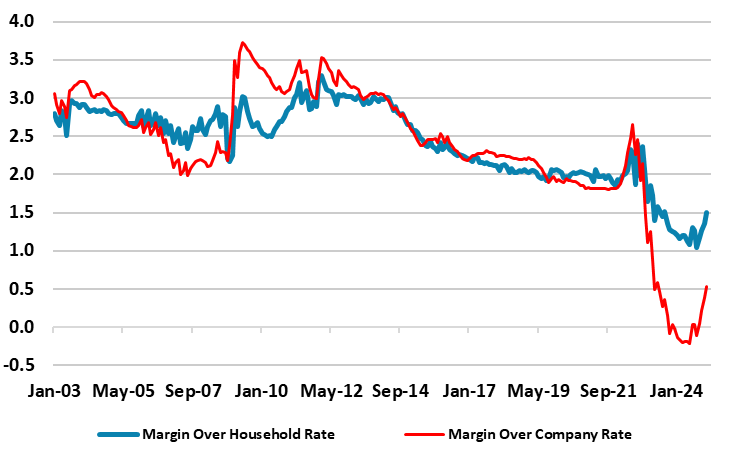

Last time around, the ECB stressed monetary policy remained restrictive albeit with differences on the degree and the likely the debate on this issue may have been more intense this time around. Indeed, while amending the analysis to suggesting ‘monetary policy is becoming meaningfully less restrictive’ is justified, the change in tense by noting becoming rather than remains, probably reflects ECB thinking that policy restriction is better based on an array of factors not one particular policy rate as it reflects just how the transmission mechanism is actually faring. It may also reflect a growing acceptance that even policy rate reductions are taking time to filter through into the rates at which borrowing actually occurs. The transmission mechanism, after all, determines not just the cost of borrowing but bank’s willingness and ability to supply credit. In this regard, perhaps a key factor is the margin that banks lend relative to any policy rate. This margin has narrowed markedly of late (Figure 2), the question being whether banks will seek to rebuild lending margins back to those seen prior to the pandemic, thereby actually acting not only to slow the impact of policy easing but even to offset it.

The Policy Outlook Getting More Complicated and Uncertain

It could be argued that the updated ECB forecasts are already out of date as they understandably fail to account for the fiscal and defence initiatives that are emerging in the EZ and most notably from the likely new German coalition. These and other factors need to be taken into account in due course by the ECB, hence why President implied policy thinking as being ‘work in progress’ certainly in regard to defence issues. The attempt to change fiscal rules to allow for higher defence sending is something Germany is now planning but also advocating across the EU/EZ. For Germany, the defence shift could add some EUR 40 bln per year to the economy (nominally and potentially), ie potentially by some 1 ppt to around 2% in real terms for 2026. The question being how much would actual boost German growth as German defence currently purchases over 75% of its equipment spending from abroad and mainly from the U.S. That could change if German companies are confident the defence boost will persist but in the short-term Germany would also find it difficult to get rapid increases in defence equipment given existing lags in orders. But the infrastructure initiative based around the creation of an off-budget infrastructure fund with worth EUR 500 billion over 10 years is the more notable as it could raise nominal GDP by 1%-plus annually but again may take time to get underway as there will be questions about what are the spending priorities, although the speed at which the CDU and SPD have agreed this initiative bodes well for their likely collation. More notably, the initiative could also raise Germany’s feeble potential GDP rate which the EU estimate is a current paltry 0.6% per year. With Germany some one third of the EZ a possible 1% boost to growth into 2026 could add around 0.4 ppt to EZ growth and possibly more with Germany also calling for EZ fiscal rules to be relaxed more generally.

Figure 2: Bank Lending Margins Too Low to Last?

Source: ECB, CE

Pluses vs Minuses

But this is where it gets even more complicated. Any such upgrade to the EZ outlook would largely result in – as far as our thinking is concerned – merely take the 2026 GDP picture up toward the ECB’s optimistic projection it offered three months ago. Of course there may be some further impact into 2027 but this is uncertain given the factors spelled out above, these added to by how and when any EU-wide defence boost comes to fruition. But there are downside considerations, not least the looming risk of U.S. imposed tariffs of around 25% on EU exports. This could hit the EZ economy by easily the same amount as the possible boost from Germany’s altered fiscal plans, especially as Germany would be possible the most exposed EU country meaning that the circa-1% boost to the growth in 2026 may effectively be halved. And if the EU chose to levy reciprocal tariffs the damage may on balance be negative. There is also the risk from higher interest rates – both the actual rise in bond yields and the possible more limited and/or deferred ECB easing outlook. This could both hit activity directly as well as heightening the risk of fiscal tremors in some heavily indebted EU countries especially if the European Commission to raise around EUR 150 bln that could be disbursed to EU individual countries s as loans to invest in the arms industry fails to materialise. And of course amid these plus and minus factors for the EZ outlook it as unclear what impact there will be inflation.

Other Considerations for Next ECB Meeting

As for being data dependent which the ECB insists it will be even more drawn to, the non-hawks on the Council may be more influenced by the business survey backdrop, still concerned that they still imply little to no growth. In particular, amid an ECB central view that consumer spending should pick-up further helped by real incomes growth, this is being threatened by what may be a clear emerging slump in the labor market. And as even the ECB noted this time around, European Commission survey data now echo PMI numbers in suggesting falling employment including in hitherto solid services. Thereby this questions the ECB projection of circa-0.5% jobs growth and helping to explain recent much softer wage signals.

In addition, the inflation picture is showing better underlying conditions, something that flash February HICP data did highlight. Indeed, we suggest inflation (even for services) is already behaving as it is at target – if not below when assessed on an adjusted shorter term time frame – NB the January Council account very much noted the importance of services inflation once again and also pointed to measures of underlying services inflation (ie persistent measures) already near 2%. Indeed, a clear inflation undershoot is still envisaged even with the dip below target now deferred to 2026. But core inflation minus indirect tax changes based around EU Emissions Trading System plans still see a rate increasingly below 2% through 2027!

All which implies that while the ECB may not have altered its underlying theme as to the direction of travel for policy, but it is possible that the speed of travel may bow have slowed.