German Data Review: Headline Jumps Energy Base Effects?

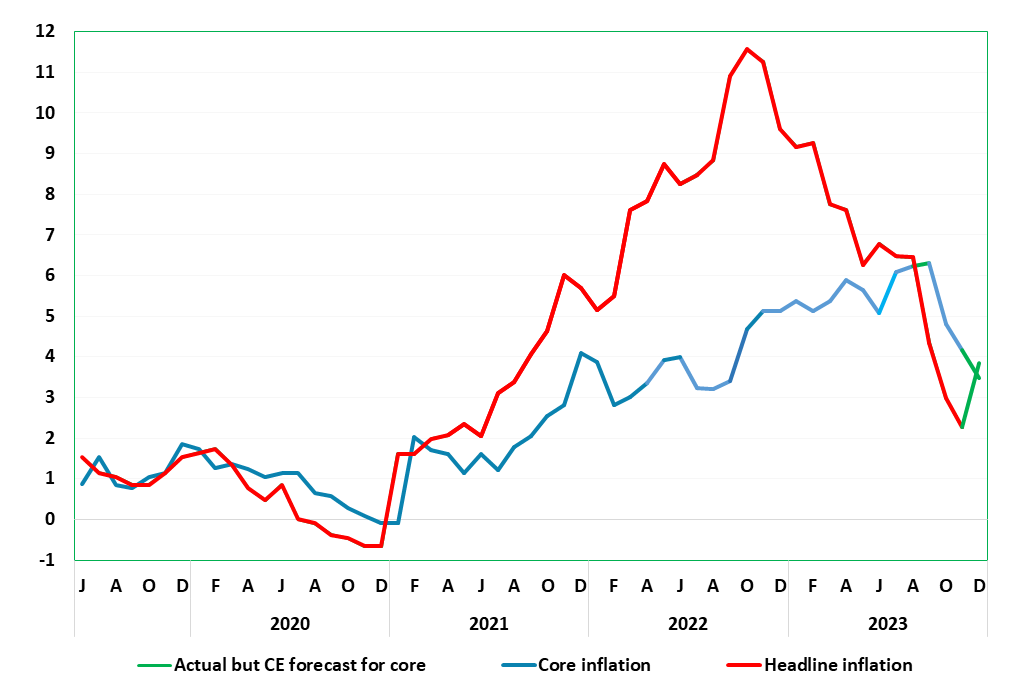

A clear and continued fall in overall German and EZ inflation pressures, initially evident in survey data but spreading to official numbers has been the case for some months. This downtrend was much more evident in the softer-than-expected October and also the November HICP numbers. Indeed, the headline HICP in November eased 0.7 ppt to 2.3%, a 29-month low, with the core dropping by 0.7 ppt to 3.5%. However, last month, and despite a further fall in fuel prices, recreation-sourced and particularly energy-related base effects, pushed up the headline rate back to 3.8%, a little lower than consensus and with the core down further at least for the CPI measure (Figure 1) where the headline for the latter rose by far less. Regardless, the disinflation backdrop is underlined by what may be a softer core seasonally adjusted trend (Figure 2) which may be running close to zero. Regardless, the headline y/y rate may resume a downtrend in the New Year even with some tax rises now due.

Figure 1: HICP Inflation Jumps, But Core More Contained

Source: German Federal Stats Office

EZ Implications

Adverse energy related base effects may have affected other EZ countries such as Italy, as well as in France. But progress on core inflation should continue, this very much the case in recently related Spanish numbers. As for the actual EZ HICP due tomorrow (Jan 5), the headline tick higher from November’s 2.4% by 0.4-0.5 ppt, but only on a short-lived basis as the fall will resume into and through 2024. We see the December core steady at 3.5% but with downside risks. As for the ECB, its forecast outlined last month implies a rise of around 0.25 ppt and a slightly higher headline outcome than our expectation.

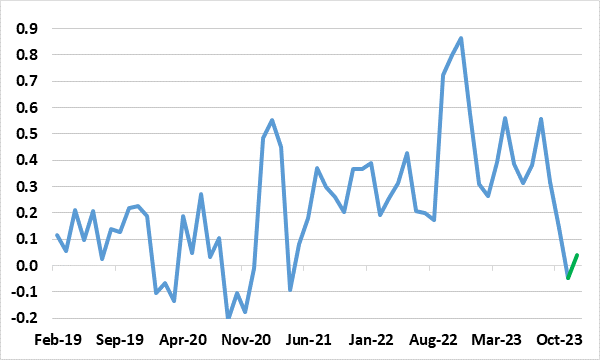

Disinflation Continues Meanwhile

Regardless, a further insight into the disinflation backdrop is provided by the seasonally adjusted data which we compute – the Bundesbank does its own measurement on this basis. As Figure 2 shows there has also been a clear slowing in the trend m/m changes on an adjusted basis, most notably for the core. This seemingly continued in December albeit with the smoothed (3-mth avg) adjusted rate edging up to just 0.1% m/m

Figure 2: Adjusted Core Rate Has Fallen Clearly

Source: German Federal Stats Office, CE, % chg m/m, smoothed

This is important amid the jump in the y/y rate, reflecting largely energy related base effects – mainly attributable to a reduction in government subsidies on gas and electricity that began last year.

Some Fresh Upside Price Risks?

Regardless, amid the clear fall in headline and core rates in recent months, fresh upward price pressure risks have emerged of late, albeit little to do with demand. Events and shipping risks in the Gulf clearly pose such a risk, albeit hard to estimate and also beyond energy given the rise possible to transport costs. More specifically to Germany, upside price risks stem fiscally as the German government is being forced to scrap several subsidies and increase taxes in order to help fill a circa-€ 60 bn hole in its budget plans left by a constitutional court ruling against its use of off-balance sheet funds. One example is that the government has already raised the VAT rate on restaurant meals from a temporarily reduced level by 12 ppt to 19% at the start of this year, something that has prompted us to revise up out current quarter CPI profile. Importantly, this also has the ability to affect core numbers, although any such impact may add to already clear pressures on spending power which we think ill erode pricing power further.

Against this backdrop we now see German HICP inflation rising a notch this quarter from the 3.1% rate averaged in Q4 last year but then fall to 2% in Q3 this year.