SEK, USD, JPY flows: SEK softer on weaker CPI, USD falls, JPY gains on suspected intervention

SEK dips as CPI comes out weaker than expected - further decline possible. USD generally softer on hopes of US/Iran deal. JPY surges on suspected intervention.

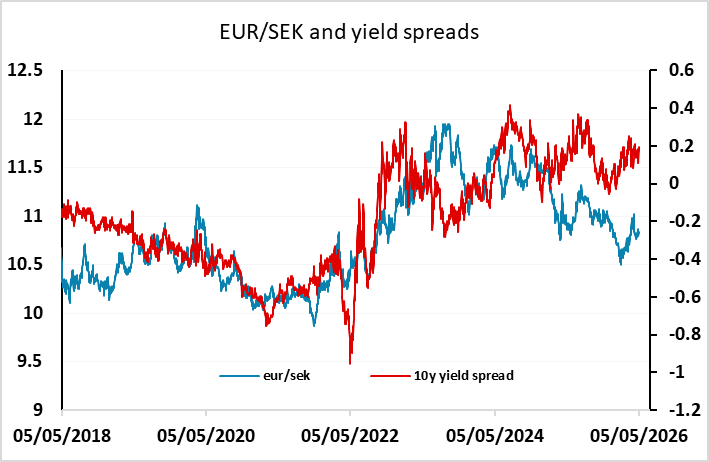

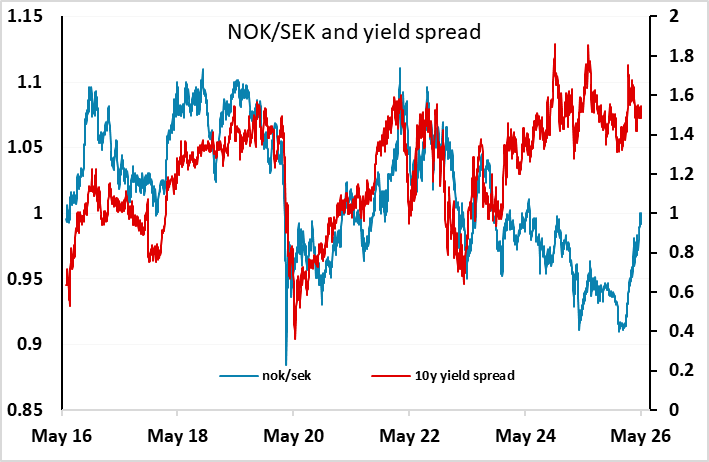

First up this morning we see considerably weaker than expected Swedish CPI, coming in at -0.6% m/m and -0.1% y/y, against market consensus of -0.2% and +0.3% respectively. EUR/SEK has popped up a couple of figures to 10.82 in response. The modest reaction to some extent reflects the fact that the market has no expectation of near term tightening from the Riksbank, with one hike priced in this year, but not until November. The soft CPI data may reduce market expectations of this hike, but won’t much change the near term view. Even so, EUR/SEK continues to look on the low side given current yield spreads, having been held down by the weakness of EUR/NOK in response to the rise in the oil price. While NOK/SEK has risen sharply, there is some impact from NOK strength against the EUR on the SEK. But this may not persist and the risks for EUR/SEK still look to be on the upside, especially if the ECB hike in June as is 80% priced in.

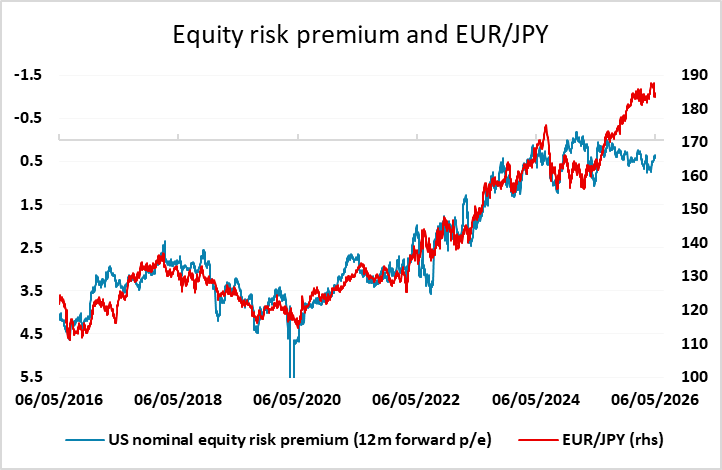

Bigger picture, the USD is generally softer overnight as optimism over a US deal with Iran mounts. The JPY gained sharply late in Asia on what is generally thought to be more BoJ intervention, sending USD/JPY 250 pips lower initially to a new post-February low of 155.03 before bouncing. The Japanese authorities certainly seem serious about preventing a renewed test of 160, and are no doubt motivated in part by the inflationary impact of higher oil prices which can to some extent be counteracted by a higher currency. Even so, it remains hard for the JPY to rally significantly against riskier currencies as long as equity market continue to perform well, as they have done overnight helped by the optimism over a US/Iran deal. But it increasingly looks like the upside for USD/JPY and EUR/JPY is capped, so that the risks are now all on the downside, even though a trigger for a significant downmove may not emerge for some time.