Swiss SNB Preview (Mar 19): Keeping a Low Profile

Once again and in line with consensus thinking we see SNB policy being unchanged when it gives its next quarterly assessment with little shift in the forecast for either growth or inflation. Admittedly, the tone of the economic outlook will be more guarded but where it will be underscored that it is too soon to make material changes to the outlook given current heightened uncertainties. The strong Swiss Franc will be mentioned but its current strength needs context (Figure 1). Indeed, it will adhere to a medium-term inflation at 0.6% (Figure 2) and a gloomy 2026 activity picture with projected GDP growth of around 1% masking the fact that the underlying picture is more sobering given the circa-0.25 ppt boost sports events will provide this year. But with inflation forecast to be within the confines of its target range of less than 2%, this will be enough to justify stable policy. We still see policy remaining on hold until at least mid-2027, with only a slight possibility of a return to sub-zero rates given the high(er) bar seen by the SNB for this to occur.

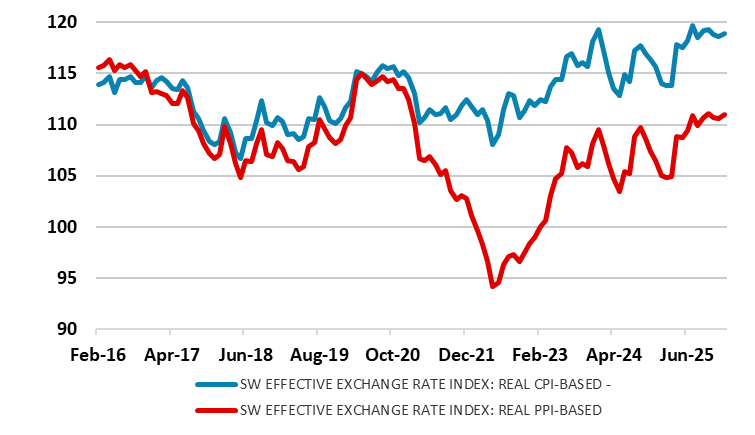

Figure 1: Two Alternative Impressions of Competitiveness?

Source: SNB – last 12 months of PPI index estimated by CE

Regardless, the increasing strength in the Swiss France is causing reverberations. More a reflection of U.S. dollar weakness than that of the euro, the nominal trade weighted Franc is hitting new highs. But while this strength in impairing competitiveness – vital to an economy where exports account for 75% of GDP – this is not the whole story despite what are increasing complaints from high profile Swiss companies. Instead we would argue that with the strong currency also reducing import and producer prices, Swiss companies are enjoying a clear reduction in their cost bases. Moreover, this is even allowing a rise in profit margins as falling costs contrast with CPI inflation currently around zero. This is important in assessing competitiveness too as compiling a real or inflation-adjusted effective exchange rate shows a far less sizeable appreciation when deflated by producer prices rather than those for the consumer (Figure 1).

Moreover, the near zero CPI inflation rate (albeit only a notch below SNB thinking) is as much a result of weak domestic price pressures which are slightly negative in smoothed and adjusted m/m measures.

Figure 2: SNB Inflation Outlook To Remain Little Changed?

Source: SNB

Thus the clear easing bias (ie an acknowledgement that the policy rate could go negative again) may be diluted somewhat amid a search for a greater assessment of current uncertainties related to the Middle East, tariffs and domestic property prices. Indeed, financial stability issues may feature more in the Board’s discussions as the summary of this month’s discussion (due Jan 8) may highlight. Notably real estate prices are still very much on a recovery track, if not clearly rising, all very much correlated with the low SNB policy rate.